“The State is the great fiction through which everybody endeavors to live at the expense of everybody else.” — Frédéric Bastiat To Whom It May Concern (You): I used to spend most weekends watching sports. I’d stare at fantasy football scoreboards for hours at a time. My father eventually told me,

Twenty years later, I read Bank for International Settlements reports on Sundays, build momentum systems to avoid liquidity crunches, and read SEC Form 4 filings before sunrise. The financial system is the biggest game in the world... more players, more stats, and more consequences. Those results just don’t end up on SportsCenter. And that’s a shame, because the best stories in the world are found in the math and trends most people ignore. All the while, my career north star is simple. Tell the truth about money and our deeply misunderstood financial system, regardless of who it pisses off. What follows covers those bases. The 900-Pound GorillaLast week, we explored a number. The Debasement Index... money supply divided by real GDP over time. This isn’t an inflation statistic. It is a dilution statistic of the currency itself. It’s been 6.7% per year for the British pound since the end of Bretton Woods. Estimates for the U.S. dollar cluster around 7% to 8%, depending on methodology, liquidity regime, and the measure of real output. This aligns directionally with work discussed by macro analysts at Real Vision and CrossBorder Capital, among others. Vincent Bühler’s model measures how the money supply expands beyond what the real economy actually produces. A few of you asked the obvious question after last week. Will it get better? To answer that, I spent the last week looking at the one variable that few people in finance and politics want to touch. It’s a number that underlies every fiscal projection, pension model, sovereign debt calculation, and Social Security estimate. And after looking at those numbers, my answer to your questions is… No. It doesn’t get better. It gets mathematically and structurally worse. The math tells me that there’s a variable in this equation that makes extraction and debasement more inevitable. That is the number of people being born. And this number is falling off a cliff in front of me. Welcome back to the Edge of the World.

The Ways They TakeThe one number that matters most in economics and public policy is 2.1. That’s the population replacement rate, or what each woman needs to have, on average, for a population to hold steady. When that number falls below 2.1, the population doesn’t collapse overnight. It creates inevitability, which every politician tries to outrun during their tenure. So where does the world stand today?

