The 2 Biggest Dividend Investing Pitfalls to Avoid |

Money & Markets Daily,

I’m what you would call a social butterfly. As my grandmother once told me … I could talk to anyone and make friends instantly.

I was in the grocery store the other day, and I met a man named Robert.

He just retired as a college professor up north. Robert and his wife Rhonda moved to Florida to take advantage of the abundant sunshine, the Atlantic Ocean and an excellent overall quality of life.

In talking to Robert, I learned that his retirement dream wasn’t going as well as he expected. Money was tight.

Let’s be honest … Florida isn’t cheap.

He and Rhonda were living off his pension, but it simply wasn’t enough to allow them to take advantage of all that retirement had to offer. He mentioned he hadn’t seen his grandchildren in two years.

It was heartbreaking.

During our conversation, he mentioned investing in dividend stocks to earn more income and help with their situation.

That conversation got me thinking about whether dividend stock investing was Robert’s best option.

| From our Partners at Banyan Hill Publishing. $15.7 billion is at stake — and the best chance you’ll have at claiming your fair share … and becoming one of America’s next big winners … is to take these three simple steps before June 30. Click for details. |

The Blind Chase for High Yield

One of the first things to look at when making potential investments is the dividend yield.

This is a simple percentage that shows how much income you earn in dividend payouts for every dollar you invest in the stock. It’s calculated by dividing the annual dividends per share by the price per share.

If you consider a stock trading at $20 per share with a dividend yield of 5%, you can expect a dividend payout of $1 per share per year.

Logic tells us that the higher the dividend yield, the higher the dividend payout.

But you have to look deeper because there may be a nefarious reason behind a high yield.

First, dividends are payments of a percentage of company profits to those who own the stock.

Companies use profits to invest back into the operations of business.

So if a stock you're invested in has a high dividend yield, that company has less money to invest in growth.

A high yield could also signal that management doesn’t see an upside in reinvesting profits, so they opt for a high dividend instead. That’s not necessarily a good thing for the investor, as growth sustains a solid dividend payout.

High yields can also signal a stock that's in trouble.

Because the yield is relative to the price of a stock, a high yield could signal the stock has fallen. The company posts a high dividend yield on paper, but it’s because the stock is on the decline and profits are faltering.

Dividend Investing Is Capital Intensive

Let’s say you are retired, living off your benefits … but those benefits only cover your base expenses (think mortgage, food, gas, etc.).

To live comfortably, you need an additional $1,500 per month … or $18,000 per year after the government takes its cut.

After extensive research (including using the Green Zone Power Ratings system… wink, wink), you find XYZ Inc., which pays a 5% dividend on a stock trading at $10 per share.

The big question is: How much do you need to invest in XYZ Inc. to reach your $1,500-per-month dividend goal?

Follow me here because this is where it gets a little complicated.

Because the government takes a cut of dividends paid out (let’s assume it’s 30%), you actually have to bring in $25,714 in gross dividends each year ($18,000 divided by 0.7).

If you own 100 shares at $10 per share, a 5% dividend would pay you $5.

To reach your monthly dividend goal with a $10 stock paying a 5% dividend yield, you need to invest $517,280 ($25,714 divided by the yield of 0.05).

That's a ton of capital you'd need to be comfortable in your golden years!

| Mike Carr is in the top 1% of analysts worldwide. And now, leveraging his decades as a computer scientist for the U.S. Government… helping to develop the first generation of artificial intelligence…

He engineered an algorithmic system… which laid out a strategy that had the power to grow an account 199% over the last year.

And on April 25, 1 p.m. ET… he’s laying out exactly how it works.

Click here for full details. |

A Better Way to Reach Your Retirement Goals

Don’t get me wrong; dividend investing can give you a massive leg up in retirement. And there are plenty of fantastic dividend-paying stocks out there.

But, as I showed you, it takes a lot to achieve a significant and sustainable payout.

That's why my friend, colleague and Money & Markets chief market technician, Mike Carr, has developed a strategy with a 95% win rate and the power to grow your account by 199% in a little over a year.

He’s investing $30,000 of his own money in this strategy to pursue his goal of $1,500 in profits … per week, not per month.

That’s the potential to earn 4X the retirement goal I just told you about with considerably less capital to start.

If you don’t have $30,000, that’s OK. You can actually start using this system with as little as $470 in your brokerage account.

It’s bold … it’s ambitious … but a 95% win rate with the potential to grow your account by 199% is something you can’t pass up.

And Mike’s ready to help you achieve what you might’ve thought wasn’t possible.

He's putting the final touches on this new strategy, and seats for his upcoming presentation are limited. Click here to reserve your place NOW. He'll have all the details for you at 1 p.m. ET on Thursday, April 25…

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets Daily

The Fed's Biggest Problem

Interest rates might now be beyond the Federal Reserve's ability to control. The U.S. central bank controls monetary policy, sets key rates, and ensures there is enough money in circulation for the economy to function. Congress and the president share responsibility for fiscal policy and the amount of money the government spends.

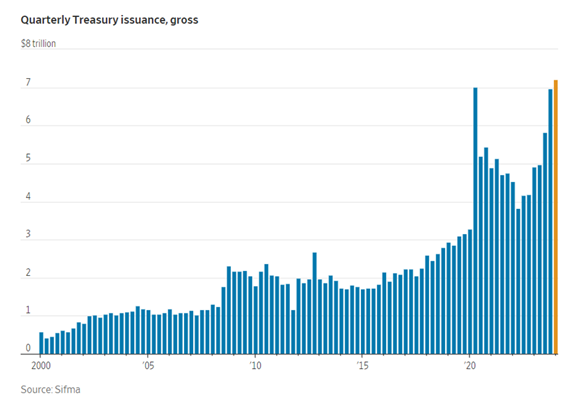

After decades of deficit spending, fiscal policy is closer to the inevitable crash everyone knows lies ahead. To fund deficits, the Treasury Department issues debt. And its doing so at a record-breaking pace right now.

According to The Wall Street Journal:

In the first three months of 2024, the U.S. sold $7.2 trillion of debt, the largest quarterly total on record. That surpasses the second quarter of 2020, when the government was financing a wave of Covid-19 stimulus. It also builds on a record $23 trillion of Treasurys issued last year, which raised $2.4 trillion of cash, after accounting for maturing bonds.

The chart below shows this. With unemployment at 3.8%, the economy is good. Debt should be decreasing, not growing at record highs. This is putting upward pressure on interest rates and might make it impossible for the Fed to use monetary policy to offset risks when the economy slows.

— Mike Carr, Chief Market Technician, Money & Markets

(Click here to view larger image.)

Check Out More From Money & Markets Daily:

Post a Comment

Post a Comment