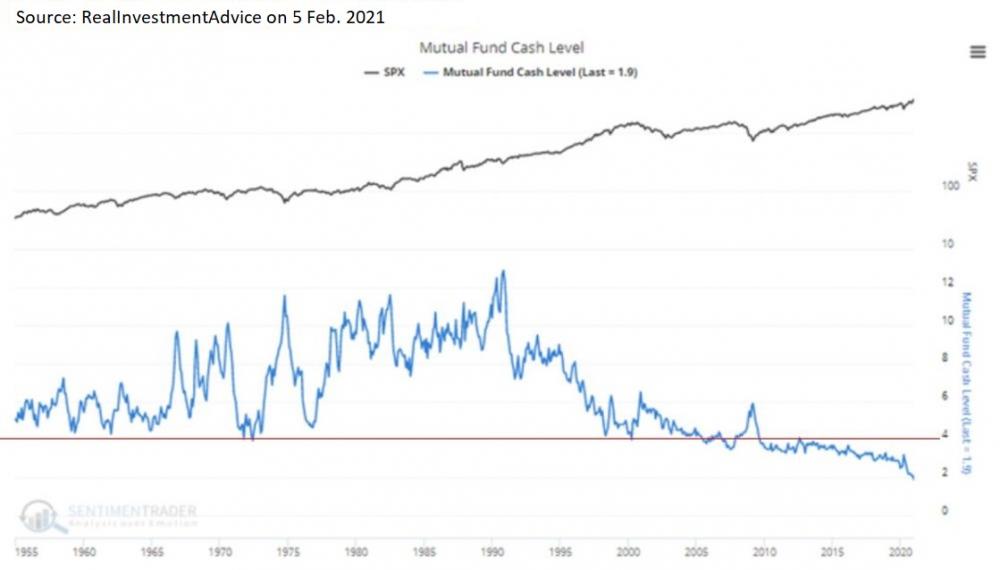

| As you can see, between 1995 and 2005, mutual funds never had cash reserves of less than 4%. After the financial crisis, these fund managers got bolder.

The cash levels are currently at only 1.5%!

This is also a consequence of the enormous pressure on fund managers to perform.

The Greed Factor

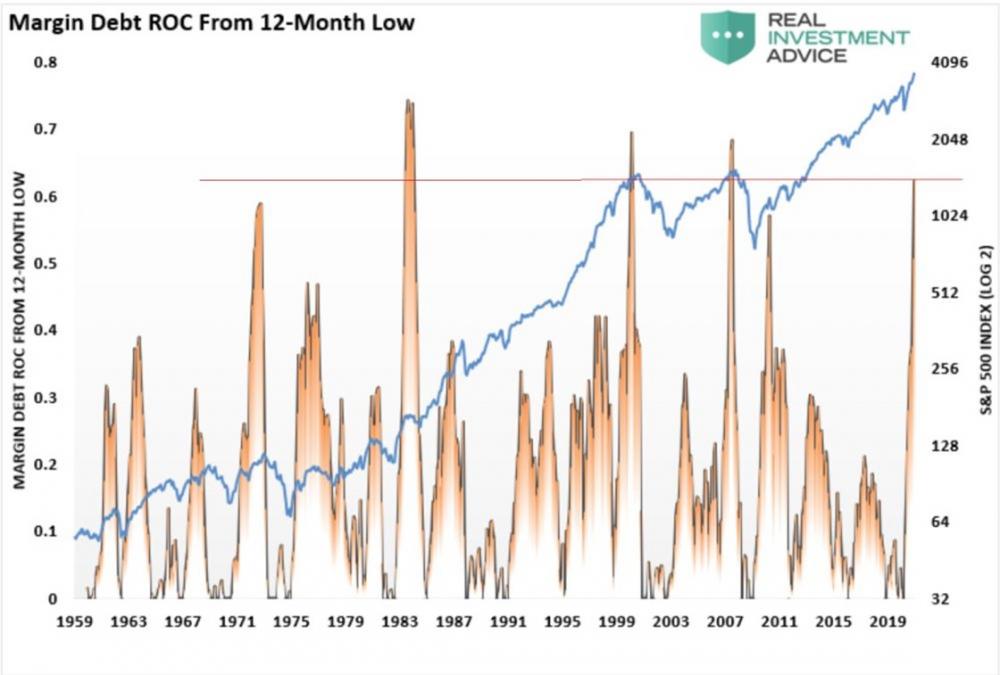

Unseasoned investors who grow bolder from success do not only enter riskier trades, they also invest all the capital they can raise.

And when that isn't enough anymore, there's money to borrow—cheaply, since the interest rates are so low.

But this type of securities lending almost always uses the portfolio as collateral.

Every market day, the collateral values are updated. For stocks, it's usually 50% of their list price.

For derivative instruments like futures, options, warrants, and certificates, it's usually set at 0%.

If the collateral value sinks below the sum of the debt due to falling stock prices, the borrower has to make up the difference by paying in more money or selling off positions.

If they don't do it fast enough, their portfolio will be subject to "forced liquidation."

The following chart shows changes in margin debt since 1959, measured from each yearly low point. |

Post a Comment

Post a Comment