Postcards from the Edge of the World (Vol. 10)The One Thing They Take More than Anything Is The Only Thing That Matters.

To Whom It May Concern (YOU!): We’ve reached the critical volume of Postcards from the Edge of the World. This is Volume 10. This is the most important discussion about policies and outcomes in the modern financial and social system. That’s because what’s really extracted doesn’t top the list of daily American concerns. Largely, because we don’t really talk about how the system works. Moving forward, you’ll never unsee the impact or details. And, as always, I ask you to keep an open mind. A Homework Assignment and Measure of Your MoneyThis weekend, I ask you to do a few simple calculations. It’ll be very difficult to tally everything, and the outcomes may make you uncomfortable. Calculate your federal, state, payroll, property, and, finally… the sales (excise fees and usage) taxes from everything you bought. Start there. I know. It’s a lot. Every dollar, nickel, and dime you can find on statements, tax bills, receipts, and so on over the year 2025. Subtract that figure from your annual income. That will give you a net income figure. Divide that net income by gross income. That percentage represents how much of your working year you really keep. Don’t think about it as money. Think of it as hours. The percentage of hours of your working year you actually kept. The rest of those hours (percentage-wise) were transferred before you ever had control of them. There’s no debate about this. It’s just math. The financial system doesn’t care how you feel about this surprising calculation. You’ll find FAR more is collected than the advertised rates we calculate each spring tax season. We’ve been trained to think of taxes in terms of percentages of income earned once a year on only on two major sources. Those basic metrics are income tax brackets. You might pay 20% federal and 5% state, and the government will calculate an “effective rate” based on deductions. That’s an easy framing for tax collectors. Percentages can feel abstract and exist in spreadsheets or legislation that few people read. These percentages obscure the real costs, and we rarely “count” all the sales, excise, and other fees that nickel-and-dime our income. Those just feel like inconveniences. Unless we really reframe this. Taxes and fees are not percentages of wages or investments. They are, when tallied, hours of your time. They are an extraction of time and energy, not necessarily the trade-offs of consumerism, as Henry David Thoreau realized in Walden (the quote above). If your combined “tax and fees” burden across all methods is 40% (and it is easy to reach that level if you run your own business), then 20 out of every 50 hours are transferred. That’s basic arithmetic. It also means that two of the last five years of work were transferred to another location. We start measuring YEARS in life when we look at the long run. This will not be a rant about taxation. It’s simply an observation of mathematics and its impact on finite time. You traded finite hours for wages, and a portion got redirected before you could decide what to do with it. By definition, this is an extraction of your present time (less than 12 months). It’s visible and documented. But present-time extraction is only one layer of the financial system. Two more forms of time extraction operate with less visibility.

