04/30/2025 | Unsubscribe |

Mission: Ultimate Alerts was designed for active and passive US investors to notify you about short-term and long-term risks and opportunities. Our mission is to provide you with an objective and historically accurate understanding of financial markets, macroeconomics and how it all affects your saving and investing. |

|

|

Good Morning! |

Here are some important charts and ideas capturing the latest trends in US markets to help you understand what is happening from multiple different perspectives: |

| Augur Infinity @AugurInfinity |  |

| |

🇺🇸 US financial conditions have eased over the past two weeks, but remain tighter than earlier in the year. | |  | | | 1:30 PM • Apr 28, 2025 | | | | | | 7 Likes 0 Retweets | 2 Replies |

|

|

📊 Key Takeaways |

|

🔄 Counterpoints & Alternative Perspectives |

🟠 Short-term easing may reverse — if inflation surprises or global risk-off sentiment returns. 🟡 Still restrictive vs. history — easing isn't the same as being loose; borrowing costs remain elevated. 🔵 Fed may delay cuts — easing conditions may give the Fed more time to watch data before acting. 🟣 Market-led easing ≠ broad economy relief — small businesses and consumers still face tighter lending standards.

|

💼 What This Could Mean for You |

Volatility may ease near-term — looser conditions often support risk assets (stocks, credit). Risk-on assets may bounce, but stay cautious — conditions are better, not great. Bond markets may still offer an opportunity if credit conditions ease further. Watch credit spreads and FX — their movement is key to whether easing continues or reverses.

