The Biggest Threat to the Markets TodayBy Mike DiBiase  It's the No. 1 threat on many investors' minds today... It's the No. 1 threat on many investors' minds today...

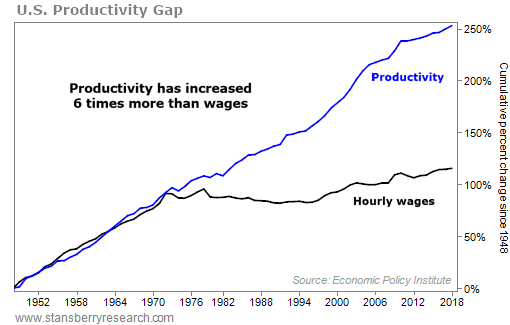

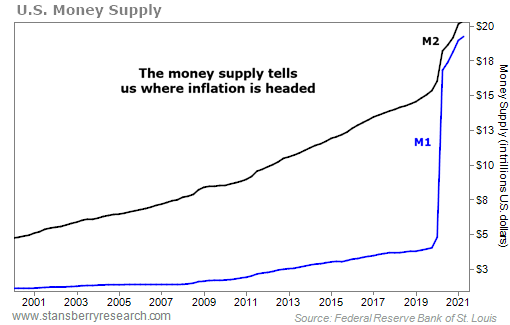

The mainstream media can't stop talking about this threat... You can't go a day or two without reading a headline or seeing a news story about what it could all mean for us. It isn't a new threat, either. Folks in our country have feared its onslaught for decades... For example, in the late 1970s, former President Ronald Reagan described this threat better than anyone. He said it was "as violent as a mugger, as frightening as an armed robber, and as deadly as a hit man." Reagan wasn't talking about the perpetrators behind the ongoing Iran hostage crisis at the time... or some rogue organization out to assassinate him. He was talking about inflation... the general rise in prices in an economy. Here in the U.S., inflation doesn't happen overnight. It's an insidious force that slowly – and often secretly – erodes our wealth, perhaps taking a few decades for people to notice its real impact... As comedian Henny Youngman once joked, "Americans are getting stronger. Twenty years ago, it took two people to carry $10 worth of groceries. Today, a five-year-old can do it." In today's essay, I will explain why investors are correct to worry about inflation... Right now, it's the biggest threat to both the stock market and the much bigger bond market. More important, I'll show you what steps you can take right now to prepare for – and even thrive – whenever the next crisis strikes in the markets. Let's start with the biggest myth about inflation... Many people make the mistake of thinking that a small amount of inflation is good – that it's some byproduct of economic growth. After all, the Fed targets 2% inflation... so that must mean that this is a good amount, right? But have you ever asked yourself why the Fed wants inflation? This question has always left me scratching my head... Why would anyone want prices to increase? Do you want to pay more for the same things you bought last year? That's the definition of getting poorer, isn't it? Wouldn't a rational person want the opposite of inflation – deflation? Most arguments about why deflation is such a bad thing center around the idea that it's only caused by economic contraction. But this view misses a much bigger point... Deflation doesn't have to be caused by a shrinking economy. I would argue that most price deflation is caused by economic expansion... resulting from increases in productivity. So what causes inflation? For starters, it isn't a natural outcome of a healthy economy. It's a result of government policy. Inflation is not caused by the actions of private citizens or businesses. It's caused by the artificial expansion of the money supply by the government. It slowly takes money out of all of our pockets. That's why American economist Milton Friedman once called it "taxation without legislation." From an economic point of view, what really matters is price inflation relative to wage inflation. In economics, that's known as your "real wages." As long as your income is rising faster than the rate of inflation, you're getting richer. In other words, your real wages are increasing. But on the flip side... if the rate of inflation is rising faster than your income, your real wages are declining and you're getting poorer. The truth is... for most people, prices have been rising at about the same rate as their wages over the past 50 years. So their purchasing power is roughly the same. But here's what most people don't realize... They should be much richer than they are because of massive increases in productivity over that period. You can see when the disparity started to occur in the following chart. Notice from 1948 to the early 1970s, productivity and wages increased at about the same rate – around 2.5% per year. But in the five decades since then, wages have remained flat while productivity has soared... So what happened in the early 1970s to cause such a dramatic divergence? That's when former President Richard Nixon took the U.S. off the gold standard. Starting in 1971, U.S. dollars no longer needed to be backed by gold. In other words, it gave the Federal Reserve free rein to print as many dollars as it wanted. And as anyone who has taken an economics course knows... when more dollars in the system chase a fixed number of goods and services, prices rise. This one policy shift unleashed massive amounts of inflation... Without it, we would all be much wealthier today. And without the increases in productivity, prices would be much higher. But as the above chart shows, the true amount of inflation has been mostly hidden from the average worker. With the massive increases in productivity, his dollar should be able to buy more. But it doesn't... and he's none the wiser. According to the Fed, inflation has averaged around 1.9% per year since 2000. Those numbers are based on the central bank's preferred inflation gauge – called the personal consumption expenditures ("PCE") index. But inflation is headed much higher. It is already above that today. The most recent PCE reading was 3.9% in May... nearly double the Fed's stated goal of 