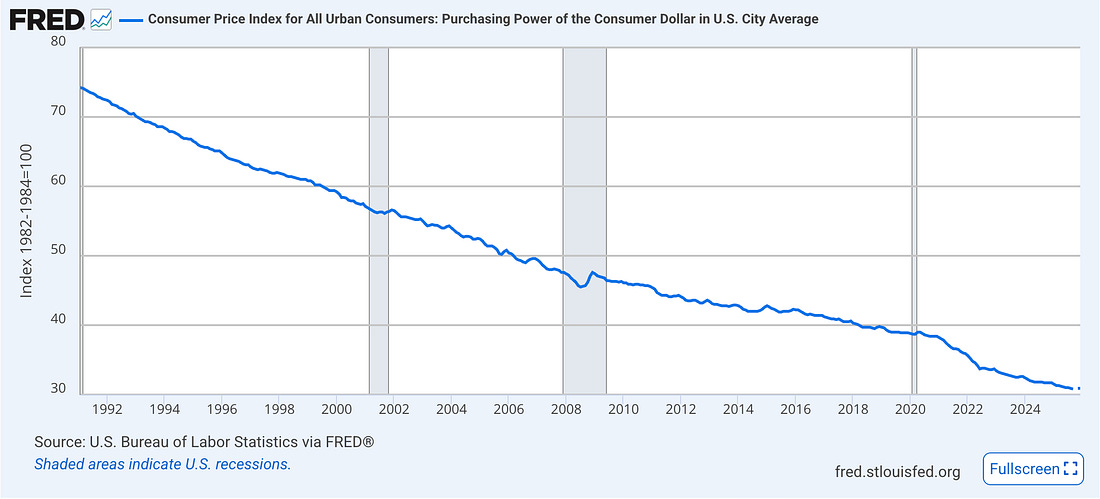

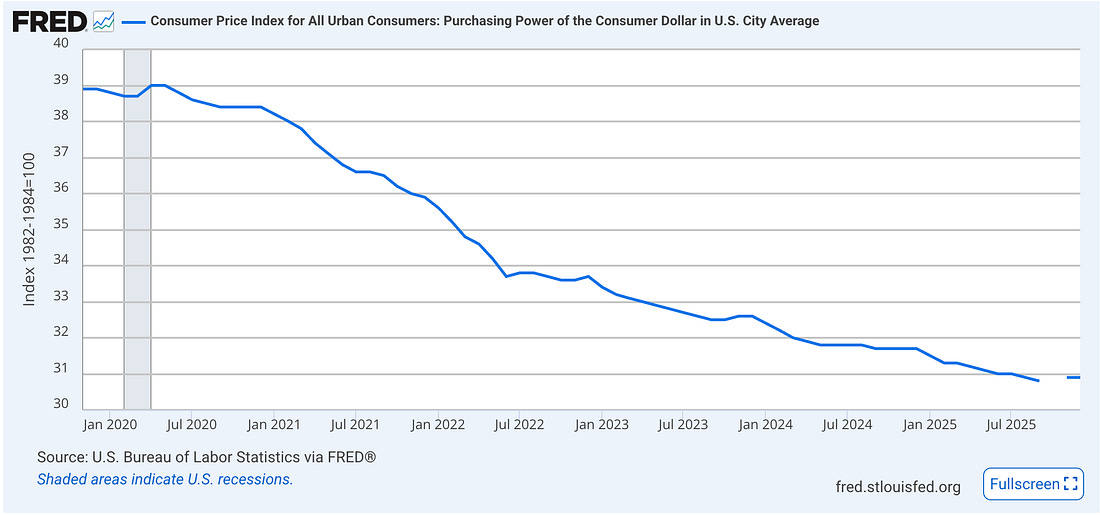

The Ways They TakeLet’s talk about your savings account. Many people have disciplined savings behaviors and might be nervous about deploying it to a stock market that has surged and crashed repeatedly since 2008. Sure, we’re back near all-time highs, but only 62% of Americans invest. Many might just live off fixed-income payments. They may be older and more risk-averse. Or they’ve thrown in the towel and don’t trust the equity market. They might have also delayed consumption, resisted the temptation to spend, and set money aside for the future. These savings are not just dollars. They are stored labor and crystallized time. The hours you might have worked in 2015 or 2018, or whenever you earned that money, are preserved in a simple figure… at a specific rate. Now, let’s discuss what happens when we see the purchasing power of that stored time erode over time due to fiscal and monetary policies. Economists have a specific term for this. It’s called the “inflation tax.” This is a nice way to say that we’re seeing the purchasing power fall for someone who thought they were doing the right thing by saving for another day. The U.S. dollar’s purchasing power has steadily declined for decades.

Now, this is a static analysis. Let’s talk about the guy with the rainy day fund who tosses cash into a basement safe. If you saved $10,000 in 2020, and inflation eroded that purchasing power by more than 20% (which is the official reading of CPI), then you’ve lost a sizeable stake of your stored labor (unless you spent it or found a way to generate a return over 20% during that period). Not everyone has done this. We are only focused on the “real value” of the underlying money. Remove the expectation or argument that a person needs to keep up with inflation (which isn’t guaranteed, given the 2022 stock market performance). People understand nominal value declines. If they invested $10,000 in the stock market at the start of 2022, and the market fell 20%, they would have $8,000 on paper. That’s a nominal decline. But a real decline - fueled by purchasing power - feels different to people. The real purchasing power loss of $2,000 due to inflation is not shown on paper.