|

| Lisa Abramowicz @lisaabramowicz1 | |

| |

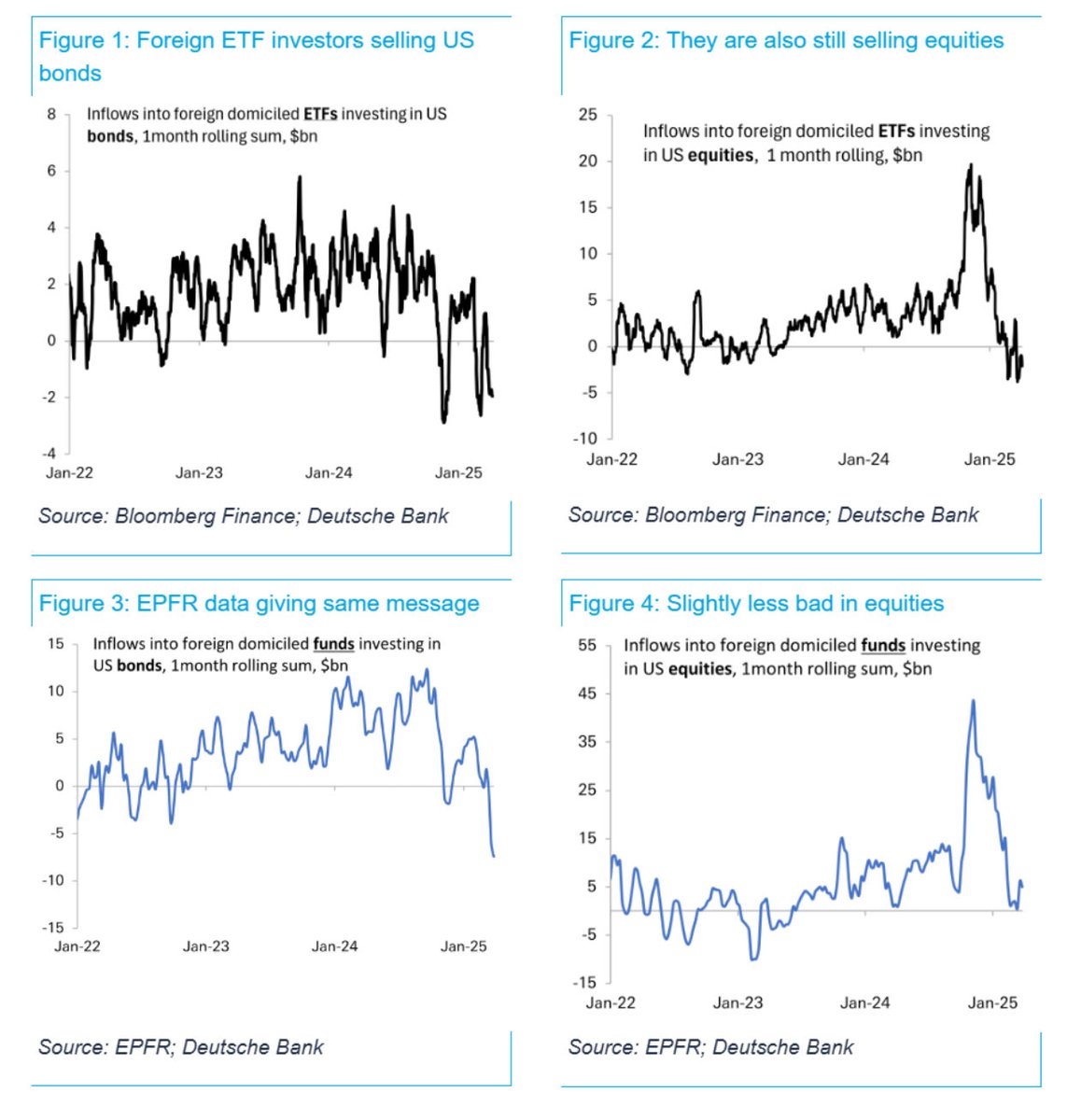

"There has been a sharp stop of foreign investor inflow into US bond and equity markets over the last 2 months…The flow evidence so far points to an, at best, very rapid slowing in US capital inflows and, at worst, continued active disinvestment from US assets:" DB's Saravelos | |  | | | 9:11 PM • Apr 28, 2025 | | | | | | 1.01K Likes 361 Retweets | 74 Replies |

|

|

📊 Key Takeaways: Foreign Investors Are Pulling Back from US Markets |

🧾 Bonds |

|

📉 Equities |

Figure 2 & 4: Foreign ETF flows into US equities are also declining, falling from 2024 highs. Fund flows (Figure 4) are "less bad" but still show significant cooling since January 2025.

|

🔄 Alternative Perspectives & Counterpoints |

🟠 Temporary pullback? Investors may pause due to macro uncertainty or wait for better entry points. 🟡 Currency hedging effects — a stronger dollar in early 2024 may have deterred inflows; a weaker dollar now could reverse the trend. 🔵 Domestic demand may offset this — US-based investors and institutions could absorb some foreign selling. 🟣 Rotation, not exit, money may reallocate toward non-US assets due to valuation or policy shifts.

|

💼 What This Could Mean for You |

Markets may stay volatile — declining foreign support can amplify downside swings in bonds and stocks. Watch the dollar and yields — if disinvestment continues, it could pressure the dollar and drive higher rates. Gold and international assets may benefit if foreign capital rotates away from US holdings. Investors should stay diversified — consider non-US exposure, commodities, or defensive allocations to weather capital outflows.

|

| Neil Sethi @neilksethi | |

| |

Since 1950 first half of May has been the 4th weakest half of the year for the SPX with a slight decline (Goldman). | |  | | | 11:20 AM • Apr 28, 2025 | | | | | | 22 Likes 8 Retweets | 3 Replies |

|

|

📊 Key Takeaways from the Chart (Goldman Sachs) |

Timeframe: The Chart shows median 2-week S&P 500 returns for each half-month period since 1950. Highlighted Insight: The first half of May (1H_May) ranks the 4th weakest period, with a slight negative median return. Other Weak Spots: Historically weak returns also appear in: 2H_June 2H_September 1H_February

|

🔄 Counterpoints & Alternative Perspectives |

🟠 Seasonality ≠ destiny — historical averages don't guarantee future performance in any given year. 🟡 Macro backdrop matters — Fed policy, earnings, and geopolitical context can override seasonal patterns. 🔵 The first half of May's weakness may be front-loaded tax or fund rebalancing, which is not true selling pressure. 🟣 Market positioning may differ now; seasonal effects may fade in AI-led or inflation-driven markets.

