Do You Use the Best Data Available?By Marc Chaikin, founder, Chaikin Analytics  'You're not really going to only rely on the firm's research, are you?' 'You're not really going to only rely on the firm's research, are you?'

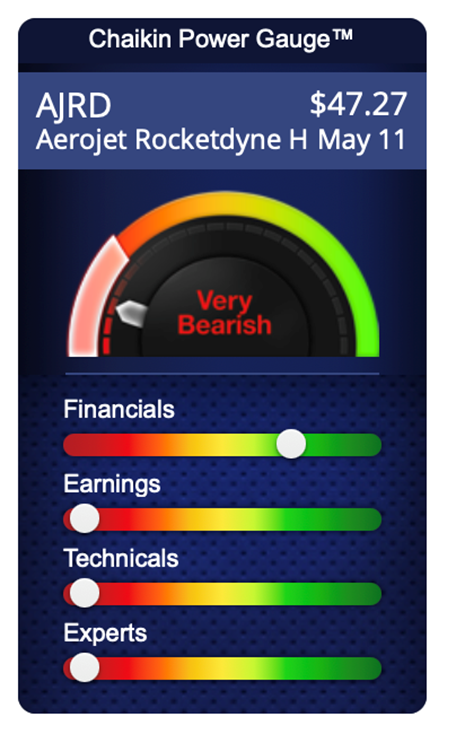

It was 1966. I had just landed a position as a broker. And at the time, I really did think my own firm's research would be plenty for me and my clients. A member of the "old guard" had pulled me aside to tell me different. "Listen, you'll have to learn this on your own. But there's someone I think you should know about..." It might sound like a random piece of advice. But it was actually a life-changing introduction... one that completely transformed my approach to helping investors. It started when my colleague introduced me to George Chestnut's financial writing. I'm guessing you haven't heard of Chestnut. But his work was pioneering at the time. He used math to find the strongest industry groups... and the strongest stocks in those groups. That made Chestnut an outsider for sure. Back then, nearly everyone was looking at a smattering of fundamentals. Then, they'd assemble an interesting story around those few bullet points, and that was it. The best storytellers turned out to be talented brokers. That is, they were talented at getting their clients to buy. Great for them... Not so great for their clients. The day of that conversation, I realized my mentor was right. I needed more than just stories. My clients deserved better. Not only that, but to be able to really sell, I knew I'd need to have data to back up my claims. So, I did the most reasonable thing I could... I signed up for Chestnut's newsletter service. Chestnut's work was my way of accessing the best data available at the time. And I knew that I wanted the best data on my side. Here's the thing, though: To get the best data, you have to go the extra mile... Chestnut was a bit out there compared to most analysts at the time. The guy spent his time meticulously tracking the major industries trading on Wall Street. He did a lot of it by hand. And he did the rest with early calculators. Those of us who were around back then know what a monumental task this was. You'd have to be a little crazy to even pursue it. I didn't realize where I was headed back in the '60s... not at first. But once I looked outside my own firm, I started to follow Chestnut's path. My life's work became collecting data, parsing it, and using it to make evidence-based investing decisions. I'm very fortunate to have been successful at it. Bloomberg built my systems into its world-famous trading terminals. And its main competitor Thompson Reuters did, too. I made finding the best data into my life's goal... and just as important, performing the best analysis on it. I've found it deeply rewarding. And I'm passionate about sharing it. That's because the best data gives you an edge as an investor that nothing else can. I saw firsthand exactly how important this was – after the financial crisis in 2008... I saw the little guy get creamed by Wall Street. So my focus shifted yet again. I developed a set of tools for individual investors. They're specifically designed to turn trading and investing into a fair fight for those who aren't Wall Street elites. Together, this set of tools is called the Power Gauge. And I've poured everything I've learned over my more than 50 years in finance into it. My Power Gauge even got me on CNBC's Fast Money Halftime Report back in 2012. "Based on the bearish Power Gauge rating, I think the risk of a negative earnings surprise is too great," I said back on a panel with Jon Najarian. I'm guessing you've heard of him... The NFL linebacker turned high-profile trader had become a household name in the financial world by then. He would go on to sell his publishing and trading platforms, optionMONSTER and tradeMONSTER, to E-Trade just a few years later... for $750 million. He was at the peak of his financial career. And although I'd been making the rounds on CNBC, this was the first time we had crossed paths. The stock we were talking about was online travel agency Priceline... The company, which later changed its name to Booking Holdings, was one of Jon's bullish trades at the time. And I had just told CNBC viewers that it looked too risky... The thing is, I didn't know anything about Priceline. But I did have the Power Gauge to guide me. And that tool was all I needed... The Power Gauge is the culmination of my life's work. It combines more than 56 years of data-driven market research. And it packages everything I've learned about the markets into actionable information for every stock it processes. So, I didn't need to know much about Priceline. I simply typed in the ticker and got my report. Instantaneously, I was able to see that Priceline was set up to released disappointing earnings. The Power Gauge made it clear. Obviously, the interface for the Power Gauge has gotten more refined over the years. Here's an example of another stock that the Power Gauge turned bearish on recently... You've probably never heard of Aerojet Rocketdyne (AJRD)... But that's not important – because the Power Gauge has. Each of these sliders is backed by data that can be further explored. And the data shows us that AJRD is in a risky spot for investors right now. That was the kind of setup I saw when I told Jon – one of the most famous traders in finance at the time – that Priceline looked like a no-go. The Power Gauge had provided me with the most important (and most relevant) information. Again, Jon was excited about the stock. But he was a professional. And that means he was willing to re-examine his ideas. The interview ended with Jon saying, 