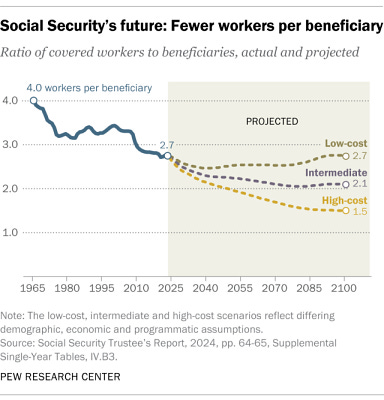

That initial value of $10,000 was from work previously performed and consumption previously postponed. It’s still $10,000… reads $10,000. But that real value decline compounds, just not on a dollar holder’s behalf. Inflation isn’t really about raising prices. It’s a redistribution of time from savers to borrowers. Inflation shifts stored time from fixed-income or dollar holders to those people whose income adjusts with prices (more on that below). Academics Doepke and Schneider have studied this redistribution of nominal wealth. They noted that the transfer isn’t random, but extends across balance sheets and the hierarchy of the credit system. I argue it’s not just an extraction of past time, but also the dignity of past work. What makes it more troublesome is that this process never requires a vote, and it doesn’t appear in headlines. It’s a silent assassin that compounds quietly. But one day you wake up to realize that what you previously earned no longer can purchase what it once did. People aren’t taught this on a wide scale. If they learn anything about finance in high school these days, it’s that it’s responsible to save money in a bank. But the last 16 years have proven otherwise. And the economist with the Ph.D…. who knows better, just shrugs. Beyond Past and PresentThere’s a third layer to the extraction of time. It stretches beyond the past and present. Governments must borrow… and have always borrowed money. It’s just historically been about whose been the least worst at that process. But let me ask: What are they really borrowing? To answer that question, we must discuss how much they borrow and who eventually pays the bill. Traditional theory in public finance uses a phrase that sounds mundane, but it’s extremely important: the “intertemporal budget constraint.” [Editor’s note: Intertemporal budget constraint! The editor has used another wonky term… Drink!] It’s a challenge for a decision-maker trying to balance the impact of present and future outcomes. The Congressional Budget Office (CBO) publishes long-term projections each year that show how current deficits impact future financial obligations. This budget constraint means simply: “Borrow today, and pay tomorrow.” Think of it as “Buy Now, Pay Later” - but in the trillions of dollars by governments. How is it paid off? Through taxes, inflation, fewer public services, or a combination of all three outcomes. The U.S. runs a massive deficit, and this isn’t free money. For now, they’re borrowing time. Deficits are claims on hours that haven’t been worked… by taxes that haven’t been collected and by obligations measured against future output. We’re just running an expensive tab at a bar… But the people who have to ultimately pay the bill haven’t walked through the doors yet. Future time is important in this discussion… and that’s why I asked you to compute your “payroll taxes” in your tax obligations calculation above. Social Security and Medicare costs are ample for self-employed workers, and they withdraw capital from employers that could have gone to employees in real time. Some economists will argue that payroll taxes are deferred compensation… not a form of taxation or “extraction.” The argument goes that you’ll receive those benefits later. And, yes, that’s true. The obvious problem is that the Social Security Trustees’ reports project the depletion of the trust fund within the next decade. That would happen without reform. This suggests we’ll see either benefit reductions, higher payroll taxes, or additional government borrowing. Right now, there are just 2.7 to 2.9 workers for every person receiving Social Security payments today. That’s a big drop from 4 workers in 1965. And that ratio could fall to 2.1 to 2.3 workers in the coming decades. This isn’t sustainable, and the expectation is that we’ll collect more from existing payees to finance existing claims.

The chart above shows a measure of “demographic math.” When demographics force changes or deferment, the system doesn’t remove the cost of time. It just shifts those costs across generational cohorts, tax thresholds, and future expectations that people think they’re going to receive. But none of these deferrments are “guaranteed” under current frameworks. The government can raise retirement ages. The overseers can reduce benefits. Or contributions can increase on existing workers, which eats into the present value of their labor and income. And all that does is borrow more time. Many younger people now assume that the full present value of their Social Security contributions will not be realized in future benefits. This is why the Social Security Administration creates these “Fact Sheets” - because the government would never, ever showcase any dishonesty about anything. Anyone, including politicians and bureaucrats, trying to argue that the current system is sustainable has an arithmetic problem and a time problem. Extractions from future time are the most invisible layer of this system. But the modern system doesn’t choose between taxing the present, inflating the past, or borrowing from the future. It does all three at once. Why? Because layered efforts in fiscal and monetary management stabilize the system better than any single lever could. It’s also very hard to keep up with all the different layers and feel them at the same time. Voters don’t really notice. Economists just shrug. And it’s uncomfortable to think about because it means that portions of our future are already mortgaged. The math, however, is clear in CBO reports.

