Inflation is a "persistent process of money devaluation, which becomes noticeable through general price increases. One monetary unit can then constantly buy less..." is how the German Federal Agency for Civic Education describes this term. We've noted that the Federal Reserve has been expecting inflation to rise...

| | | | | | The Central Banks Will Save Us |

|

| Dear Reader,

Inflation is a "persistent process of money devaluation, which becomes noticeable through general price increases. One monetary unit can then constantly buy less..." is how the German Federal Agency for Civic Education describes this term.

We've noted that the Federal Reserve has been expecting inflation to rise since the end of August. This was documented by the statement of the FED chief (Federal Reserve Bank) Jerome Powell that one "would also like to 'tolerate' an inflation rate in the future that would be 'moderately above the +2% target' pursued so far."

Since the 2008 financial crisis, central banks' actions have solidified the impression among investors that they avert ALL crises with the panacea of money printing, virtually guaranteeing a permanent upswing in stock prices.

However, this is not true in the case of rising inflation. And certainly not with the level of (global) debt that has been reached in the meantime.

How Inflation Rises

Once again, the Federal Agency for Civic Education is quoted:

"In the emergence of inflation, the money supply in the economy plays a particularly important role. If the quantity of goods in the economy as a whole is matched by an excessively large money supply (inflation of the money supply), one condition for inflation is met.

If the aggregate demand for goods exceeds the aggregate supply of goods, which cannot be increased in the short term, rising prices are the result, and inflation sets in."

Now let's take a look at two graphs. |

|

| | | | What you see here is consistent with the above conditions for inflation:

|

|

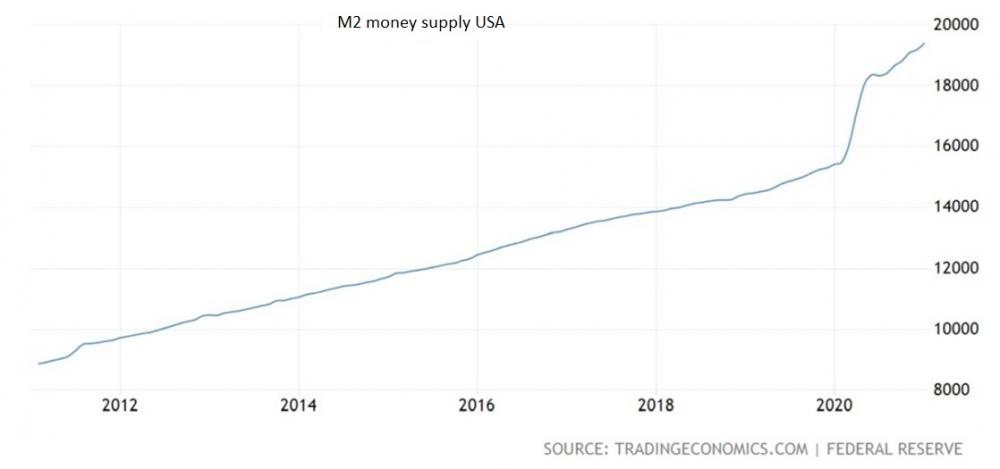

| | | M2 money supply has been rising at an accelerated pace in the U.S. for the past 12 months:

From $15.5 trillion in February 2020 to $19.4 trillion in January 2021.

That is an increase of $3.9 trillion or +25% within one year.

The same rate of increase previously took the money supply pretty much four years (from 2016 to 2020).

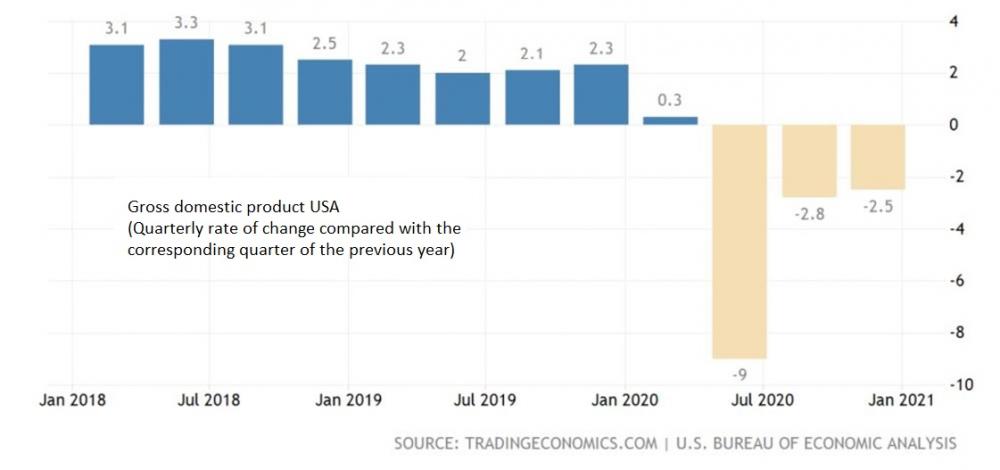

At the same time, gross domestic product (GDP) has been declining for the last three quarters. Even the 1st quarter of 2020 brought only an insignificant increase of +0.3%.

