Hello, Thanks for signing up for MarketBeat Daily Ratings—we’re excited to have you on board. Every weekday, you’ll get a curated summary of new “Buy” and “Sell” ratings from Wall Street’s top-rated analysts, the latest stock news, and bonus investing content—all delivered straight to your inbox. You’re just two quick steps away from completing your sign-up: 1. Make sure our emails go to your inbox Gmail users:

Mobile: Tap the three dots (…) in the top right and select Move to Inbox or Move to Primary

Desktop: Click the folder icon at the top and select Move to Inbox or Primary Apple Mail users:

Tap our email address at the top (next to From: on mobile), then select Add to VIP Other providers:

Reply to this message and add newsletters@analystratings.net to your contacts 2. Confirm your subscription Click this link to confirm your subscription. This verifies your account and ensures you receive your newsletters without interruption instead of getting stuck in your spam filter. Confirm your subscription here. After you confirm, feel free to download our popular free report, "7 Stocks to Buy and Hold Forever" with this link. Thanks again for subscribing—we look forward to being part of your investing journey.

Matthew Paulson

Founder and CEO, MarketBeat. P.S. If you didn’t mean to subscribe, no problem—you can unsubscribe here.

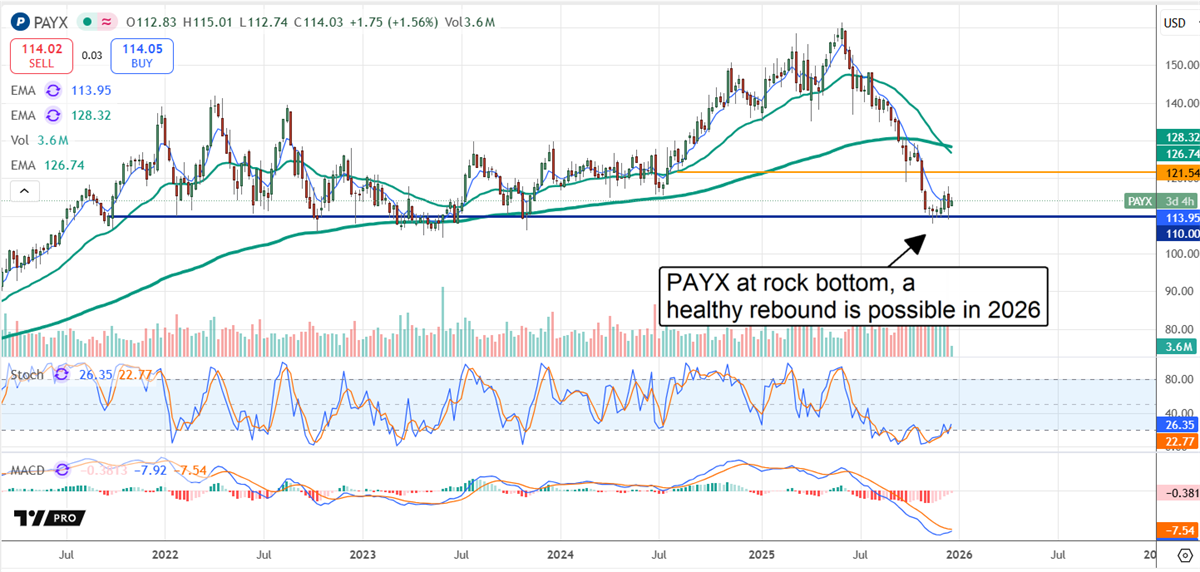

Exclusive Content from MarketBeat Paychex Is Out of Favor—And That's the OpportunityWritten by Thomas Hughes. Originally Published: 12/25/2025.

Key Points - Paychex is testing long-term support after mixed institutional flows, but underlying payroll demand remains intact.

- Insider activity has skewed toward selling rather than buying, even as the dividend yield has moved higher.

- AI-driven product rollouts and improving sentiment could be the catalysts that shift the stock off its floor.

