ESG Investing Moves Beyond Virtue SignalingBy Berna Barshay  This story is like the corporate version of 'The Little Engine That Could'... This story is like the corporate version of 'The Little Engine That Could'...

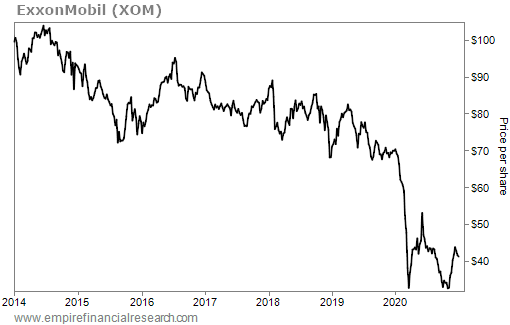

It's about a tiny hedge fund that brought a massive corporation – one that was once the largest in the world by market cap – to its knees. This hedge fund – the aptly named Engine No. 1 – manages only $270 million but bit off the big challenge of trying to oust four board directors from oil giant ExxonMobil (XOM). Citing poor financial performance, a lack of decisive action to address climate change, and its corporate contribution to the climate crisis, Engine No. 1 proposed its own slate to replace the directors, in the first serious activist investor challenge to Big Oil in the U.S. Engine No. 1 wants to see Exxon take meaningful steps to diversify to renewable energy and stop maximizing its oil production. It argued that Exxon has its head in the sand about the climate crisis, which poses an existential threat to its business. In its investor presentation, Engine No. 1 criticized Exxon... A refusal to accept that fossil fuel demand may decline in decades to come has led to a failure to take even initial steps towards evolution, and to obfuscating rather than addressing long-term business risk. Despite being outmuscled by a corporate behemoth that went on an eleventh-hour full-court press to defeat the challenge, Engine No. 1 prevailed in replacing at least two of the Exxon directors... Vote-counting continues to determine the fate of the two. Engine No. 1's upset isn't being regarded as a fluke and is no small matter for the energy – or money management – industries. Anne Simpson, managing investment director at the highly influential California Public Employees Retirement System ("CalPERS") – the largest pension fund in the U.S. – commented, "Investors are no longer standing on the sidelines. This is a day of reckoning." By picking a fight with ExxonMobil, Engine No. 1 essentially kicked a dog when it was down... Last year, Exxon was tossed out of the Dow Jones Industrial Average, after being a member since 1928. That downgrade in prestige happened after Exxon lost more than $250 billion in market cap from its peak of around $450 billion in mid-2014, and after earnings per share ("EPS") fell from $7.60 in 2014 to just $2.44 in 2019, before the COVID-19 pandemic took an additional toll on the company. In short, XOM shares were down 59% from 2014 through 2020... Over the same time period, the benchmark S&P 500 Index was up 103%. Things have been better lately. As oil prices soared, so did XOM shares... which are up 47% in the year to date – massively outperforming the S&P 500, which is only up 12%. But the strong relative performance this year isn't enough to call a trend, as XOM shares have underperformed the broader index in eight of the past 10 years. Engine No. 1's win never would have been possible without recruiting some big Wall Street players to its cause... Engine No. 1 holds just 0.02% of Exxon's shares outstanding, representing a position worth around just $50 million. Its own vote count is basically a rounding error to the outcome, but its victory came by recruiting big money managers – the ones who do have a lot of votes – to its side. Among the major institutional investors that Engine No. 1 got support from are a number of large pension funds and endowments, including not only CalPERS but also the California State Teachers' Retirement System ("CalSTRS") as well as the New York Common Retirement Fund and the Church of England. BlackRock (BLK), the largest asset manager in the world and the second-largest Exxon shareholder, has been signaling a sustainability focus while at the same time fighting at times with climate-driven activists, who accuse it of not doing enough to impact climate change. Last Tuesday, BlackRock announced it would back three of Engine No. 1's four nominees, and this seemed to turn the tide in favor of the activist challenge. After the vote, we learned that top shareholder Vanguard and third-largest shareholder State Street (STT) voted for two of the Engine No. 1 nominees, which is especially notable since so many of the Vanguard and State Street shares are held by passively managed index-linked products. Earlier in May, Institutional Shareholder Services ("ISS") told clients to vote for three of Engine No. 1's nominees. Glass Lewis also told its clients to vote for two of the four nominees proposed by Engine No. 1 and noted... We believe Engine No. 1 has presented a compelling case that, without a more concerted response and well-developed strategy... related to the global energy transition, Exxon's returns, cash flow and dividend, and thus its shareholder value, are increasingly at threat. Firms like ISS and Glass Lewis are highly influential on these matters of corporate governance as large money managers – mutual funds, pension funds, and sometimes hedge funds – hire them to advise on how to vote in contested shareholder contests, such as this one. It's important