On a recent episode of The Joe Rogan Experience, NVIDIA CEO Jensen Huang delivered a blunt assessment of AI's next big hurdle.

It's not chips, it's electricity.

Huang told Joe Rogan that the explosive growth of AI workloads is running headlong into a new kind of bottleneck - power. The availability of electricity will ultimately shape how far and how fast AI can scale.

That's a stark departure from the narrative of hardware scarcity. A future where companies must not just innovate faster, but power their innovations sustainably, is now coming into view.

His solution? Build AI data centers in space.

In orbit, satellites can operate in near-continuous sunlight, generating up to eight times more solar power than ground-based panels. Cooling is handled naturally by the vacuum of space. And there are no land shortages, zoning rules, or grid bottlenecks.

It may sound like science fiction - but the shift is already underway.

While Google, Microsoft, Amazon and NVIDIA explore space-based AI concepts, one publicly traded company is already moving from theory to execution.

This early-entry company has partnered with aerospace firm Orbit AI to help build the blockchain verification layer for the first Orbital Cloud - an AI-enabled satellite network designed to operate securely and autonomously in orbit.

This infrastructure is intended to serve as the trust layer, allowing AI systems in space to authenticate data and coordinate workloads without relying on Earth-based oversight.

The first satellite, Genesis-1, is scheduled to launch in December 2025, with a full constellation planned by 2030.

As Big Tech pushes toward AI data centers in space, the infrastructure needed to support them is being built now.

Learn how this company is positioning

at the foundation of space-based AI infrastructure.

Capital Trends

These 3 Stocks Trade at Discounts the Market Won't Ignore Forever

Authored by Dan Schmidt. Article Posted: 1/5/2026.

Key Takeaways

- The S&P 500 posted another gain above 15% in 2025, but the market is now approaching historically concerning valuation levels.

- When valuations are elevated, slowing earnings growth is harshly punished, and investors often turn to value stocks for safety.

- These three large-cap stocks all trade well below their industry-average P/E ratios, which could help protect against market volatility in 2026.

The S&P 500 wrapped up 2025 with a total return of about 18%, the third straight year above historical norms but a lower figure than the gangbusters 25% returns of 2023 and 2024. AI euphoria is still the strongest market trend entering 2026, and the usual suspects like NVIDIA Corp. (NASDAQ: NVDA) and Alphabet Inc. (NASDAQ: GOOGL) are up once again on the first day of trading. If you’ve ridden the AI rally since the market bottomed in 2022, you’re likely sitting on substantial gains and may feel compelled to diversify, especially if you have a tech-heavy allocation.

The S&P 500 is entering the year trading at 26x forward earnings, a stark elevation above its 20-year average of 16x forward earnings. When valuations are this elevated, investors become ravenous for earnings growth, and high-multiple stocks can fall out of favor quickly if growth slows even a little. And if rates remain high, 2026 could be the year value investing makes a comeback.

Today, we’ll look at ways to de-risk a portfolio by investing in stocks that enter the new year undervalued and overlooked. Each company discussed here trades at a substantial valuation discount to its industry average, but fundamental and technical tailwinds suggest this discount may not persist for much longer.

Comcast: Strong Balance Sheet and Sports Expansion Enhance Outlook

The Comcast Corp. (NASDAQ: CMCSA) was one of the biggest victims of the cord-cutting revolution, as customers fled expensive cable packages for a la carte streaming services.

A lost decade is always an investor’s worst nightmare, and CMCSA is about five months from completing this dreaded milestone, trading at about the same price it was in May 2016.

But now, customers are getting cord-cutting fatigue; streamers are raising prices and getting into costly disputes with major networks.

Meanwhile, Comcast has quietly built a sturdy balance sheet with a variety of revenue streams and its forward price-to-earnings (P/E) ratio of 6.84 is well below both the communications industry average (16.5) and that of major competitors like The Walt Disney Co. (NYSE: DIS) and AT&T Inc. (NYSE: T).

Comcast’s broadband business is a steady, high-margin cashflow machine. Despite Connectivity and Platforms revenue slowing 1.4% year-over-year (YOY) in Q3 2025, the EBITDA margins of the residential and business segments were 37% and 56% respectively. The advertising business also expects a boost in 2026 as NBCUniversal has the rights to Super Bowl LX, the FIFA World Cup, and the Winter Olympics in Italy.

The company generated $4.9 billion in free cash flow in Q3 as well, continuing to support its 4.4% dividend efficiently. Comcast’s value story might not be a secret much longer as the stock is up nearly 10% in the last 30 days, and some technical signals are hinting at further upside ahead.