Institutional activity has been mixed for Paychex, Inc. (NASDAQ: PAYX) over the last 12 months, with $6.38 billion of institutional inflows versus $5.17 billion of outflows. That selling pressure pushed the stock to a 52-week low in calendar Q4 2025. The move, driven by growth concerns, found support near those lows later in the quarter, creating a potential opportunity for value-oriented income investors. While downside risk remains, limiting factors—still-positive growth, strong cash flow, capital returns and shifting sentiment—are in place, and several catalysts lie ahead. Growth concerns aside, the company posted 17% revenue growth in the quarter ended Aug. 31, 2025, and raised its full-year fiscal 2026 earnings outlook, supported by generally healthy labor-market activity that points to continued outperformance and sustained capital returns in coming quarters. Insider activity is worth noting alongside the mixed institutional flows. InsiderTrades.com's last-12-month summary shows no insider purchases, three insider sales totaling roughly $16.46 million, and insider ownership near 0.80%. That doesn't automatically imply negative sentiment—insiders sell for many routine reasons, including pre-set plans or tax liabilities tied to stock awards—but in a sell-off investors often look for open-market insider buying as a show of confidence, and that has not been evident recently. The key takeaway from 2025 labor data is that growth slowed but continued: employment and wages are still rising and consumers remain healthy. The most recent releases, including weekly jobless claims, suggest some stabilization toward year-end. Those trends may be supported by policy and rate tailwinds, such as federal deductions tied to qualified tips and overtime for the 2025 tax year (claimed when filing in 2026) and the potential for lower interest rates—factors that could help keep consumer spending and labor markets steady. For Paychex, that translates into persistent demand for payroll and HR services. Analyst Price Targets Suggest Support Near $110 Analyst sentiment has been a headwind for PAYX in 2025, with downgrades and price-target cuts reinforcing the downtrend. Even so, there are constructive takeaways. One is that analysts appear to limit downside late in 2025: the low-end target near $110 aligns with a critical support level. That $110 area sits at the bottom of a long-term trading range, where deeper value can emerge. Another positive is the spread of targets following the Q2 fiscal 2026 (FY2026) release. While the low end is $110, most targets cluster around the consensus, implying low-double-digit upside for this high-yielding stock. Paychex is not cheap on a standalone basis—trading at roughly 21x current-year earnings—but that multiple looks reasonable compared with the average S&P 500 company, which generally lacks double-digit growth and does not offer a 3.8% yield. Relative to its own history, PAYX appears attractively valued: the stock's historical average P/E is about 28x (it has ranged from the high-30s down to the high-teens). The current 21x multiple is below the long-term average, implying meaningful upside versus historical norms. The greater opportunity for PAYX investors is longer term. Current headwinds and 2025 growth concerns appear to be discounting future earnings, placing the stock at roughly 11x projected 2035 earnings in one scenario. Under that outlook, the share price could potentially double over the coming years if growth materializes and sentiment shifts. In the meantime, the 3.8% dividend yield provides income and has historically increased annually. Share repurchases also continue to reduce the share count incrementally, supporting per-share metrics. Paychex Has an AI Catalyst in 2025 Paychex also has an AI-driven catalyst in 2025. The company is rolling out new AI-enabled tools regularly, reinforcing its position with small and medium-sized businesses that increasingly rely on cloud-based services. For clients, Paychex's tools offer automated HR tasks, data-driven insights, greater efficiency and improved operational quality. For the company, these products can boost demand for existing services and create higher-margin revenue streams through premium offerings—such as AI-enabled compliance tools that give clients an edge and typically command better margins. Technically, price action suggests a possible floor near $110, though downside risk remains if fundamentals or guidance weaken. Technical indicators—such as the stochastic oscillator—can be consistent with an oversold setup near support, and the MACD may be starting to improve as selling pressure eases. Likely catalysts for a rebound include early-January labor-market data, evolving rate expectations and upcoming company updates that clarify growth and margin trajectories.

|

Post a Comment

Post a Comment