to note that this wasn't the first time Exxon or its peers had been pressured by advocates for sustainability... But this was the first time a measure passed, and management lost. And it lost a big one... While the two (or possibly four) directors handpicked by Engine No. 1 will be a minority on Exxon's 12-person board, they will be there, as the activist hedge fund explained, to serve as watchdogs and monitor where Exxon spends its money. They will also lobby for "a strategic plan for sustainable value creation by fully exploring growth areas, including more significant investment in clean energy." Sure, management and the other eight to 10 members on the board can choose to blow off the input of Engine No. 1's representatives... But they do so at the risk of their share price because these representatives won a vote, meaning that the majority of Exxon's shareholders support the demands of Engine No. 1. The company can choose to stonewall the new board members, but holders who get ignored are also free to dump their shares. The fact that XOM shares have been such a poor investment for many years is what opened the door for Engine No. 1 to win this proxy fight. While there may be a moral argument for Exxon pursuing a more sustainable path, Engine No. 1's argument for a change in board oversight was firmly rooted in an economic argument: Exxon has seen earnings fall and has therefore been a bad stock, and the only way for the company to make more money is to find a go-forward strategy that isn't wholly reliant on fossil fuels. It does feel like a greater good may have been motivating Engine No. 1, an entity barely six months old and seemingly set up to pursue this fight. On the surface, it doesn't seem like they are likely to make much – if any – money pursuing this. As Bloomberg's Matt Levine explains... Spending $53 million on stock and $30 million on a proxy fight is an odd business proposition: If your plan works and the stock goes up 60%, you still lose money. In some instances, companies are required to reimburse activists who are successful in their proxy contests. And Engine No. 1 may end up making money off this investment in ways that go far beyond Exxon... The small startup hedge fund just launched last December, but its seasoned managers are alums of top-tier funds. It's possible this was a high-profile, calculated bet that the managers knew would attract wads of capital should they pull off an upset. But even if one were less cynical about Engine No. 1's motivations, moralizing aside, it's important to remember that a valid financial argument is what got it over the finish line. Big financial funds like the ones that backed Engine No. 1's alternative board candidates have been talking a big game for years when it comes to ESG investing... "ESG" refers to "environmental, social, and corporate governance" investing... It's a field of investing that considers a corporation's sustainability and effect on society. The general idea is that companies that are good corporate citizens and earn their profits in a way that is good for the environment and society in general will win in the long run because their earnings will in turn prove to be sustainable and durable. A 2011 study out of Wharton Business School demonstrated that companies listed in the 100 Best Companies to Work For outperformed their peers in the stock market by 2% to 3% per year from 1984 to 2009. They also had a great track record of posting earnings that beat analyst expectations. Despite evidence that being strong on ESG factors has a correlation to posting strong financial results, ESG for many years remained a specialty area in investing, with dedicated funds pursuing the strategy. But over the past few years, beginning in Europe and working its way over to the U.S., questionnaires about how the evaluation of ESG factors works itself into the investment process started cropping up as a routine part of the due diligence done by allocators at pension funds, investment consultants, and other entities that give big bucks to institutional money managers. The victory of Engine No. 1's David against the Goliath of the biggest American oil company could in fact usher in a new era for ESG. ESG investing so far has been more about avoiding bad actors than it has been about specifically investing in companies actively contributing to a more sustainable or just world. Among the most widely held "ESG stocks" are consumer-products titan Procter & Gamble (PG), software giant Microsoft (MSFT), and Google parent company Alphabet (GOOGL). While all these companies have set broad sustainability goals – Microsoft aims to be carbon-neutral by 2030, for example – none of them are engaged in a primary business with ESG at the heart of the mission. Thus to date, the practice of ESG investing has been more about deciding what not to own – such as Big Oil and social media giant Facebook (FB) – than actively buying companies engaged in environmental or other social endeavors, partially because the universe of public companies pursuing such goals is so small in terms of number and market cap. But Engine No. 