| Hey there, savvy investors! This week, I'm bringing you two stocks that look messy on the surface but are absolute steals underneath – one's an AI server company everyone's panicking about before earnings, and the other's a midstream giant that just posted record results while the stock tanked. Let's dig in. Super Micro Computer (SMCI): The $50 Stock That Should Be $73So SMCI just dropped from $60 to $50, and everyone's freaking out about next week's earnings (November 4th). The preliminary revenue report showed a $1.5 billion miss, analysts are skeptical, and the momentum looks terrible. Naturally, I'm buying more. Here's what everyone's missing: That $1.5 billion "miss" wasn't lost revenue – it was moved to next quarter because management upgraded design wins. Translation: they're not losing sales; they're optimizing for bigger, better deals. The FY2026 revenue potential hasn't changed at all. The long-term story that matters: SMCI is expected to double revenue between FY2026 and FY2031. That's not hype – that's based on a proven 45%+ CAGR over the past five years across all key metrics. These guys know how to capitalize on data center tailwinds. The partnerships nobody's talking about: - Intel and Micron collaboration for quantitative trading benchmarks – opening them up to a massive $127 trillion global stock market (plus commodities and forex)

- Federal government expansion with Nvidia's help to win digitalization contracts from the world's largest spender ($7 trillion annual budget)

- New DCBBS division targeting smaller clients to complement their success with large enterprise customers

