04/29/2025 | Unsubscribe |

Mission: Ultimate Alerts was designed for active and passive US investors to notify you about short-term and long-term risks and opportunities. Our mission is to provide you with an objective and historically accurate understanding of financial markets, macroeconomics and how it all affects your saving and investing. |

|

|

Good Morning! |

Here are some important charts and ideas capturing the latest trends in US markets to help you understand what is happening from multiple different perspectives: |

| Vincent Deluard @VincentDeluard |  |

| |

📢Tax Collection Update & Why I Fade the Cuts 📢 In March I had warned that tax collections were coming in slower than last year, which confirmed my case for a March bear market (See" Beware Ides the of March": ) .. But April is stronger, with 8.4% growth | Vincent Deluard @VincentDeluard "Nasty inflation surprises in January and February followed by a growth soft patch in the spring could make investors question the wisdom of paying 38 times for the cyclically adjusted earnings of the S&P 500 index." Beware the Ides of March - Dec 17, 2024 💪My 2024 outlook is |

| |  | | | 5:26 PM • Apr 23, 2025 | | | | | | 68 Likes 10 Retweets | 4 Replies |

|

|

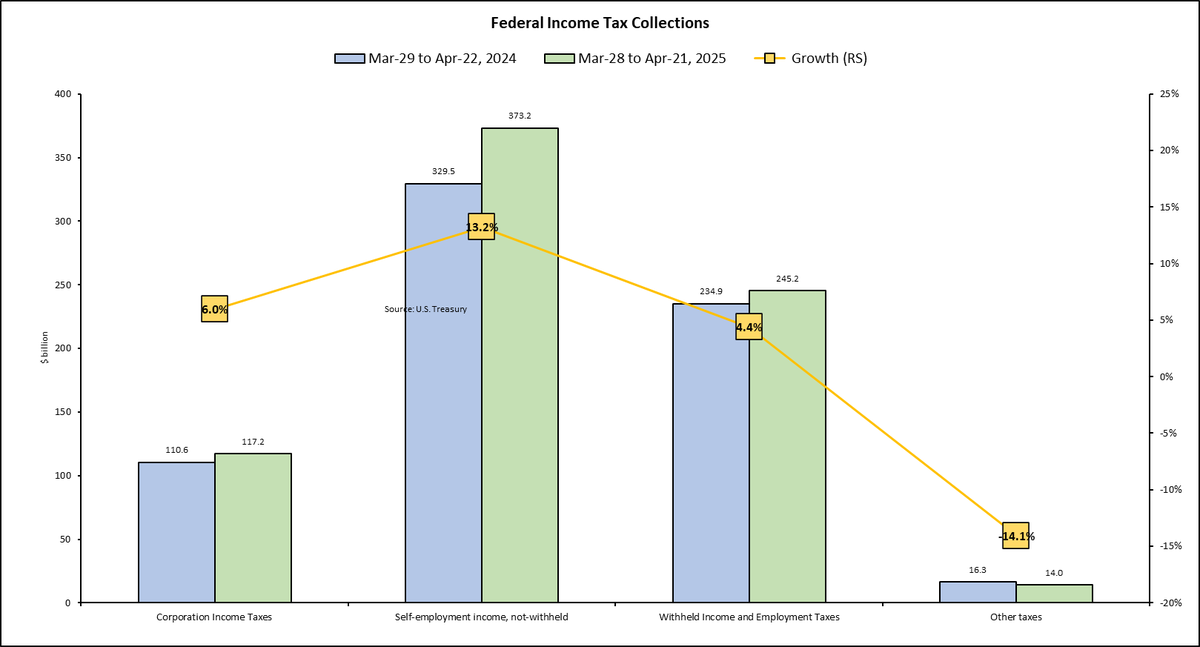

📊 Federal Tax Collection Snapshot (Mar 28–Apr 21, 2025 vs. same period 2024) |

Total tax collections up +8.4% YoY — April bounced back after a weaker March. Self-employment taxes up +13.2% — strong activity in the gig/freelance sector. Withheld employment taxes up +4.4% — payrolls still expanding, though growth is slowing. Corporate taxes up +6.0% — businesses are still profitable. Other taxes down -14.1% — likely tied to lower imports and customs issues.

