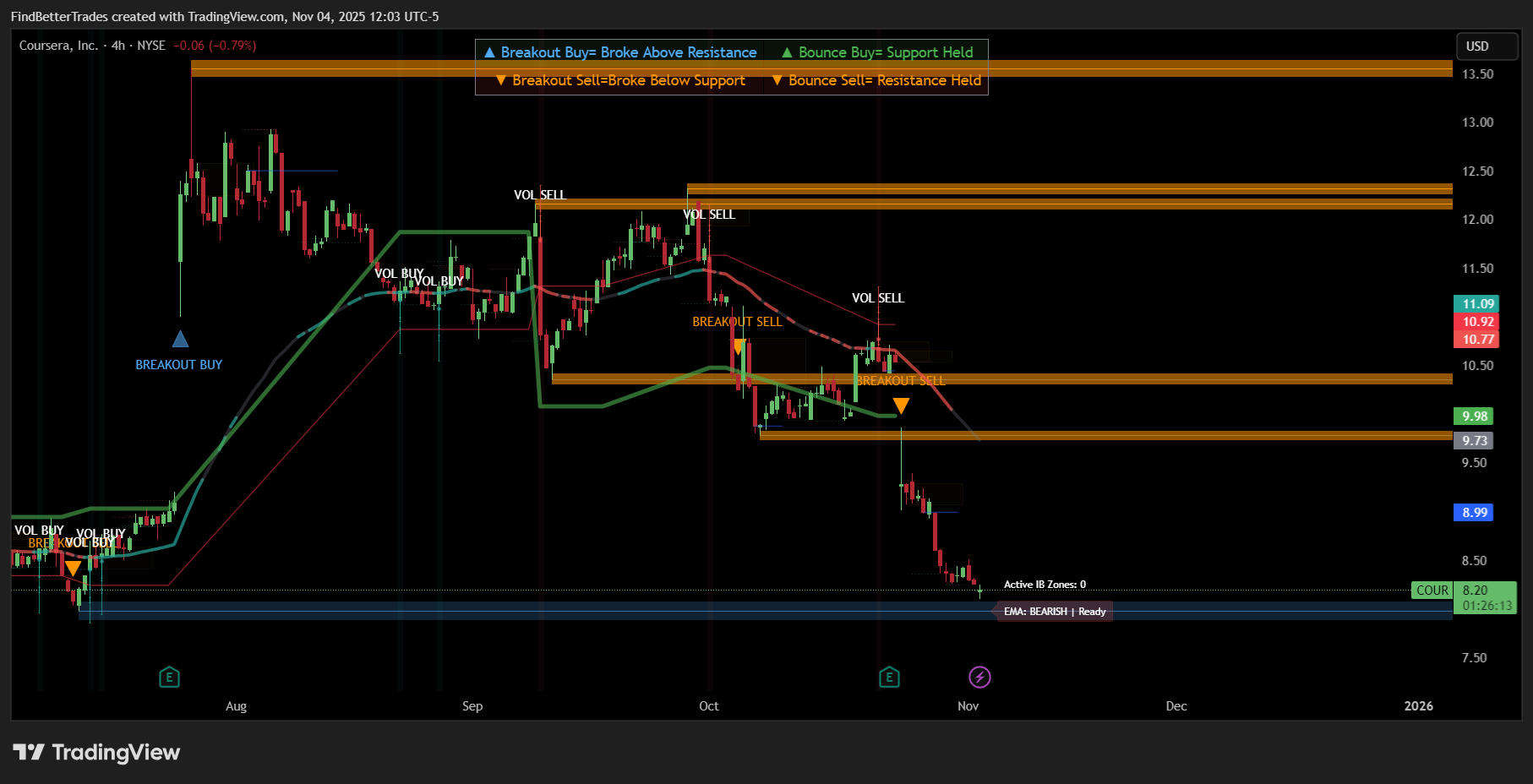

| Hey there, So Coursera just got absolutely hammered—down 20% after earnings. And you know what? The market completely overreacted. Let me ask you something: when a company raises full-year revenue guidance, maintains its EBITDA margin, and analysts don't touch their 2026 estimates... does that sound like a business that deserves to lose a fifth of its value overnight? Yeah, didn't think so. WHAT ACTUALLY HAPPENED IN Q3Look, I'm not going to sugarcoat it—the quarter was mixed. Enterprise retention rates stayed flat at 89%, which isn't great. Q4 revenue growth is expected to decelerate from 10% to somewhere between 5-8%. Those are legitimate concerns. But here's what everyone's missing: the 2026 consensus revenue estimate actually increased after earnings. It went from $785.7M to $796.6M. The EPS estimate for 2026? Still sitting at $0.45, unchanged. So let me get this straight—analysts are more confident about next year's performance, but the stock tanks 20%? That's not rational pricing. That's panic selling in a market that has zero tolerance for anything less than perfection. THE REAL STORY: AI IS REWRITING THE PLAYBOOKHere's where it gets interesting. While everyone's chasing semiconductor stocks and cloud infrastructure plays, they're completely missing the human capital angle of the AI revolution. Think about your own job for a second. How much has it changed in the past two years because of AI? What skills do you need now that you didn't need before? Now multiply that across every white-collar worker in the world. That's Coursera's market. The AI revolution isn't just about building the technology—it's about retraining the workforce to use it. And Coursera is positioned better than anyone to capitalize on this shift. WHY COURSERA OWNS THIS SPACEThe consumer battle is over, and Coursera won. They've got 191 million registered learners—up 18% year-over-year—and that's only 3% of the world's adult population. The new management team slashed prices in emerging markets like India by 60%, opening up massive growth opportunities. Who's going to compete? 2U's barely surviving bankruptcy. Udemy pivoted away from consumers. LinkedIn Learning and Skillsoft don't have the university partnerships to offer credentialed courses. Coursera has the moat, and it's getting wider. But here's the kicker: their partnership with OpenAI and ChatGPT integration isn't just a flashy press release. It's a fundamental shift in how people discover educational content. While competitors are still optimizing for Google SEO, Coursera is embedding itself directly into AI