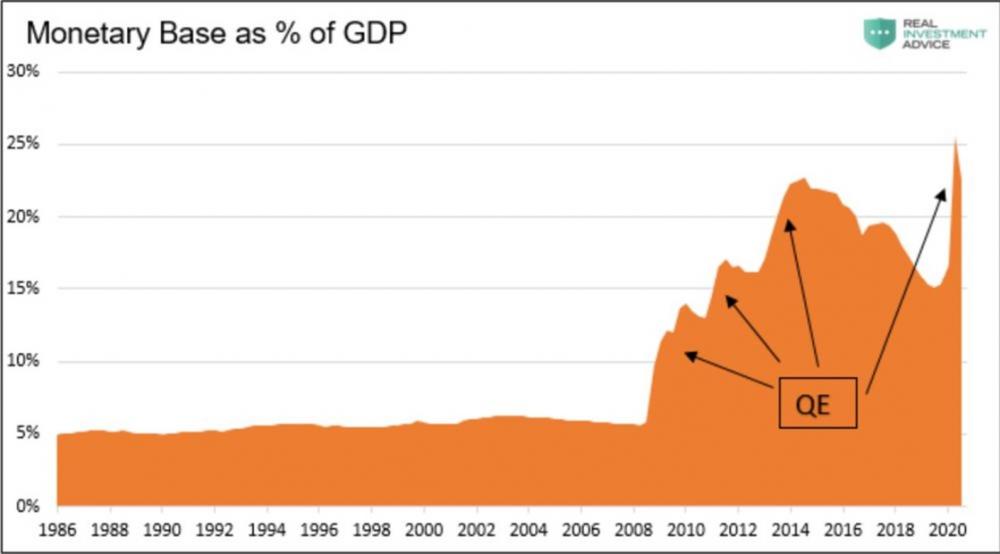

The following chart establishes a connection between the two aspects: Here, the monetary base is shown as a percentage of GDP (source: RealInvestmentAdvice.com as of January 26, 2021).

|

|

| | | You can see very well that a serious discrepancy has already arisen with the financial crisis. In the meantime, this discrepancy has increased almost fivefold compared to 2008!

The change began with the low-interest rate policy and the flooding of money by the Fed in the form of "quantitative easing" (= quantitative monetary easing = "Q.E." in the chart), as a measure to combat the consequences from the financial crisis:

Since then, the U.S. Federal Reserve - and, of course, most other central banks worldwide - have been printing digital money to finance bond purchases. By creating an artificial demand for bonds in this way, it has been possible to drive down the market interest rate, which would otherwise be outside the Fed's sphere of influence.

The market interest rate - which we looked at yesterday in the form of the yield on 10-year U.S. government bonds - is, in turn, essential for (new) government and corporate debt: It depresses the ongoing interest burden resulting from borrowing.

Why We Haven't Seen Inflation Yet

But then why did inflation not occur earlier?

This has to do with the velocity of money in circulation. The FED of St. Louis gives the following definition for this:

"The velocity of money is the frequency with which a unit of currency is used to purchase domestically produced goods and services within a given period of time.

In other words, it is the frequency with which a dollar is spent per unit of time to purchase goods and services. As the velocity of money increases, more transactions take place between individuals in an economy."

|

|

| | | It's easy to see that the velocity of M2 money in the USA has been declining since around 1998. It slowed down even more significantly with the financial crisis and has crashed in the last 12 months.

But what is the cause of this crash? The money supply was increased exorbitantly, but economic activity was cut back at the same time. As a result, even less money was put to work in terms of demand.

So no danger of inflation after all? Not quite.

The Importance of Supply Chains

Just because the velocity of circulation has slowed down so far does not per se mean that it is fixed for eternity.

When economic activity picks up again - which is exactly what the stock markets expect - and demand picks up, the circulation of the money supply will also accelerate again.

But now another factor comes into play: the disruption of supply chains!

The German transport newspaper Deutsche Verkehrs-Zeitung reported on December 16, 2020: "In a survey by Euler Hermes, 94 percent of around 1,200 managers said their company had to deal with interruptions in its own supply chain at least some of the time."

It went on to say that according to a survey of 1,000 retail and industrial supply chain executives from 11 countries (including Europe, the U.S., China, and India) conducted by consulting firm Capgemini in August and September, 80% of respondents reported "problems in all areas of their operations."

"The main factors cited are bottlenecks in critical parts and materials, delayed deliveries and longer lead times (nearly 75 percent each), difficulties in adjusting production capacity, and planning uncertainties due to fluctuating demand (about 70 percent each)."

You see: Disrupted and often out-of-sync supply chains are a major problem for manufacturing companies. When increased demand - for example, from the planned U.S. stimulus package and an end to the lock-down - meets reduced supply that also cannot be promptly replenished, the velocity of money in circulation increases.

Tomorrow, we'll look at whether inflation is already on the horizon and put the partial aspects discussed so far into context.

Enjoy your day, |

|

| | | | | | |

|

|

Post a Comment

Post a Comment