1 might drag ESG investing into a new era – an activist one in which funds buy stakes in the companies historically shunned by ESG investors and try to change them from the inside. If the events last week at Exxon end up marking the birth of a trend, then we could see the current momentum in ESG investing – the practice of which has so far been dominated by a "first, do no harm" attitude – give way to an era of "impact investing," which goes one step further and seeks to steer capital to companies that act in a way that ultimately benefits society. In the mailbag, readers react to my essay on Amazon's (AMZN) potential acquisition of Hollywood studio MGM, which was announced officially later in the week... Do you think that ESG factors should be considered when big institutions invest? What about when individuals invest? Do you agree with the study that suggests that pursuing sustainable and socially responsible business goals will result in better long-term returns for corporations and their shareholders? Share your thoughts in an e-mail to feedback@empirefinancialresearch.com. "Dear Berna, I truly enjoy your reports, and as a former sell-side analyst I really know the effort it takes to produce such an engaging, informative, and thought-provoking product daily. "Your analysis of Amazon's proposed acquisition of MGM is a great piece and a study in understatement. You tersely wrote that '[you]... never 100% understood the synergies between the Amazon Studio and the rest of Amazon's businesses... but it wouldn't be the first time that a well-thought-out Amazon endgame is opaque to a third-party observer.' "Your concise history of MGM and the one percenters that owned the studio over the years made me think that you were leading us to what many a Hollywood wag has been saying sotto voce about the underlying reason for world's richest man's years-long adventures in the screen trade (tip of the hat to William Goldman here) which is best summarized in a name: Lauren Sanchez. "But you left this/her out, maybe because you consider Empire Financial Daily a family publication. But never mind, I still loved your report. Keep up the great work!" – J.G.S. Berna comment: Thanks for the compliment, J.G.S.! And you're right, I didn't opt to delve into the psychological reasons that a titan of industry with unlimited funds like Jeff Bezos would want to get into the entertainment business or own a trophy asset like MGM. But yes, there's always that factor possibly at play. Spaceships are pretty cool as far as toys go, but when you're the richest man in the world... why limit yourself? "Berna, Prime Video making unreasonable acquisitions and relying on Amazon's other businesses to backstop the inevitable losses is a violation of antitrust law." – O.P. Berna comment: I'm not an antitrust lawyer, so I can't comment on that one. I do know that the way regulators define markets, it makes it very hard to stop companies operating wildly profitable large businesses from coming in and cornering new areas with investment that overwhelms companies with fewer financial resources. "When Disney (DIS) started its own streaming service, the futures of Netflix (NFLX) and of the big screen movie theater chains became very doubtful. I see streaming today as not unlike where Blockbuster and Hollywood Video were the day Netflix started its streaming service in competition with its snail-mail based DVD service. The future belongs to the streaming services with huge content-creating potential, along with a huge content library. "Take Disney's library and MGM's library away from Netflix, and it becomes much weaker in the long run. Netflix will also need to acquire a content library, but it's not in as strong a position to do so. Amazon sees this long-term trend and recognizes it needs a content library which it currently lacks to compete successfully with Disney. Once most of the major distributors are in control of the streamers, big screen movie theaters operating independently from the same streaming companies have a very limited future, if any. "In ten years, I look for Amazon, Disney, and Netflix (if it acquires a distributor's library – maybe Turner's), to be the big three of streaming, with one or two of them also having acquired one of the large big-screen chains at bargain prices." – Kelly F. Berna comment: Kelly, I largely agree with your vision of how this plays out and have been skeptical of streaming latecomers (even those with big libraries) like Paramount+. But I diverge from your view a bit with regards to Netflix... I'm not sure I agree it needs an acquisition. I was bearish for many years (unfortunately for me) on Netflix, thinking the incumbent media companies would ultimately cripple it by pulling their content... which they did, but way too late. In the interim, Netflix has built its own mountain of content and subscribers. It's Netflix's game to lose now. Regards, Berna Barshay

June 1, 2021 If someone forwarded you this e-mail and you would like to be added to my e-mail list to receive e-mails like this every weekday, simply sign up here. |

|

Post a Comment

Post a Comment