Let’s Go Beneath the NoiseLet me show you another way that this works within the mechanisms. Right now, the Treasury is issuing large amounts of U.S. debt at the short end of the yield curve. They’re choosing to keep ample capital in the financial system, and economic conditions expanded. The more people who lock up money in longer-term premia (10-year bonds or more), the less liquidity sloshes through the system. The Treasury, effectively, runs the economy hot with short-term Treasury bills that must be refinanced within 12 months or less. And if you read the quarterly refunding statements, you’ll see a pattern. Short-term debt has been the strategy of Treasury Secretaries for a decade. During Steven Mnuchin, Janet Yellen, and now Scott Bessent’s tenure. This strategy technically carries lower interest costs in the near term… as buy purchasers should demand greater returns for locking up capital for longer. And that’s rational given the incentives facing policymakers to manage $38 trillion in debt. But issuing short-term debt lowers costs today, while increasing rollover risk in the future, especially if inflation runs hot and yields rise. Funding is easier today, but tomorrow is more rate-sensitive. When rates rise, governments issuing large amounts of short-term debt must refinance more quickly. If rates rise, the theoretical savings of the strategy evaporate, and the burden shifts forward - for everyone paying into the system. Yes, lower payments today look responsible and manageable. And in a world based on four-year presidential cycles, higher refinancing costs tomorrow become someone else’s problem. This is not a policy failure in the traditional sense. It’s a policy success if you understand the incentives of the people in government. Politicians operate on election cycles measured in years. But remember, these are human beings. Behavioral economists like David Laibson have shown that humans place far too much emphasis on present values relative to future values… or they want smaller rewards now over better long-term outcomes. This is a behavior known as hyperbolic discounting. This is the key quote from a 2003 interview at the Fed Reserve Board.

People constantly want relief now and assume they can manage the costs later. Public policy follows the same logic. Policymakers are humans responding to human voters. Central bankers are responding to the financial system. They’ll regularly front-load the benefits and back-load the costs. The pundit says that we’ve “kicked the can down the road.” The economist prefers the line: “We’ve deferred the adjustment.” The latter doesn’t sound like the former, but it just means that the bill will come due another day. By default, these actions mortgage time that people haven’t lived yet.