World Bank data shows that East Asia’s numbers are cratering. South Korea has a rate of just 0.7, meaning fewer than one child per woman on average. The U.S. sits at 1.6… Japan is 1.2. About 67% of the global population lives in a country where fertility rates have fallen below the replacement level. Today, 37 of the 38 OECD nations are under the 2.1 threshold. The only place above the replacement rate? Africa. And Pew Research says their replacement rate has plunged from 6.5 to 4.0 since 1950. The developed world, however, will see a decline start within the next decade. That matters. These nations run the global financial system, establish reserve currencies, and… importantly… make pension and government-retirement promises. Nippon.com says Japan’s population declined by 910,000 people in 2024… and about 400 schools close there each year because there aren’t enough students. China’s population peaked in 2022, the first decline in more than six decades, after building entire cities for a generation that never arrived. These are current numbers, based on present conditions. The issue is that today’s pension models, sovereign bond calculations, and Social Security calculations rely on outdated math. That same math assumed more children would arrive to fund those systems. They never arrived. What’s Beneath the NoiseDemographics were always going to collide with extraction models and currency debasement. In this case, it’s two vehicles speeding toward each other and gaining speed. The longer policymakers keep kicking the can down the road and stretch the timeline, the more violent that inevitable crash will be. The Debasement Index equation is “Money Supply divided by Real GDP.” In the fiat era, that ratio has been increasing between 6% and 8% a year, depending on how analysts interpret the data. We’ve treated the numerator and the denominator as somewhat independent forces. The reality is that they’re not. Demographics drive both sides of this equation in opposite directions at the same time. Start with our denominator. That’s Real GDP. A nation’s economic output is primarily the result of two things. How many workers do you have, and how productive are they? When that labor force starts to drop, productivity must increase to maximize the output. The latter must do the lion’s share of the work… It usually doesn’t… In a 2023 paper published in The American Economic Journal, Nicole Maestas, Kathleen Mullen, and David Powell found that a 10% increase in the population aged 60 and older is linked with a 5.5% decline in GDP per capita. About a third of that drop is due to slower employment growth. But two-thirds stem from a productivity slump. What’s our primary case study for this? Japan. The nation’s labor productivity has grown at about 1% on average over the last 25 years. But GDP per capita sits at just 0.5%. Productivity gains are being eaten up by fewer workers, more retirees, and lower average hours. I know exactly what someone is yelling right now. “What about AI? Isn’t that going to fix all of this?” Here’s the problem with that argument. Social Security, Medicare, and most pension systems are financed through labor income. Think wages, hours worked, and contributions tied to people, not machines. Robots don’t pay FICA. Payroll and labor taxes do. Productivity doesn’t fund entitlement systems. This is where most AI optimism makes a fundamental category error. It confuses higher output with a system’s ability to fund fixed, legal promises. And if AI replaces human labor at the scale its advocates promise, the funding gap actually widens. You get fewer workers, lower payroll contributions, more retirees, and larger obligations. That doesn’t reduce debasement. It should accelerate it. There’s also a timing problem. Social Security hits depletion around 2033. AI would need to generate unprecedented gains in less than a decade, and those gains would need to flow into taxable wages fast enough to fund a system designed for a much larger workforce. Arithmetic always wins in the end. Now, there is a real distinction worth acknowledging. Japan’s automation wave focused on manufacturing and industrial processes. Generative AI targets white-collar work and services, where productivity gains have historically been hardest to achieve. Even if AI finally cracks service productivity, it still runs headlong into the same wall. The math doesn’t change. For AI to “solve” the demographic problem, it would need to deliver unprecedented productivity gains AND generate enough taxable human labor income to replace a shrinking workforce. And… this is the critical part… GOVERNMENTS WOULD STILL NEED TO STOP PRINTING MONEY. That combination has never occurred. Every dollar of unfunded obligations is a promise some politician made to someone who votes. The printing isn’t driven by a lack of productivity. It’s driven by a lack of political will and the gravity of debt-based systems. Technology is deflationary… and “money printing” or monetary expansion papers over the deflation that impacts real asset prices in a debt-based system. This means monetary expansion through “inflation targeting” toward a 2% target. If deflation threatens the economy… they print more to bring inflation up. That’s been the standard since the mid-1990s, although it wasn’t officially announced as Federal Reserve policy until January 2012 by then-Fed Chair Ben Bernanke. We papered over the impact of labor deflation from the fall of the Berlin Wall and the rise of China’s cheaper workforce. We papered over the deflation of the e-commerce boom. We engaged in multiple rounds of Quantitative Easing after the 2008 Great Financial Crisis due to deflationary pressures. If AI is robust, the labor shift would be unprecedented. We outsourced blue-collar labor to Asia. This time, we’re outsourcing white-collar labor to AI models and data centers, all while passing higher electricity costs onto Americans, which is like paying your salary to the person who’s replacing you at work. AI would be highly deflationary. In a debt-based system, monetary expansion becomes the fallback to prevent refinancing crises and ensure voters feel whole in dollar terms. Combine this deflationary impact with an aging population, and all roads point to monetary expansion (which means they’ll fire up the printer and extract more time from younger generations, past, present, and future). Yes, they might reform the system. They could raise the cap on taxable income. But as you’ll soon see, that too just accelerates the extraction from the younger workers who are already the denominator in this equation. You can’t pay today’s retirees on the back of tomorrow’s maybe. Even though politicians try all the time. The Great BRRRRRNow… It’s time to look at the other side of the equation. That’s the money supply. Governments across the West face surging healthcare costs, rising Social Security claims, higher pension obligations, and other mandatory commitments. What do those things have in common? An aging constituency. To address those future obligations, there are three choices. Politicians can cut spending… and then immediately lose office because the most important – and growing – voting bloc is retirees. They can raise taxes, which will choke existing workers. Or they can borrow and print. What’s easiest? Printing. So, that demographic downturn nudges both sides of the Debasement Index in the wrong direction. Our denominator stalls out because we don’t have enough bodies. The numerator starts to surge because our obligations pile up. This is what I’m defining as Dependency Driven Debasement. It’s not a discretionary policy choice. It’s quiet, structural, and politically invisible. It’s also the very thing that sits in the pit of anyone’s stomach if they’re under 50 in America. Younger Americans already knew something was off before this AI revolution. They just couldn’t figure out what is wrong with the money. They’re told inflation is just 3%, but they know nothing about the way that we keep changing the government definition of it… and we don’t talk about the real costs in cities for the things that people actually buy… They might not know the history of Lyndon Johnson and his push against the Federal Reserve to fund the Great Society and the Vietnam War… and how the Fed relented, took America off the gold standard under Richard Nixon, and then enabled the unraveling over the last six decades. WTFHappenedin1971.com documents the shift in how America changed. Over time, with the monetary base expanding 6% to 8% annually… the problem isn’t going away... Structural debasement is more likely to worsen. Not because of public policy or who is president. It’s just because of math. Nations made promises to people who were alive and sent the bill to people who weren’t. How Power Really WorksThis is where the system stops being theoretical and starts being contractual. Here’s some more math… In the U.S., our fiscal gap represents the present value of all future government obligations minus expected future revenues. In 2023, that figure, according to the Cato Institute, was about $80 trillion, depending on how the Treasury Department defines the discount rate. That was almost three years of the nation’s GDP. Cato said about 95% of that figure is Medicare and Social Security. Now… our Social Security fund goes belly up around 2033, which is where we risk a serious entitlement crisis and perhaps the start of a new monetary system (if not sooner). Without reform, at that point, the continued tax will only cover about 75 to 77 cents of every future obligation owed to citizens. I pulled these figures from the 2025 OASDI Trustees Report. That’s published by the Social Security Administration. People get mad at me for repeating numbers published by their own government. The operators are telling us, in writing, that the math doesn’t work. And the workforce math supporting Social Security gets worse each year. In 1980, the U.S. had about 3.2 workers for each retiree. That figure just hit 2.6 this year. Come 2040, it’s on track to fall to 2.28. And then it keeps falling over time. The OECD writes that, by 2060, the working-age population across its member nations will decline by an average of 8%.