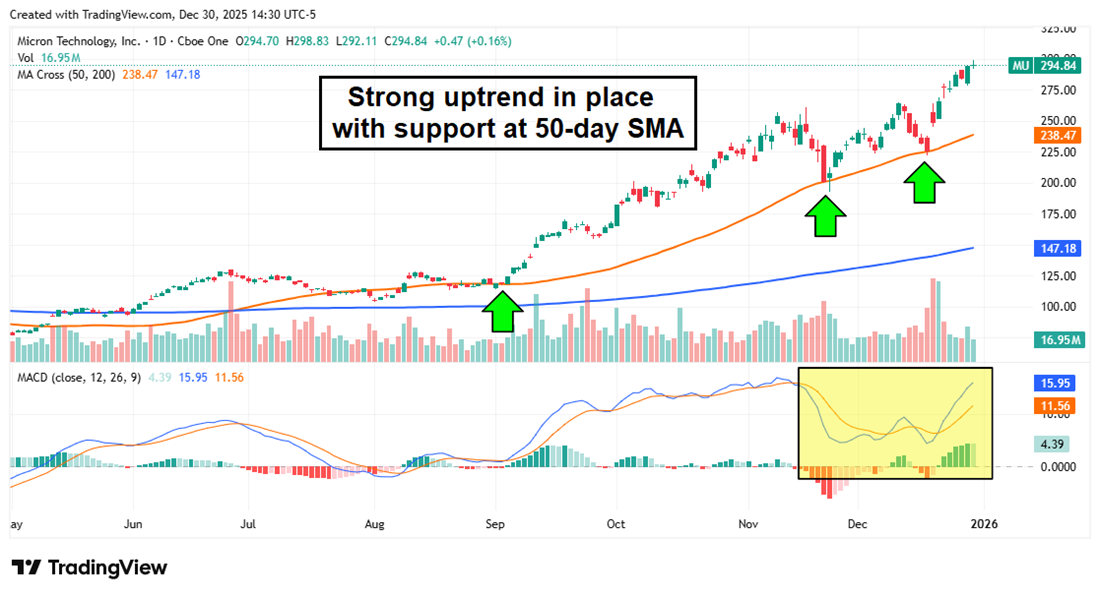

Micron: An Essential AI Stock Trading at a Deep Discount

How can a stock that just wrapped up a 200% year still be undervalued?

Despite its parabolic 2025, Micron Technology Inc. (NASDAQ: MU) remains one of the more undervalued players in the AI industry, trading at 29x earnings while the tech sector sits at close to 75x earnings.

A P/E ratio of 29 isn’t exactly cheap compared to the rest of the broader market.

Still, it's a great deal for a company generating 57% YOY quarterly revenue growth, 57% gross margins, and boosting guidance projections every conference call.

Memory stocks are high-margin businesses, and Micron management has stated it is struggling to keep up with insatiable demand from data centers. The chart shows a healthy stock in a strong uptrend, with support along the 50-day simple moving average (SMA). This matches the TradeSmith Health indicator, a new feature that measures a trend's viability. In this case, MU shares are in the Green Zone, which indicates a strong uptrend with healthy pullbacks.

Pfizer: Fueling Pipeline Innovation Through Acquisitions

Shares of healthcare giant Pfizer Inc. (NYSE: PFE) have struggled now that the COVID-19 pandemic is in the rearview mirror; the stock is down more than 30% over the last five years.

Competitors like Eli Lilly and Co. (NYSE: LLY) have soared past PFE thanks to obesity drugs like Mounjaro, but now Pfizer is trading near historical lows in valuation (8.4x forward earnings) and is far cheaper than most large-cap peers in the pharmaceutical sector.

The company’s Seagen acquisition is also beginning to pay dividends in the oncology division, adding more than $6 billion in revenue since the deal closed in 2023.

Despite a slow pivot into the growing obesity drug market, Pfizer now has a strong pipeline there as well, acquiring two smaller drugmakers with oral and injectable treatment options. The market has basically left Pfizer for dead in this space, hence the vast valuation gap. But low expectations often create opportunities; the stock hasn’t priced in Pfizer making successful inroads into the GLP-1 market. Additionally, Pfizer makes an excellent defensive investment thanks to its cheap valuation and history of dividend growth.

This email is a sponsored email for Capital Trends, a third-party advertiser of MarketBeat. Why was I sent this email content?.

This message is a paid advertisement for Intellistake Technologies Corp. (CSE: ISTK | OTCQB: ISTKF) from Capital Trends and Think Ink Marketing. MarketBeat Media, LLC receives a fixed fee for each subscriber that clicks on a link in this email, totaling up to $4,500. Other than the compensation received for this advertisement sent to subscribers, MarketBeat and its principals are not affiliated with either Capital Trends or Think Ink Marketing. MarketBeat and its principals do not own any of the stocks mentioned in this email or in the article that this email links to. Neither MarketBeat nor its principals are FINRA-registered broker-dealers or investment advisers. The content of this email should not be taken as advice, an endorsement, or a recommendation from MarketBeat to buy or sell any security. MarketBeat has not evaluated the accuracy of any claims made in this advertisement. MarketBeat recommends that investors do their own independent research and consult with a qualified investment professional before buying or selling any security. Investing is inherently risky. Past-performance is not indicative of future results. Please see the disclaimer regarding Intellistake Technologies Corp. (CSE: ISTK | OTCQB: ISTKF) on Think Ink Marketing' website for additional information about the relationship between Think Ink Marketing and Intellistake Technologies Corp. (CSE: ISTK | OTCQB: ISTKF).

If you have questions about your newsletter, feel free to contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 North Reid Place, Suite 620, Sioux Falls, SD 57103-7078. United States..

Post a Comment

Post a Comment