There are 3 stocks I believe you should be keeping a close eye on right now.

You may not know it yet…

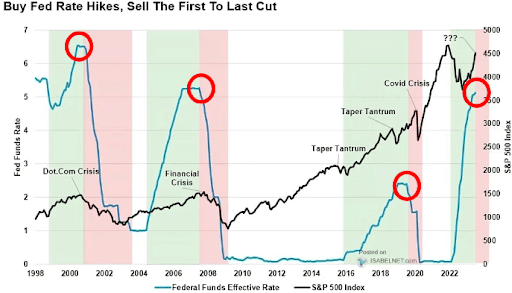

But we're at the brink of one of the market's most consistent resets – thanks to what Fed Chair Powell just set in motion.

And once this happens, you'd want to have your feet deep in one or all three of these names.

Granted, I can't make absolute guarantees here...

But allow me to show you my reasoning (backed by 4 decades of market experience) behind this stance...

And of course, hand you the 3 tickers in question.

If you'd like that, quickly head over here now for the full details.

By clicking the link above you agree to periodic updates from The TradingPub and its partners (privacy policy)

You Don't Need Big Money for These 3 Under-$30 Stock Plays

Written by Chris Markoch. Publication Date: 12/26/2025.

Article Highlights

- Stocks under $30 can help investors build meaningful positions with limited capital while maintaining diversification.

- Nintendo, NU Holdings, and Carnival each offer distinct growth catalysts heading into 2026.

- Analyst optimism, improving fundamentals, and company-specific tailwinds support upside potential.

There's something compelling about stocks you can buy for under $30 per share. For investors with $5,000 or less to put into the market, finding quality names at a low price creates an opportunity to build a meaningful position that can grow over time.

Of course, the key is finding low-priced stocks with genuine growth potential. That's the case with the three stocks profiled below. While inexpensive shares shouldn't make up an entire portfolio, they can play a useful supporting role in a diversified strategy.

Switch 2 Sales Momentum Makes Nintendo a Holiday Bargain

This stock gets a 94 out of 100 (Ad)

Buy This AI Stock Tomorrow Morning?

A former hedge fund manager known for spotting early winners is sounding the alarm once again. He called Netflix at $7.78 (up 4,200% since), Apple at $0.35 (up 20,000%), and Amazon at a split-adjust $2.41 (up 3,200%). Now he's turning his focus to a little-known AI company that just earned a near-perfect score in his new proprietary stock grading system. In a brand-new presentation, he reveals the name, ticker symbol, and why this could be the smartest AI move of the year... especially if you're over 50.

Nintendo Co. (OTCMKTS: NTDOY) has had a solid year in 2025. The stock is up about 14.5% year to date, which lags the broader market, and that performance includes a 21.7% drop over the 30 days ending Dec. 24. The recent slide reflects rising prices for random access memory (RAM) driven by demand for artificial intelligence (AI) applications, which has put pressure on margins for Nintendo's Switch 2 consoles.

Nintendo has raised its Switch 2 sales forecast from 15 million to 19 million units and said it will maintain current console pricing. It may be able to do that thanks to long-term supplier contracts that should help mitigate higher component costs, at least temporarily.

The investment thesis is straightforward: if Nintendo meets its sales targets, NTDOY looks attractively priced trading under $20 per share.

One caveat: NTDOY trades on the over-the-counter market, so some brokerage platforms may not offer the stock.

Explosive Customer Growth Fuels Bullish Case for NU Stock

NU Holdings (NYSE: NU) has jumped more than 61% in 2025, outperforming many financial stocks and the broader market. The Latin American fintech showed particularly strong growth in its most recent quarter, adding approximately 17 million new customers and increasing revenue about 42% year over year.

The bullish case for NU in 2026 centers on continued customer growth and the resulting improvements in unit economics. The company also plans to pursue a banking license, which could open additional revenue streams and enhance profitability.

Risks include slowing customer acquisition—especially in Brazil—and potential setbacks in obtaining a banking charter. U.S. investors also face currency risk if Latin American currencies weaken versus the U.S. dollar.

Analysts remain optimistic: Goldman Sachs recently reiterated its Buy rating with a $21 price target, roughly 16% higher than the consensus target and about 8% above the stock's Dec. 24 price.

Dividend Reinstatement Signals a New Chapter for Carnival

For many, the holiday season is cruising season. For Carnival Cruise Lines (NYSE: CCL), it's been relatively smooth sailing this year—CCL is up about 21% in 2025, roughly in line with the broader market.

The stock has shrugged off some headwinds that surfaced after its most recent earnings report. Analysts are generally bullish: the consensus price target of $34.41 implies roughly 10% upside, while several firms maintain significantly higher targets.

On Dec. 19, Carnival issued a business update that raised full-year guidance and forecast net yields of at least 2.5% for the upcoming fiscal year.

The company also reinstated its dividend, authorizing a quarterly payout of $0.15 per share payable Feb. 27, 2026, to shareholders of record on Feb. 13, 2026. Carnival suspended its dividend in 2020; returning to a payout suggests the company is on firmer financial footing and can support shareholder returns while funding future growth.

This email message is a paid sponsorship provided by The TradingPub, a third-party advertiser of MarketBeat. Why was I sent this email message?.

If you need help with your subscription, feel free to email our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place #620, Sioux Falls, South Dakota 57103-7078. U.S.A..

Post a Comment

Post a Comment