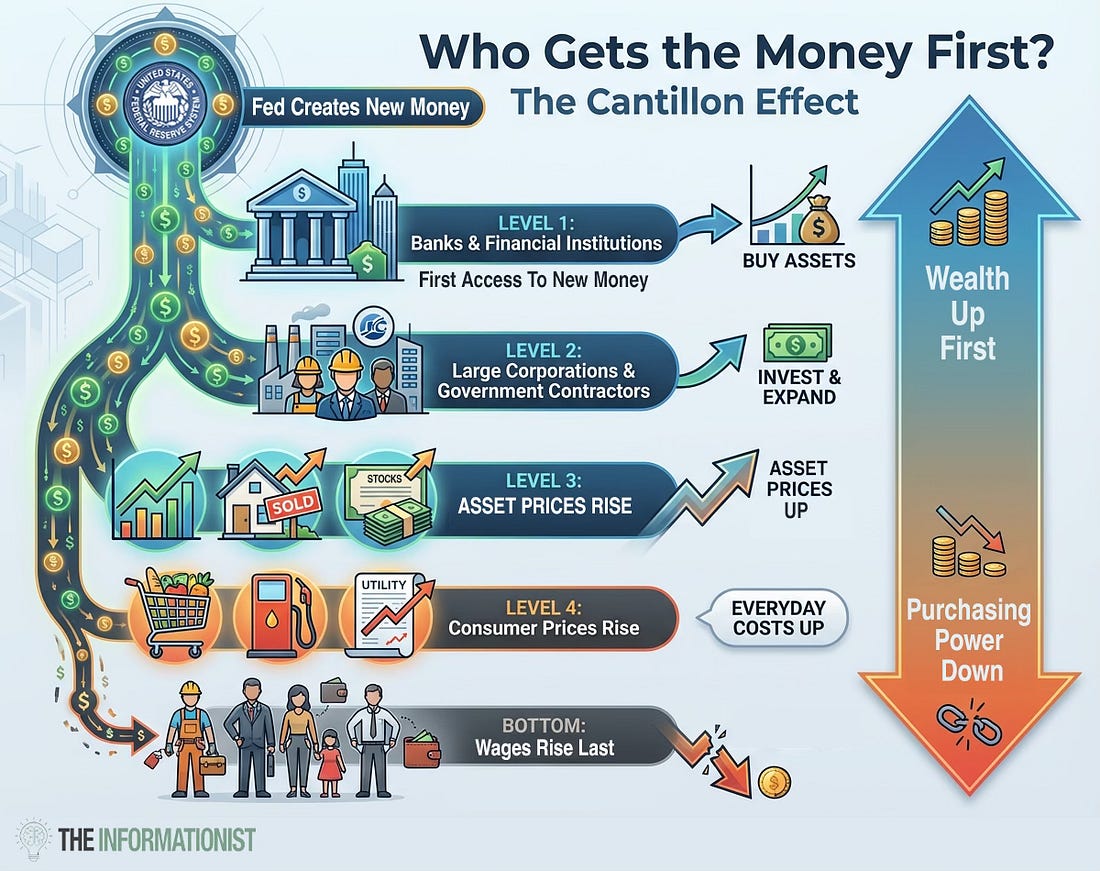

How Power Really WorksThere is one more mechanism worth exploring. It tells us why extraction destabilizes a financial system. When new money enters the system, it doesn’t hit everyone equally at once. We’ve explored this phenomenon quite a bit at Me and the Money Printer. But let’s offer a quick refresher on what happens. Recall economist Richard Cantillon. He noticed how people behaved when capital was created in 18th-century Europe. He saw who benefited the most from the process. What’s dubbed the Cantillon Effect shows us how newly created money benefits early recipients before prices adjust across the economy. No, we don’t operate on debased gold coins like in the 1700s, but we have a different financial system that benefits people at the point of capital creation.

In modern economies, liquidity or “credit” usually enters through large financial institutions and credit markets. The chart above, from James Lavish, offers a clear breakdown of how money enters an economy and erodes purchasing power by the time it reaches wages, which are at the bottom of the chain of capital. After money moves to banks, contractors, and people closest to the money’s creation, we see asset prices rise. We see housing prices and equity prices rise… money moves into risk assets. But wages lag well behind capital creation. And that reduces buying power. The average person at the bottom is more likely to encounter new money through mortgage payments, student loan balances, auto loans, or credit card balances. Effectively, it arrives in the form of higher entry costs, financed with debt. Debt service is an extraction and precommitment of future time… driven by the monetary and fiscal policies. People might blame the banks or lenders, but the origins lie in the halls of fiscal and monetary policy. And, our debt-based system is really just an ongoing collection of legal claims on future labor hours that were underwritten against earnings not yet generated. And since asset prices adjust before wages, the cost of entry into housing, education, and economic participation rises faster than your ability to pay. The Everyday HustleYou’re not the only one experiencing this effect. Businesses do as well, which is why the little fees and increased taxes find their way into our lives. You feel the scalping of time and income in small ways. It’s not just the excise taxes that come up in state budgets each year. It’s the subscription that renews automatically at a higher rate or the insurance premiums that surge despite no claims on your house or vehicle. It’s the product shrinkflation or the convenience fee that’s just introduced. And the worst: a cancellation policy that aims to prevent subscription or service cancellations. None of these things alone breaks a person. But that’s the point. They now just hover beneath our tolerance for financial pain or sources of outrage. But they build gradually. The gym membership that you struggle to cancel feels like the problem. But what about the fact that it’s now designed to make cancellation very difficult? That in itself is another form of extraction. One that takes you present time to complete… and one that might even cost your more money (and - resultantly - past time). Yeah, we just reach into one another’s pockets constantly. It all starts back at the front of the capital chain... in policy. Let Me Speak ClearlyI want to stress something. And I said this earlier. This is not a complaint about taxation. It’s a measurement of mathematics and calendars. All governments extract time and demand taxation. We must build roads and make sure that courts operate. This is the point where people start saying: “Well what about fire stations?” That’s not the thought experiment. We must pay for defense and coordinate on infrastructure that isn’t provided by private markets. So, I’m not arguing for anarchism.l And I’m not opposed to the concept of taxation. But I will discuss a broader point about the scale and opacity of policy. The truth is simple. Social Security transfers today’s worker income to retirees in exchange for a promise of future payments, a system that struggles to replace the people paying in. In modern finance, U.S. deficits can smooth financial shocks, and monetary policy historically stabilized markets and economic downturns. However, our behavior in recent years has led to drastic expansions of deficits and economic conditions in non-war-time. The question isn’t about whether time has shifted. It’s really about how much, how transparently, across which generations, and over how many decades. When taxes increase, inflation runs hot, and debt compounds, the burden across generations increases, and affordability becomes a central problem. The results are evident in the CBO’s long-term debt projections and the dollar’s century-long decline in purchasing power. It’s evident in the massive amount of leverage one must take to rise above middle-class status. It’s clear in the way that the Treasury is using short-term debt and how sensitive that strategy is to interest rates. We pull forward future demand to the present. We strengthen balance sheets that, on paper, protect against inflation, but raise the cost of entry into real assets for anyone just getting started in America. And since no one explains what has been done… we end up with politicians who make insane promises doomed to fail a younger generation. That can lead to more debt, more taxes, worse services, and more time extraction. But we must all look in the mirror. Political pendulums swing in a world where we’ve been treating multiple expansions as a form of innovation via financialization, and we pretend that financial leverage is a form of progress. When money is created, taxed, inflated, or borrowed against future production, the underlying transfer of time shifts from one party to another. Money can be printed. Time cannot be. That imbalance is a foundation of everything I discuss here (and one of my great agitations with policy-making). The people who kicked off this process are long gone, and memories are short. Whoever is in charge during the crisis is to blame. It always seems that way. In good times, the system always looks like it’s running smoothly. Inflation looks modest, and deficits look manageable. And, as always, there’s always an economist at the New York Times who will tell us not to believe our own eyes and that all of this is sustainable. Gradual extraction is designed to look normal. But one day, all of a sudden, the present feels tighter than it used to. You find yourself feeling that your past was lighter and easier than you recall. And it’s all because the future was mortgaged before you to this moment. The Sovereign Moves at HomeWe know the system extracts time (and money) across three time dimensions. How do you store your time in forms that resist future extraction? The answer to this question is positioning.