|

💼 What This Could Mean for You |

Caution in early May — historically, it was a weaker stretch, so it may warrant hedging or trimming risk. Don't panic-sell — weakness is typically mild and short-term, not a sign of major trouble. Use dips strategically — May pullbacks have often led to summer rallies (1H_July is seasonally strong). Stay balanced — consider using seasonal softness to rotate or rebalance instead of exiting positions.

|

| Warren Pies @WarrenPies | |

| |

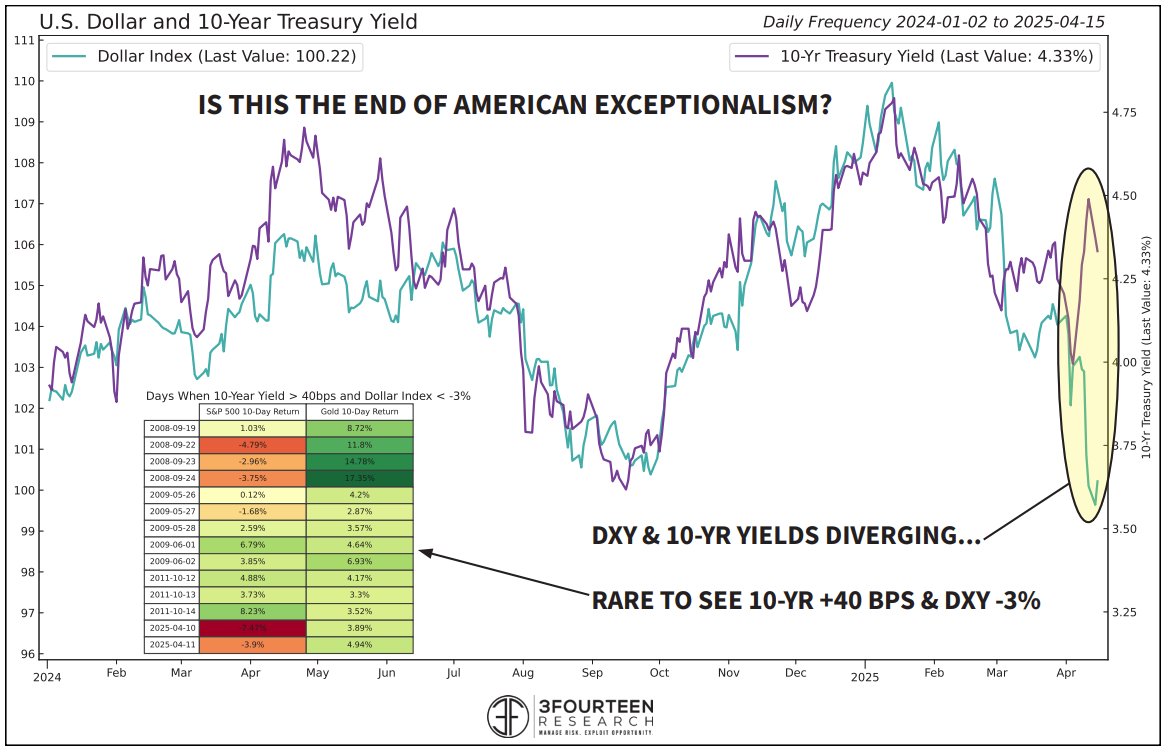

The post-"Liberation Day" cross-market price action has been unsettling and unprecedented. 1) Bonds & DXY falling together. At the height of the panic (4/10 & 11), the 10-yr had risen by 40 bps and the Dollar fell by 3%. This combination has only happened 12 days since 2000. | |  | | | 11:17 AM • Apr 21, 2025 | | | | | | 536 Likes 104 Retweets | 25 Replies |

