The Update Issue: L Brands Reveals the Fate of Victoria's SecretBy Berna Barshay  On Tuesday, L Brands (LB) made a big announcement... On Tuesday, L Brands (LB) made a big announcement...

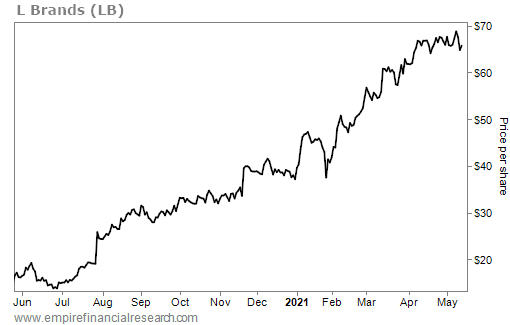

The company said it will pursue a tax-free spin-off of its Victoria's Secret lingerie retail division, instead of selling the chain. A year ago, I offered readers an extensive history of the rise and fall of Victoria's Secret, but I'll give the CliffsNotes version here for the factors leading up to this corporate break up... Investors had long been itching for L Brands to unshackle its Bath & Body Works retail division from what many viewed as the albatross of Victoria's Secret. Victoria's Secret had been on a multi-year decline in value after a series of operational missteps, primarily related to marketing and merchandising. While Victoria's Secret had been one of the best-performing chains in retail for around two decades, results turned south in 2016 and turnaround efforts had since faltered. While Victoria's Secret stumbled, Bath & Body Works soared... The seller of candles, lotions, and other home fragrance products has proven an incredibly reliable and steady grower within the challenged retail industry. The chain also has industry-leading margins in the low 20% range. The company reached an agreement in early 2020 to sell the lingerie chain to private equity ("PE") firm Sycamore Partners, a deal that I hated because it was happening at a fire-sale price. The deal was brokered shortly before the pandemic took hold across the nation, and Sycamore used the temporary retail closures to legally maneuver its way out of the $1 billion deal. Its cold feet – even at such an uncertain time – were interpreted as a poor signal for Victoria's Secret's prospects. When I wrote about the company shortly after the deal broke, LB shares traded around $15, down 85% from their all-time highs in late 2015. What a difference a year makes... In the wake of the busted deal and during an obviously tough year for retailers, management at Victoria's Secret finally started to get its turnaround right. Fourth-quarter results showed phenomenal improvement at Victoria's Secret. Not only was the sales contraction contained at a modest 3% – not bad for apparel retail during a pandemic – but operating margins soared. In the fourth quarter, Victoria's Secret posted a 19% operating margin. This is an excellent level for any retailer and a huge increase from the 8% it reported in the prior year. Green shoots notwithstanding, L Brands reiterated its commitment to giving Wall Street what it wanted: a separation of the two divisions. Management promised that Victoria's Secret would be sold or spun off by this August. Back in the February 26 Empire Financial Daily, I wrote... It's unclear if Victoria's Secret will end up spun off or sold. I would normally say a spin-off was a near certainty because of the tax advantages of that strategy. Structured correctly, the spin could be a tax-free transaction for shareholders, whereas an outright sale will trigger a taxable gain for the company – reducing net proceeds. But I wouldn't rule out a sale – even though it's less tax-efficient – because there's so much money sloshing around seeking an asset to buy. Not only do private equity firms have more money to put to work than ever, but the explosion of special purpose acquisition companies ("SPACs") means there are literally hundreds of companies out there looking for a deal... And Victoria's Secret is in the sweet spot for the size deal many SPACs (and private equity firms) are pursuing. The New York Times reported on Tuesday that L Brands received multiple bids "north of $3 billion" for Victoria's Secret. That's 3 times the price that Sycamore walked away from less than a year earlier! But L Brands said no to $3 billion. As the Times reports... It turned the offers down, because it expects to be valued at $5 billion to $7 billion in a spinoff to L Brands shareholders. Analysts at Citi (C) and JPMorgan Chase (JPM) recently valued Victoria's Secret as a stand-alone company at $5 billion. This may seem greedy, given where the company was a year ago. Things are looking up at Victoria's Secret... But retail stocks are notoriously volatile, and consumers are notoriously fickle when it comes to apparel retailers. L Brands is taking a gamble, but I'd argue that after years of struggle, this is not the time to sell it for anything less than full price. On Tuesday, L Brands also released preliminary results for the first quarter... The results at Bath & Body Works are almost always solid... But these were excellent. Sales almost doubled from $761 million to $1.5 billion in the first quarter, but of course COVID-19 lockdowns disrupted the first quarter of last year, making for an easy comp. First-quarter 2021 revenue at Bath & Body Works was up 60% versus the first quarter of 2019. That's fantastic two-year growth for a 30-year-old retailer that barely opened any new stores and is operating at the tail end of a pandemic. Preliminary operating margins came in at 26% – more like software company margins than retailer margins, which generally range from mid-single digits to mid-teens. But Bath & Body Works being a total beast isn't groundbreaking news... What's more interesting is what was reported at Victoria's Secret... Sales at the lingerie chain were down 7% versus 2019 levels, which is not terrible when you consider it closed 233 locations over the last two years. But it's the margins, not the revenue growth, that's key here. The chain reported preliminary operating income of $245 million in the first quarter, which equates to a healthy 16% operating margin. Putting this result in