|

🧠 Analyst Insight (Vincent Deluard's View) |

April's strong receipts undercut the argument for imminent Fed rate cuts. The labor market remains tight — firms are "hoarding" workers, not laying them off. Tariffs are failing to boost customs revenue significantly; enforcement is inconsistent across industries. Overall, The Economy may slow, but it is likely heading toward stagflation, not recession (at least according to tax collections).

|

💼 What This Could Mean for You |

Don't expect rate cuts too soon — borrowing costs may stay higher through mid-2025. Investors: Favor companies with strong cash flow and pricing power in a stagflation scenario. Savers: High interest rates still support solid yields in money markets and Treasuries. Job security remains decent, but wage growth might not keep pace with inflation long-term.

|

| Marko Papic @Geo_papic | |

| |

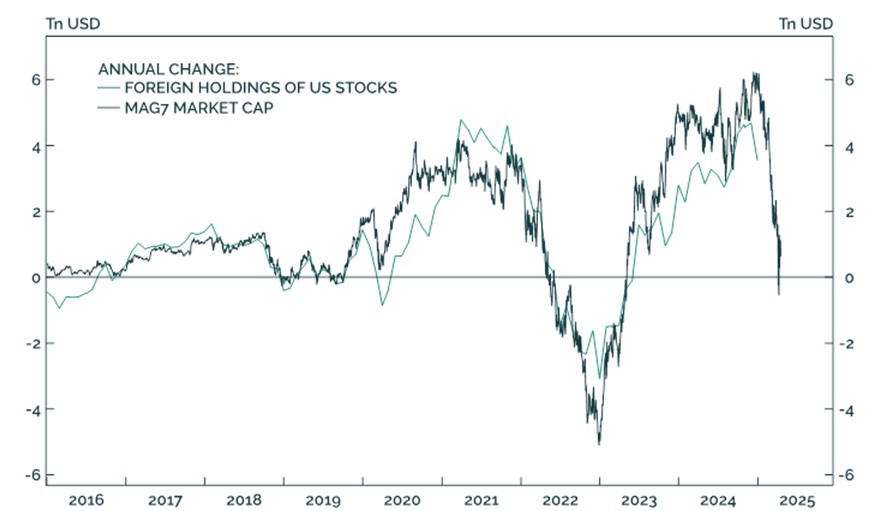

One of the best charts from a good friend of mine who for compliance reasons can't receive a shout out on this platform. It basically shows that the EXODUS has not even started folks. | |  | | | 9:11 AM • Apr 26, 2025 | | | | | | 922 Likes 194 Retweets | 92 Replies |

|

|

📊 Key Takeaways from the Chart |

The chart compares: 🟩 Foreign Holdings of US Stocks (annual change, green line) ⚫ MAG7 Market Cap (annual change, black line – the 7 mega-cap tech giants)

Recent collapse in both: Implication: The relationship suggests that foreign flows and MAG7 valuations could be linked. Papic's Message: This drop isn't the "exodus" yet — implying that much larger foreign selling could still come.

|

🔄 Counterpoints & Alternative Perspectives |

🟠 Correlation ≠ causation — MAG7 and foreign flows may be reacting to broader macro shifts (e.g., rates, dollar weakness), not just each other. 🟣 Domestic buying may offset foreign exits, especially via ETFs and retirement flows. 🟡 Foreign "selling" could reflect valuation base effects, not actual capital flight. "Valuation base effects" means: if U.S. assets (like stocks) become more expensive compared to others (say, European or Asian stocks), foreigners might naturally reduce their holdings because things look expensive — not because they are scared or trying to move money out urgently.