'I'm going to take a harder look, since Marc Chaikin says he doesn't like it'... That was Monday, August 8, 2012. On Wednesday, the day after Priceline's earnings, the Halftime Report did a highly unusual follow-up. The host started by asking Jon, "Chaikin spooked you a little bit?" He responded... He did indeed. And I think a lot of folks followed Mr. Chaikin. Those of us that picked up some cheap out-of-the-money puts [...] well, they worked out like a charm. Those puts went from like $1.80 last night to $15 to $16. Again, great call from Mr. Chaikin. And thanks Marc for helping me out. In short, the Power Gauge was right. Priceline missed earnings. And Jon listened to it, made a bearish bet, and racked up big profits instead of taking major losses. Now, one great call is just that... a single great call. But it was only possible because I had the Power Gauge at my side. The Power Gauge uses the best data available to help individual investors make consistently great calls. And my goal is to share that power with as many investors as I can. I'll share more on how it works in the coming days. In the meantime, I hope you'll watch the brand-new presentation I just put together... I pulled back the curtains on my Power Gauge tool to show you which stocks could rise 100% or more, by typing in any of 4,000 tickers. Last year alone, my Power Gauge identified bitcoin miner Riot Blockchain (RIOT) before it rose 10,090% in less than 12 months... software firm Digital Turbine (APPS) before it rose 789% in eight months... online retailer Overstock (OSTK) before it rose 1,050% in four months... and more. You can watch this presentation before it goes offline for good by clicking here. In the mailbag, a reader reacts to a recent essay on employment and the economic recovery... Has anyone used any high-end data sources, such as those from Bloomberg or Thomson Reuters? If so, what was your experience? Send an e-mail to feedback@empirefinancialresearch.com. "Berna, I'm glad you wrote of the K-shaped ECONOMY rather than the K-shaped RECOVERY, as we became a service-dominant economy, as opposed to a productive economy, well before COVID-19 struck. We have more people now earning money (when they do work) serving other people yet producing nothing tangible. We're like the old joke of three men stranded on an island for a year, who when rescued, claimed to have become incredibly rich by trading hats with each other! "The greatest generation, which was glad to have a job after the Great Depression, and became used to being highly productive during WWII, have passed. Their children, raised in such an environment and quite productive themselves, but still having a lesser standard of living in their early years than today's middle class does, have largely retired. That generation (mine, sad to say) to a large extent wanted to spare their children any hardship, gave them all they wanted, and they responded by expecting everything to be given to them, an attitude they have passed to their own children, in spades. "As a result, we have many people who have learned no productive skills, and/or are racially sequestered in environments that provide little opportunity for advancement for those who might wish it, leaving us with a large number of people who will never earn much, and who will be happy to not work at all if government will provide enough benefits for them to exist in a manner little worse, or perhaps even better, than that they could earn and support by working. "Of course, it's not just the rich who benefit by keeping more of their money, but also the rest of us, who have at least an unconscious reason to maintain paying such people as little as they can to keep them working, as it keeps the cost of their restaurant meals, garbage collection, yard care, etc., at cheaper levels. "I could go on about how productive economies like China are eating our lunch, how a money-printing government doesn't really need higher taxes to do its business (which is already too extensive), how paying the lowest-level workers more will raise prices and make life for the middle class more expensive, how our status in the world is following that of pre-war to post-war Great Britain, and many other consequences, but maybe another time- I've written for a fairly long time already." – Otto K. Berna comment: Otto, there's a lot to unpack in here... You raise the oft-debated topic of whether it is OK to have such a service-oriented economy. We have been going in this direction for decades, and the trend may be irreversible at this point. But it does make you wonder if the reduction in manufacturing jobs is a factor in creating the K-shaped, "have and have not" economy we seem to be stuck in, regardless of whether the economy is strong or weak. There just aren't as many opportunities to make a good living with only a high school education as there were in the earlier generations that you reference. I'm intrigued by your acknowledgment that there is a persistent societal inclination to pay as little as possible to low-skilled workers in hourly jobs. It reminds me of a tweet I saw a couple of weeks ago, posted by a money manager that I follow... Source: Twitter/DavidSchawel It's interesting to me that consumers have come to accept inflation as normal and acceptable for all sorts of things – from food to lumber, from plants to luxury goods – but the idea of laborers asking for more money for their work is considered offensive to many people. Regards, Marc Chaikin

with Berna Barshay

May 27, 2021 If someone forwarded you this e-mail and you would like to be added to my e-mail list to receive e-mails like this every weekday, simply sign up here. |

|

Post a Comment

Post a Comment