perspective, operating income for the 2021 fiscal year that ended in January was negative $25 million. In fiscal 2020, Victoria's Secret had negative operating income of $616 million... And it just put up $245 million in one quarter. Framed another way, Victoria's Secret just registered its highest first-quarter operating income since 2015, which happened to be its most profitable year ever. In the announcement of the decision to spin not sell, L Brands' Board of Directors Chair Sarah Nash explained... In the last 10 months, we have made significant progress in the turnaround of the Victoria's Secret business, implementing merchandise and marketing initiatives to drive top-line growth, as well as executing on a series of cost reduction actions, which together have dramatically increased profitability. As a result of these efforts, Victoria's Secret is now well-positioned to operate as a standalone, public company. The move to not hit a bid that is up 200% in a year and instead spin off the company was framed as the path that will "return the highest value to shareholders." I agree with that assessment. Not only do I think that Victoria's Secret is worth $5 billion to $7 billion (not the $3 billion that buyers offered), but I also think if the company can continue to execute on its current momentum, it could be worth $8 billion to $10 billion in a couple of years. LB shares are up around 335% since I recommended them last May in Empire Financial Daily... Last November, when the shares had risen 160% in six months, I said, "I would consider taking profits on half your shares." While I thought the stock had more room to run, it's always prudent to book some gains when you make so much money so fast, especially in a notoriously volatile sector. Since then, LB shares have barely looked back... After so much frustration, the turnaround at Victoria's Secret is finally meeting my expectations... and then some. Like L Brands management, I'm exercising some patience and waiting for the market to fully value Victoria's Secret... I'm not selling here, either. In the mailbag, readers write in about SPACs and home-exercise company Peloton (PTON)... Any loyal Victoria's Secret or Bath & Body Works shoppers out there? If so, I would love to hear what you like about shopping there. Has anyone observed big changes in marketing or merchandising at Victoria's Secret in the last year? If so, what do you think of them? Share your thoughts in an e-mail to feedback@empirefinancialresearch.com. "Hi Berna, I love reading your newsletter. It is great that you write about how SPACs can be dangerous to invest in. I subscribe to Empire SPAC Investor. I originally thought if I just buy the recommendations from this list, I will make money. What I did not realize is that if the SPAC has not yet merged, it is riskier. SPACs expire in two years [if there is no deal]. "I bought a lot of Pershing Square Tontine (PSTH) warrants thinking the company would merge with Stripe. But when Bill Ackman announced the deal was cancelled, I lost half the value. I was too optimistic, and I put about 25% of my portfolio in this one. I learned my lesson. From now on, I will only buy a warrant when there is a pending merger. "I know that if I bought the PSTH stock, I would get the face value of $20 back. But what I bought was a warrant. What would happen to the warrant if PSTH never found a company after two years?" – Javid L. Berna comment: Javid, first I am sorry you took such a big hit on PSTH warrants. It's important to remember that "warrant" is just an alternative, fancy name for "call option." Options and warrants have expiration dates, while stocks do not. So you have to do two things right to make money in options and warrants: get the underlying stock direction right and get the timing right. This makes them an inherently risky investment relative to stocks, so you should keep position sizes in them relatively small. Second, the rumored deal for Stripe was just that – a rumor. Ackman had nothing to cancel, except speculation. I would also add that I think the odds of Ackman never finding a deal for Pershing Tontine are super low. That's not the case with all SPACs, but it is the case for Ackman's. Finally, to answer your question, if a SPAC fails to find a deal and returns cash to shareholders, the warrants will be canceled, and the holders will lose their money. "I don't understand the infatuation investors have with Peloton (PTON). It's nothing more than an overpriced exercise bicycle with a live instructor, which you get to pay a reverse annuity monthly fee for. I think it will be in the dustbin of fad exercise equipment like Nordic Trac in a few years." – John H. Berna comment: John, we'll have to agree to disagree on this one. I think Peloton is building a huge moat, home fitness is here to stay, and as I wrote last June, the company could be the Netflix of fitness. I am price sensitive and looking for a lower price to re-enter PTON shares... But I remain long-term bullish. PTON shares were among those pitched on Wednesday this week at the (virtual) Ira Sohn Investment Conference, a premier charity event that many Wall Street players attend every year. Octahedron Capital's Ram Parameswaran offered an investment thesis that was similar to the one I've laid out in Empire Financial Daily, although he thinks the stock is a good buy here. I'm more cautious that it has some downside potential before it resumes its climb. One thing we agreed on, however: He also called it the "Netflix of fitness." Regards, Berna Barshay

May 14, 2021 If someone forwarded you this e-mail and you would like to be added to my e-mail list to receive e-mails like this every weekday, simply sign up here. |

|

Post a Comment

Post a Comment