🟤 Geopolitics plays a role — trade policy and currency weakness/strength may deter reallocating capital elsewhere.

|

💼 What This Could Mean for You |

Last decade: Even though U.S. stocks and assets were expensive (high valuations) and the U.S. dollar was strong, foreign investors still bought heavily — because U.S. assets looked safe and returns were attractive. Now: The world is changing — we're possibly moving into a period of: Result: This double negative could make foreigners less eager to invest in the U.S.

|

🏦 Why this matters: |

Foreign buying has been a big support for U.S. stocks and bonds. If foreigners slow down or sell, it could pressure U.S. asset prices lower.

|

In short:

✅ Past: High prices + strong dollar didn't scare foreigners.

🚫 Future: Weak dollar + falling prices could finally turn foreigners away. |

| Darth Powell @VladTheInflator | |

| |

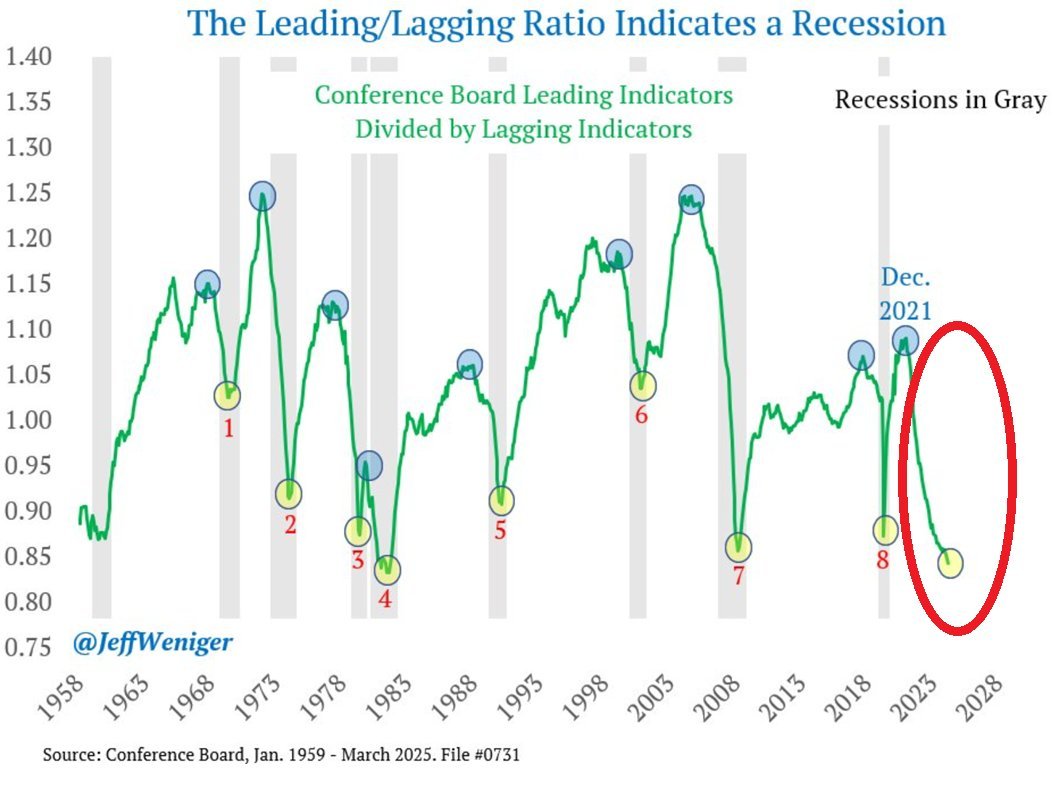

Leading recession indicator hits lowest level since 2008 | |  | | | 3:51 PM • Apr 26, 2025 | | | | | | 1.89K Likes 335 Retweets | 90 Replies |

|

|

📊 Key Takeaways from the Leading/Lagging Ratio Chart |

Leading indicators relative to lagging indicators have collapsed sharply, hitting the lowest level since the 2008 financial crisis. Historically, every sharp downturn in this ratio (circled) has been followed by a U.S. recession (gray bars). The last major peak was around December 2021, indicating economic momentum peaked over three years ago. Current reading is deeply negative — typically associated with recessions in the past (seen in cycles: 1969, 1974, 1980, 1990, 2001, 2008, 2020).

|

💼 What This Could Mean for You |

Prepare for more volatility — markets tend to weaken before and during economic slowdowns. Opportunities will come — sharp drops often lead to attractive entry points for investors. Emergency fund importance — having a liquidity buffer will be crucial if a recession occurs and layoffs happen.

|

| Anas Alhajji @anasalhajji | |

| |

With WTI at $50 for 16 months: 1. Shale will survive.