I stress the importance of following a sovereign model during this period. Our ideas here at Postcards are not about gambling on momentum. They center on inflation protection, capital and goods movement, and permanent capital. These investors own toll roads, pipelines, royalty streams, intellectual property, and infrastructure that generate returns regardless of policy cycles or who is in charge. It’s an incredibly simple model, one that has been tested through crises in previous periods and empires. You want to own the toll booth because spending your life in line at one will cost you money, time, and perhaps the dignity of your work. And since we are always focused on more than portfolio positioning, consider these simple steps to reduce extraction at the household level.

These are not wealth-building strategies. Instead, they help you play defense and stop the slow leak of hours and time from your life’s worth. The sovereign move allows you to anticipate and understand how this system shifts your time in this world, not just your money. You position yourself accordingly and start measuring life in hours that belong to you. Now then, allow me to present an investment idea that helps you own tollroads and assets that generate income and build on the constraints we’ve discussed. If you enjoyed this, please consider becoming a member and receive this pick and many more in our weekly commentaries. Once you’ve joined… please click this link for our paid content…Suggested Reading

About Postcards from the Edge of the WorldThe Postcards Doctrine holds that wealth, power, and stability do not persist through innovation, morality, institutions, or financial sophistication, but through control of chokepoints that remain productive across regime change. Civilizations rise and fall. Ideologies rotate. Technologies obsolete themselves. Financial instruments are rewritten, repudiated, inflated away, or nationalized. What survives is not what performs best in good times, but what continues to function when systems fail, rules change, and authority resets. The doctrine begins with a simple observation: extraction always migrates toward what people cannot avoid. Early on, extraction flows through trade. Then finance. Then regulation. Then platforms. Then metered access. Eventually, it settles on inputs that cannot be substituted, deferred, or digitized. Postcards are sent from the edge of these transitions. Each one documents a moment when the system tightens, when optionality narrows, and when value stops flowing to innovation and starts flowing to ownership. Enjoy.

|

Post a Comment

Post a Comment