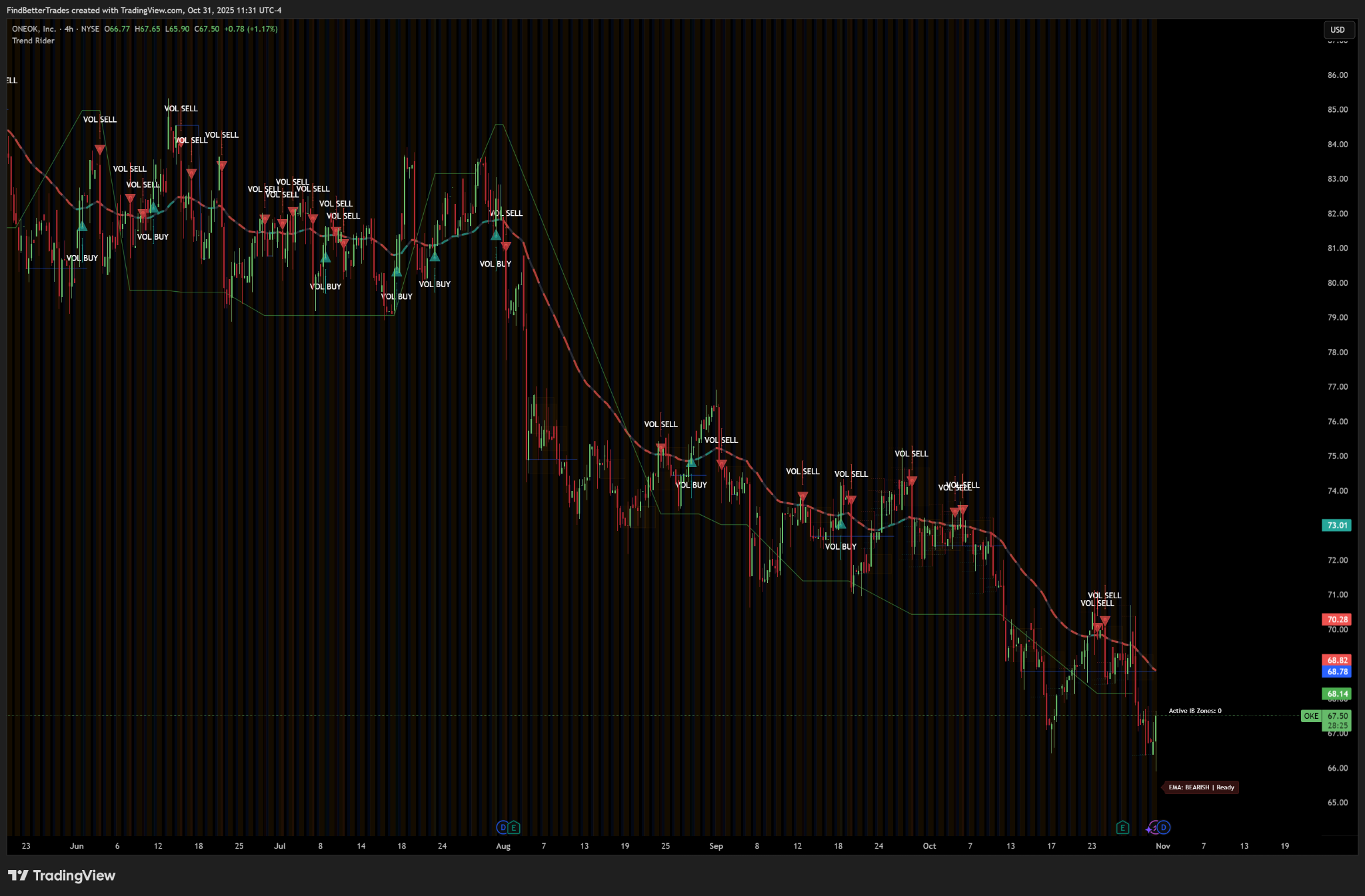

Think about that for a second. They're already dominating with hyperscalers, now they're going after the federal government AND small/medium businesses. That's three massive growth vectors most people aren't even considering. The valuation that's absolutely ridiculous: FY2027 forward P/E is just 15. For a company growing this fast? That's insane. The forward P/S ratio is below 1 – I'd challenge you to find another AI-exposed stock trading that cheaply. SMCI has improved free cash flow margins, only $5 billion in debt against a $31 billion market cap, and zero signs of distress. Using a conservative 1.4x P/S multiple (their historical average) on FY2026's $32.2 billion revenue estimate gives a fair value of $45 billion. That's 45% upside over the next year. The risks you need to know: Yes, earnings could disappoint. SMCI has missed EPS three times in the last five quarters, so the track record isn't stellar. The 14-day RSI is declining sharply, and Wall Street's ultra-conservative $53 target (below the recent $60 level) suggests analysts expect weak guidance. My strategy: I'm buying before earnings and will double down if there's a post-earnings dip. The short-term volatility is real, but at these prices with this growth trajectory? The risk/reward is too compelling to ignore. ONEOK (OKE): Record Earnings, Dead Stock, 5.9% YieldHere's a head-scratcher: ONEOK just posted record quarterly results and upgraded 2026 guidance. The stock? Down 15% while the S&P gained 14%. Sometimes Mr. Market makes zero sense. The earnings that should've sent this flying: - Net income: $940M ($1.49 EPS, beat by $0.06)

- Revenue: $8.6B (beat estimates)

- Adjusted EBITDA: $2.12B (up from $1.54B last year) – a quarterly record

- 2026 outlook: EBITDA growth nearly 10%, EPS growth over 15%

These are record numbers across the board. So why did the stock tank with the entire midstream sector? Fear. Debt concerns. Commodity price worries. All the usual suspects that don't hold up under scrutiny. The transformation Wall Street's missing: ONEOK evolved from a pure-play NGL/natural gas company into a diversified energy infrastructure beast. The EnLink and Medallion acquisitions are crushing it – NGL volumes in the Rockies up 17% year-over-year, and they're seeing $250 million in deal synergies. The debt situation everyone's worried about: Yes, Net Debt/EBITDA is at 4.5x (target is 3.5x). But here's what matters: management expects to hit that target by 2026, they've already paid down $387M in senior notes, and they repurchased another $119M at a discount. The cash flow is there, and they're executing on deleveraging. The LNG tailwind nobody's pricing in: Major U.S. LNG export terminals are coming online in 2025-2026. ONEOK's natural gas infrastructure is perfectly positioned to capture this growth as volumes surge through their system. I've been bullish on LNG, and OKE is one of the direct beneficiaries. The valuation that looks attractive: EV/EBITDA of 11.1x – lower than Kinder Morgan and Williams. FCF yield of 7.9% shows they're generating serious cash. Plus, you're getting a 5.9% dividend yield (no K-1 forms since they're a C-corp) that's grown at 5.43% CAGR over the past decade. What's next: Organic growth projects like the West Texas NGL pipeline expansion and Elk Creek will sustain growth without piling on more debt. And if they wanted to make another move, targets like Kinetik or Brazos Midstream could add massive Permian exposure. The risks to consider: They need to execute on deleveraging. If crude prices crater and producers slow drilling, volumes could drop, straining cash flow. But with their fee-based model and strong execution track record, I'm betting they hit their targets. The Week Ahead: What to WatchFor SMCI: Earnings drop November 4th. Watch for any guidance upgrades on federal contracts or new partnership announcements. If they beat EPS expectations and raise guidance, this stock could rip 20%+ in a day. For ONEOK: Monitor any updates on debt repayment progress or new LNG export terminal partnerships. With record results already announced, any positive news could break this stock out of its funk. Value Hiding in Plain SightHere's what makes this pair so compelling: both are getting hammered for reasons that don't match their fundamentals. SMCI is facing pre-earnings jitters and a revenue "miss" that wasn't really a miss. Meanwhile, they're expanding into federal contracts, quantitative trading infrastructure, and small business solutions with AI tailwinds at their back. At 15x FY2027 earnings with 45% upside? That's a gift. ONEOK just posted record results and is guiding for double-digit growth in 2026. The entire midstream sector got crushed on macro fears, but OKE is deleveraging on schedule, capturing LNG export growth, and paying you 5.9% to wait. Plus, you're getting it cheaper than peers despite similar or better growth. My take? Both offer asymmetric risk/reward. SMCI is the volatile AI play that could pop huge post-earnings or give you a better entry if it dips. ONEOK is the stable income play that's trading like it's broken when it's actually hitting on all cylinders. One's high-risk/high-reward with near-term catalysts. One's steady cash flow with a massive yield that's trading at a discount. Both deserve serious consideration depending on your risk tolerance. Which one speaks to you? The AI server play or the misunderstood midstream giant? Let me know! The Countdown Starts Now The TriSignal Scanner is live — and traders are already getting signals rolling in. But here’s the catch: the 1-Year Access option disappears this Sunday at midnight. Once it’s gone, only Lifetime Access remains. 👉 Activate your access today — and start receiving real breakout alerts this weekend. Stay sharp, Your Market Scout FindBetterTrades |

Post a Comment

Post a Comment