2. OPEC+ members will survive.

3. Canadian oil companies will survive.

4. Offshore will survive.

5- Shipping companies will survive

6- Service companies will suffer Key points: 1. Oil majors in shale plays will make profit | |  | | | 8:20 PM • Apr 26, 2025 | | | | | | 307 Likes 46 Retweets | 51 Replies |

|

|

📊 Key Takeaways on Oil Market at $50 WTI for 16 Months |

Shale producers will survive — U.S. shale breakevens have improved; most large players can profit at ~$50. OPEC+ members will survive — many need higher prices, but can withstand $50 short-term with fiscal adjustments. Canadian oil companies will survive, especially low-cost oil sands producers with existing infrastructure. Offshore production will survive — large projects will already be funded, and the focus will be on managing operational costs. Shipping companies will survive — crude transport remains essential, though margins may tighten. Oilfield service companies will suffer — lower prices discourage new drilling, reducing demand for services.

|

💼 What This Could Mean for You |

Large-cap integrated oil companies (with refining and chemicals arms) may offer safer exposure. Oil services ETFs may remain weak unless drilling activity rebounds. Expect more consolidation — mergers among weaker oilfield services and exploration firms likely.

|

| JE$US @WallStJesus | |

| |

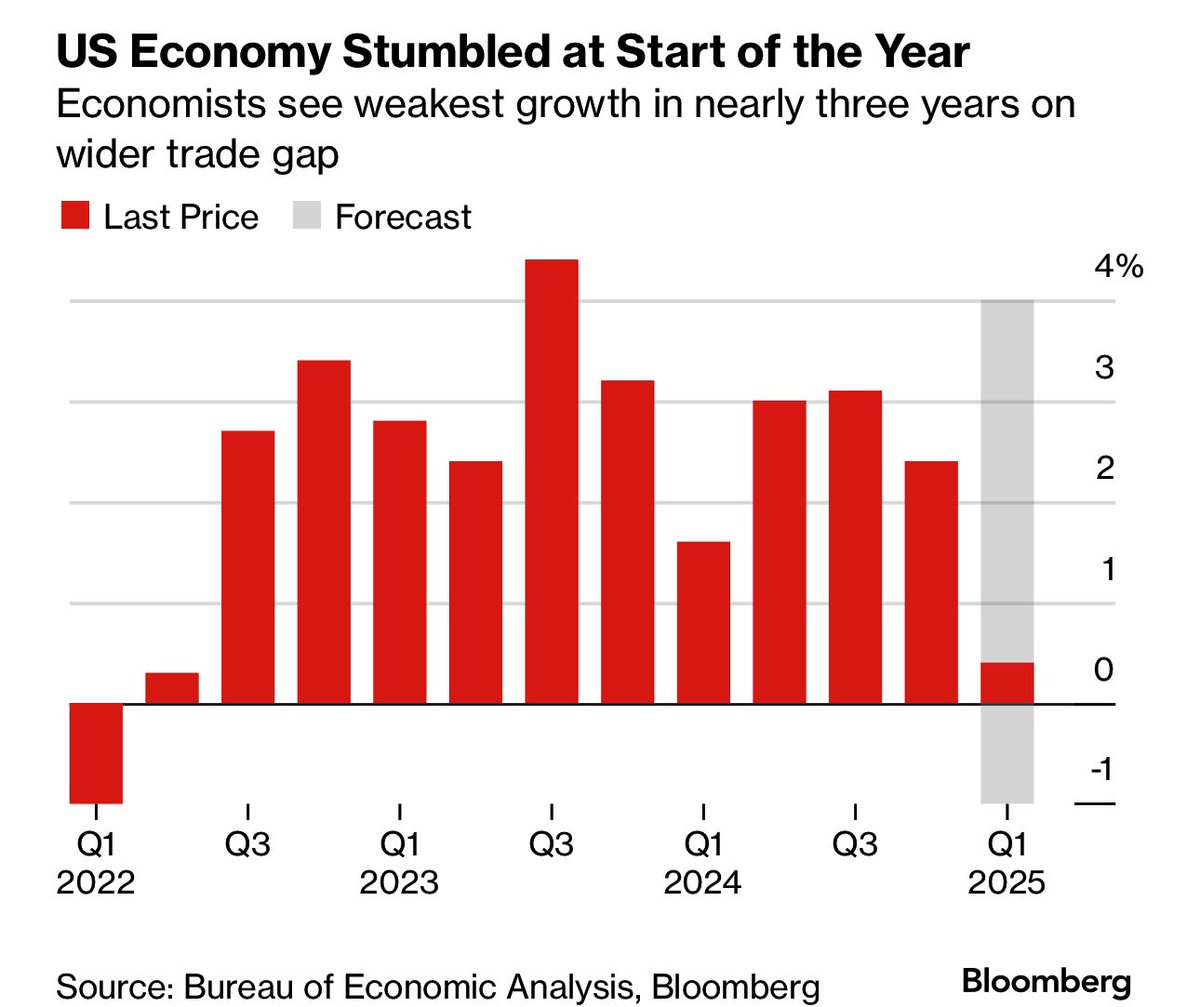

US Economy Was Already Sputtering Before Trade Pain Kicked In bloomberg.com/news/articles/… | |  | | | 8:44 PM • Apr 26, 2025 | | | | | | 14 Likes 5 Retweets | 21 Replies |

|

|

📊 Key Takeaways from the Chart |

Q1 2025 GDP growth is forecasted to be close to 0%, the weakest in nearly three years. US economic growth had slowed starting late 2024, even before the widening trade gap. Past trend: Growth was relatively strong from late 2022 to mid-2024, but momentum faded afterward. Trade imbalance is now adding additional pressure to an already softening economy.

|