conversations. When SEO dies—and it will—Coursera will still be generating leads. REMEMBER OUR DARK CLOUD REVERSAL?Speaking of opportunities others miss—our Dark Cloud Reversal indicator has been invaluable for timing entries and exits in volatile stocks exactly like this. When sentiment gets euphoric or pessimistic beyond reason, that's when the best opportunities appear. A 20% drop on mixed-but-not-terrible earnings? That's the kind of overreaction our indicator is built to identify. Whether you're looking to catch falling knives or fade rallies, having a systematic approach to spotting reversals separates winning traders from the herd. Don't trade on emotion. Trade on pattern recognition backed by data. Technical ViewpointBlack Friday’s Smartest $7 You’ll Spend”Forget clothes. Forget gadgets. Get an indicator that can literally save your portfolio from the next market top. The Dark Cloud Reversal lights up yellow when reversals form — and plots your exact exit. 👉 Grab it now for $7 — before it goes back to full price. THE RISKS YOU NEED TO KNOWI'm not here to pump sunshine. The enterprise retention issue is real, and they just hired a new GM for that segment—which means improvement might take longer than expected. Management could also invest more heavily in AI during 2026, potentially pressuring margins like competitor Udemy is planning to do. And yes, if the consumer economy stays sluggish, that could slow growth in the near term. But here's the thing: none of these risks change the fundamental trajectory of this business. THE BOTTOM LINEBIAS: BULLISH Coursera now trades at the low end of its historical valuation—around 8.2x EV/NTM Adjusted EBITDA. You're getting a company that dominates consumer edtech, has massive growth runway internationally, and is strategically positioned for the AI-driven workforce transformation... at a discount. The thesis hasn't broken. It's just been delayed. And sometimes the best opportunities come when the market loses patience and hands you quality assets at bargain prices. The AI revolution needs infrastructure. But it also needs people who know how to use that infrastructure. Coursera is how they'll learn. This selloff is noise. The signal is clear: buy the dip. Black Friday’s Smartest $7 You’ll Spend”Forget clothes. Forget gadgets. Get an indicator that can literally save your portfolio from the next market top. The Dark Cloud Reversal lights up yellow when reversals form — and plots your exact exit. 👉 Grab it now for $7 — before it goes back to full price. Stay sharp out there, Your Trading Desk TradingStrategyGuides |

Post a Comment

Post a Comment