|

|

📊 Key Takeaways from the Chart (3Fourteen Research) |

|

🧠 Interpretation & Context |

Normally, higher yields strengthen the dollar (more attractive to investors). Here, yields rose while the dollar fell, signaling a possible loss of confidence in U.S. assets or policy credibility. Gold's rise during these events shows investors shifting to non-sovereign, non-fiat assets.

|

🔄 Alternative Perspectives & Counterpoints |

🟠 Temporary dislocation? It could reflect short-term positioning, not structural change. 🟡 Geopolitical or policy-driven markets may have reacted to specific headlines unrelated to long-term trends. 🔵 Risk premiums are rising, not U.S. collapse — yields may have risen due to inflation expectations, not sovereign risk. 🟣 Foreign selling of Treasuries could push yields up while weakening the dollar.

|

💼 What This Could Mean for You |

Volatility is likely to persist — unusual cross-asset moves often precede larger shifts. Gold & commodities may outperform if confidence in fiat and U.S. assets keeps eroding. Be cautious with long-duration assets — bond volatility suggests yields may not stabilize soon. Stay diversified globally — weakening dollar and U.S. policy uncertainty may favor non-U.S. assets.

|

| Mike Zaccardi, CFA, CMT 🍖 @MikeZaccardi | |

| |

US CEO sentiment has deteriorated sharply since January. @SoberLook

dailyshotbrief.com | |  | | | 7:36 PM • Apr 21, 2025 | | | | | | 49 Likes 10 Retweets | 20 Replies |

|

|

📊 Key Takeaways (CEO Sentiment: Jan → Apr 2025) |

📈 Profit Forecasts |

|

🏗️ CapEx (Capital Expenditures) Forecasts |

|

👥 Hiring Forecasts |

|

🔄 Alternative Perspectives & Counterpoints |

🟠 Seasonal pessimism? CEOs often get cautious in Q2 before summer guidance cycles. 🟡 Macro uncertainty (Trade, policy, recession risks) may prompt a temporary pullback, not structural weakness. 🔵 Profit margins may still hold even with weaker revenue if cost-cutting accelerates. 🟣 CapEx & hiring lags GDP — firms might reverse course if the outlook improves.

|

💼 What This Could Mean for You |

Corporate caution is rising, suggesting slower earnings growth, impacting equity markets. Job growth may slow, especially in cyclical industries; consider strengthening emergency savings. Investors: Favor companies with strong balance sheets and low CapEx dependency. Watch for further downside risks in sectors reliant on capital spending or aggressive hiring (e.g., tech, construction). If sentiment reverses mid-year, markets may rebound strongly — stay nimble.

|

That's it for today! |

Please reply to this email if today's newsletter helped you in any way. Your feedback is super important to us to continue improving the quality and depth of the information that you receive. |

|

|

📌 Did we land in your inbox? Please make sure our emails arrive in your inbox where you can see them immediately. |

|

Best Regards, |

Ultimate Alerts Team |

|

Disclaimer |

The content distributed by UltimateAlerts.com is for general informational and entertainment purposes only and should not be construed as financial advice. You agree that any decision you make will be based upon an independent investigation by a certified professional. Stocks/Assets featured in this newsletter may be owned by owners/operators of this website, which could impact our ability to remain unbiased. If you click on an affiliate link the website owner may receive compensation. Although we have sent you this email, UltimateAlerts.com does NOT specifically endorse this product nor is it responsible for the content of this advertisement. Please read and accept full disclaimer and privacy policy before reading any of our content: www.ultimatealerts.com/c/disclaimer/ and www.ultimatealerts.com/c/privacy-policy |

Post a Comment

Post a Comment