🔄 Counterpoints & Alternative Perspectives |

🟠 One quarter doesn't define a recession — Q1 could be a soft patch before a rebound later in 2025 (Our View: unlikely to be the case - more likely prolonged for 2025 and 2026). 🔵 Fed pivot could help — if weakness persists, the Federal Reserve might cut rates, supporting growth (Our View: would also support inflation, not good) 🟤 Inventory adjustments often distort early-year GDP numbers — revisions later could paint a better picture.

|

💼 What This Could Mean for You |

Be cautious with growth-sensitive assets — tech (high inflation is what hurts), small caps, and cyclicals could underperform if growth remains weak. The bond market may benefit (lower yields) from slower growth, strengthening the case for bonds and rate-sensitive assets Stay diversified — uncertainty in early 2025 suggests keeping a balance between defensive (bonds) and growth assets (stocks).

|

That's it for today! |

Please reply to this email if today's newsletter helped you in any way. Your feedback is super important to us to continue improving the quality and depth of the information that you receive. |

|

|

📌 Did we land in your inbox? Please make sure our emails arrive in your inbox where you can see them immediately. |

|

Best Regards, |

Ultimate Alerts Team |

|

Disclaimer |

The content distributed by UltimateAlerts.com is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Stocks/Assets featured in this newsletter may be owned by owners/operators of this website, which could impact our ability to remain unbiased. If you click on an affiliate link the website owner may receive compensation. Although we have sent you this email, UltimateAlerts.com does NOT specifically endorse this product nor is it responsible for the content of this advertisement. |

Please read and accept full disclaimer and privacy policy before reading any of our content: www.ultimatealerts.com/c/disclaimer/ and www.ultimatealerts.com/c/privacy-policy |

Post a Comment

Post a Comment