2% inflation over the long run. The Fed says this is only temporary, and that it's nothing to worry about. I don't buy it. Just look at our money supply. The U.S. "M2" money supply – which includes cash, checking and savings accounts, money-market accounts, and mutual funds – is up 33% since the end of 2019. Our more liquid "M1" money supply – which is coins and currency in circulation plus checking accounts – is up 378% since the end of 2019. We've never seen a steep rise in the money supply like this in such a short time... Since the start of the COVID-19 pandemic, the Fed has committed to printing more than $6 trillion to support its stimulus programs. That's more than three times the amount of money that the central bank spent bailing out the U.S. economy during the last financial crisis. The government is printing and spending cash like it's Monopoly money. Any rational human also knows that this game can't go on forever... We're fast approaching a tipping point where it will be "game over" for the Fed. Once the Fed realizes that today's high inflation isn't going away anytime soon, the printing party will end abruptly. That's because the government's only way to fight inflation is through raising interest rates or raising taxes. And neither of those outcomes is good for the markets. And even if the Fed doesn't act, the free market will. Consumers don't have much power to combat rising prices – but creditors do... Creditors can demand higher interest rates – and they will... Inflation makes the dollars that the creditors will get paid in the future worth less. And their only tool to combat this evaporation of future income is through higher interest rates. Here's the bottom line... While I don't know for certain exactly when it will happen, higher interest rates will be the bubble-popping pin for both the stock and bond markets. Higher interest rates make stocks less valuable. Many investors will sell them in favor of safer, higher-yielding fixed-income securities. Higher interest rates are also a problem for another reason... They cost companies more to service their debt. And as I explained yesterday, servicing debt is already an enormous problem for many companies today. Investors already fear rising inflation and climbing interest rates. A wave of bankruptcies – which is already underway, by the way – will create even more fear in the markets. As that happens, investors will dump risky, overleveraged stocks. And they'll dump corporate bonds... causing bond prices to plummet and interest rates to go even higher. (The prices of bonds and interest rates are inversely related... So as prices fall, yields rise.) The chain reaction will continue... With more companies defaulting on their debt, banks will tighten credit. And that will lead to even more bankruptcies. That's why I believe we're on the verge of the next credit crisis... Unprepared investors will be wiped out. Fortunately, you don't have to be one of the victims... You see, there is a way to make big returns as the next crisis unfolds, completely outside of stocks. The coming wave of bankruptcies opens the door for tremendous profit-making potential, if you know what you're doing... Some of the world's greatest investors wait for moments like this... billionaires like Warren Buffett... John Paulson... Paul Singer... Andy Beal... Sam Zell... and Wilbur Ross. These guys do the exact opposite of most investors. While everyone else is chasing prices higher in the late-stage bull market euphoria, these billionaires are busy raising cash. Then, when the crisis unfolds, they pounce. They use a little-known type of investment – a type of corporate bond called a distressed bond – to make more money than you ever thought possible. It's sophisticated – and most folks know nothing about it... It's a way to boost your profits completely outside of stocks... with the potential for equity-like capital gains... and with far, far less risk than individual stocks... The key to this type of investment is knowing which bonds will pay you, and which ones won't. If you can find distressed bonds that you know will be paid in full at maturity, you can make massive, equity-like returns with far less risk than investing in the stock market. That's where we come in... In my Stansberry's Credit Opportunities advisory, my colleague Bill McGilton and I tell you which distressed bonds are safe to own, allowing you to earn huge, safe profits. Finding truly great, safe distressed bonds with extraordinary returns is much easier in moments of crisis... like the one we're about to enter. The coming crisis will make it possible to buy high-quality bonds for $0.60... $0.50... even as little as $0.30 on the dollar. Because corporate debt is larger and more burdensome than ever before, the coming crisis will be far worse than the last financial crisis. You could see some of the best opportunities of your lifetime in the coming months and years. In fact, how you prepare for this crisis could be the single most important factor in your financial security for the next decade. Learn more here. Regards, Mike DiBiase

July 30, 2021 If someone forwarded you this e-mail and you would like to be added to my e-mail list to receive e-mails like this every weekday, simply sign up here. |

|

Post a Comment

Post a Comment