Don't Let the Calm Fool YouBy Mike DiBiase  Greed in a world full of growing risk... It's a recipe for disaster. Greed in a world full of growing risk... It's a recipe for disaster.

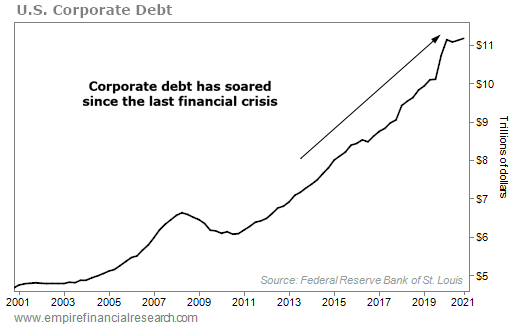

And yet, the majority of investors are falling into this trap today... They're reaching for yield wherever they can find it, blindly ignoring risks, and chasing prices higher. High-yield (or "junk") bonds are a perfect example... Junk bonds are the riskiest of corporate bonds (loans made to companies by investors). By definition, they're supposed to give investors higher yields to compensate for higher risk. Yet these bonds yield just around 4% today, on average – a historic low. (Remember, bond yields and prices move inversely... So a low yield means that the price is soaring.) The paltry yield on these bonds isn't nearly enough to compensate investors for the credit losses that they face... Historically, the average default rate of companies with junk credit ratings is around 4%. And today, there is much more risk than ever before in corporate debt as the world tries to dig out of a recession and a pandemic. But bond investors either aren't seeing the warning signs today – or they're just looking the other way as the mainstream media dishes out almost nothing but rosy news... COVID-19 vaccines are being distributed across the globe, and the end of the pandemic appears in sight. Stock markets are at all-time highs, and the U.S. economy is expected to grow 4.2% this year. Bond investors are buying what the media is selling... They're more complacent today than before the COVID-19 pandemic. You can see the proof in something called the high-yield credit spread... The high-yield credit spread measures the difference between the average yield of junk-rated corporate debt and the yield of similar-duration "risk-free" U.S. Treasury notes. When the spread is high, corporate bonds are cheap and their yields are high. But when it's low, like it is today, mostly everything is expensive. The high-yield credit spread currently sits at around 320 basis points ("bps"). That means junk bonds only yield 3.2 percentage points more than U.S. Treasury notes. Before the pandemic, the spread was around 400 bps. It briefly soared to as high as 1,100 bps last spring at the onset of the pandemic. But it has since fallen to near-historic lows. To put it simply, bond investors are overlooking massive risks in the world today... For starters, we aren't finished with the COVID-19 nightmare yet. Despite the distribution of vaccines, cases and deaths have been rising once again. New, more infectious strains of the virus like the delta variant are causing lockdowns in parts of the world once again. Meanwhile, on the financial front, U.S. corporate debt – which was already at all-time highs before the pandemic – has ballooned even higher since then. It now tops $11 trillion... It has nearly doubled since the last financial crisis. And at the same time, credit quality is at an all-time low. Many companies are choking on their debt. Even with today's ultra-low interest rates, this debt is not sustainable... A lot of businesses – especially in the travel, entertainment, retail, and restaurant industries – are still struggling. The pandemic has created winners and losers... And many of the losers are in grave danger of going bankrupt today. The number of "zombie" companies is at an all-time high... and growing. Zombies don't earn enough profits to pay for the interest on their debt. These companies are only kept alive by creditors willing to lend them more money to pay off their debt as it comes due. The number of zombie companies now accounts for nearly 25% of the largest publicly traded companies in the U.S. That's more than 700 zombies. Think about that... one out of every four companies can't even afford to pay the interest on their debt. And now, the corporate bond market's safety net has been removed... I'm talking about the program for the government to buy (mostly investment-grade) corporate bonds from the first stimulus package in 2020, which expired last December. That means the corporate-bond market is no longer being propped up by the government... Even with the government's backing, 146 U.S. companies defaulted on their debt last year. So although everything might appear rosy on the surface, if you dig a little deeper, you'll find warning signs... and they're getting worse. All of this leads me to believe that... 2022 will be the year when the corporate credit bubble bursts. When that happens, credit will dry up... Corporate defaults will soar... Fear will surge... Investors will dump their bonds into illiquid markets... And bond prices will fall off a cliff. Even safe bonds – those issued by companies in no danger of going bankrupt – will trade at large discounts to par value ($1,000 per bond). I expect the default rate to soar to at least 12% next year. That would make this crisis much worse than the last one... At that rate, another 265 companies will default, blowing past the 170 companies that defaulted in 2009 during the previous credit collapse. And in short, based on market cycles, we're long overdue for the next crisis... You see, credit cycles typically last eight to 10 years. You can identify them when the default rate rises above 10%. But the last collapse occurred 13 years ago, back in 2008. This situation simply can't last forever... no matter how much the Fed tries to save the day. The high-yield credit spread will eventually widen as more companies default on their debt. Of course, as the federal government showed in 2020, it will do whatever it takes to save the U.S. economy. That won't change under President Joe Biden's administration. It's possible that the Fed and the U.S. Treasury could kick the can further down the road... They could start to buy corporate debt once again, even junk bonds this time. The Fed could even cut the benchmark interest rate below zero. That might be enough to keep credit flowing to the riskiest companies... temporarily. But it would only delay the inevitable. They can't stop the credit bubble from bursting. All of this debt must be either repaid or written off. And we know much of it will never be repaid. Regardless of when it finally happens, we'll be ready to help you make big profits... In our corporate bond newsletter, Stansberry's Credit Opportunities, my colleague Bill McGilton and I keep our readers updated on what's happening in the credit markets... and we search for the best, lowest-risk ways to profit in the space. Some of the best opportunities of your lifetime could unfold in the months and years ahead. And it's critical to prepare for the crisis that will inevitably come. Get the details right here. Regards, Mike DiBiase

September 2, 2021 If someone forwarded you this e-mail and you would like to be added to my e-mail list to receive e-mails like this every weekday, simply sign up here. |

|

Post a Comment

Post a Comment