As this chart shows, some members will lose over 30% of their workforce. Dependency Driven Debasement is no longer avoidable. The tax base is falling while obligations are rising. The only solution… is to absorb this massive gap with the fiat currency. Japan’s debt-to-GDP ratio is 226%, according to the IMF. The Bank of Japan’s balance sheet is within striking distance of the nation’s GDP.

The yen is falling continuously… The pressure of an aging population will be addressed through currency depreciation. In August 2024, CME Group published a negative 0.65 correlation between a nation’s currency performance and its old-age dependency ratio and its currency’s performance. What does that mean? The older your population becomes, the weaker your currency gets. The Everyday HustleIf you’re under 50 like me, you’re the denominator. Most of these promises started before you were born. Pension systems originated when we had six or seven workers for every retiree. And back then, life expectancy (something else we haven’t touched on yet) was about a decade shorter. The math worked out back then. Today, it doesn’t work. It’s not just the pensions though. Let me introduce you to an ordinary person who’s paying for this system. She’s 26 years old…

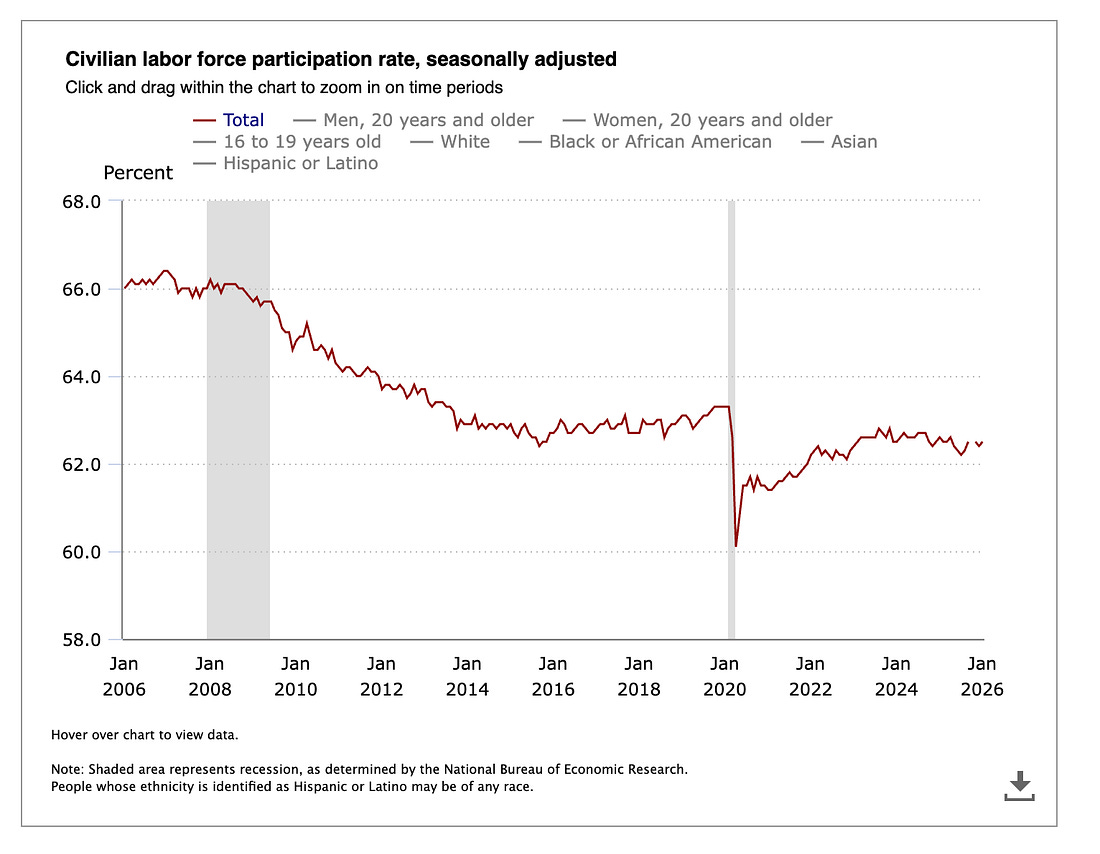

She’s an independent gig employee who earns about $70,000 a year net across various clients as a 1099 (meaning she pays Social Security taxes on both sides). She “runs her own business” and has it classified as an LLC. She pays for her own insurance with a high-deductible plan through a government exchange (part of her expenses, but with high out-of-pocket costs). She pays over 15.3% of that net revenue converted to salary ($10,710) to Social Security and Medicare, money that goes directly to fund current retirees. If she saved everything pre-tax, she’d hypothetically lose about $3,500 to $4,750 a year in purchasing power on what she manages to save, as the currency is diluted by up to 6% to 8%. She rents because the median home is about 5x the median household income, according to Harvard. In 1980, 15 years before she was born, it was 3x. Back in 1978, a minimum wage employee could pay for a year of public university tuition with 385 hours of work. Some estimates put that figure today at north of 2,000. So, she’s got student loan debt. She’ll also never receive a pension. And Social Security will be mathematically incapable of paying full benefits before she turns 40. But here’s the unavoidable part of all of it. It was all a wind-up to this point. Every non-self-aware financial advisor, “back-in-the-day talking” retiree, and self-serving politician tells her that if she just saves a little more and stays disciplined, she’ll be fine. She won’t be fine because the math doesn’t allow it. And that’s not even the half of it yet… Let’s say she lives in Chicago, where she’s also paying massive amounts of state, local, and sales taxes. Chicago’s pension system is $36 billion underfunded. When pension systems buckle… and pensioners are consistent voting blocs for politicians… someone is ultimately going to write a check. And if they can’t squeeze it out of local taxes and fees, or rising property taxes (passed on to renters like her), then eventually the nuclear option will be on the table. That check will one day likely come from federal taxpayers or from freshly minted “liquidity.” The people who were promised will demand to be made whole. They’ll argue they were legally entitled to these pensions... The cost will be borne by the people least able to afford it... through higher taxes, through a debased currency, at a time they can’t buy homes, can’t find jobs that haven’t been reclassified as 1099 contracts, and can’t escape a system that prints money and distributes it FIRST to people who already benefit the most... Either way, it all lands on her generation. She is fully funding a system that cannot fully fund her. Now let’s add this all inside a nation where politics are personal… After all this weighs down on this person just a few years out of college… Someone (maybe her parents, maybe an older financial pundit, or a political advocate canvassing door-to-door) will ask her why on earth she would vote for a candidate the questioner finds unacceptable. On one side, it’ll be a populist who wants to tear down institutions or whose policies failed in the 18th century. On the other side, it might be the socialist whose ideas failed in the 20th century. But both extremes will continue gaining ground for the same reason. The social contract was broken. This isn’t a left or right failure. It’s a balance-sheet failure that extracts from the young to preserve promises made to the old. It’s a system that has also changed the rules mid-game... the way Japan just did, quietly adjusting bond-holding requirements for insurance companies so the whole edifice doesn’t collapse under its own demographic math. Or by a Federal Reserve buying agency debt to prop up housing prices, engaging in rounds of Quantitative Easing that benefit the Top 10% of asset owners, or introducing non-QE programs aiming to achieve the QE-like outcomes, while denying their intended goal and changing the name to “reserve management.” The anger, confusion, and search for answers are not irrational. It is the perfectly rational response of a generation that was handed the bill for a party it never attended. The Bank for International Settlements estimates that aging could push inflation structurally higher by roughly 3 percentage points over the coming decades... That’s not a one-year spike, but a permanent upward shift in the baseline. Combine that with today’s 6% to 8% debasement estimate, and the total hidden tax on holders of cash and nominal bonds could approach 10% to 11% annually. The gap between what you earn and what you lose is the extraction. Demographics are widening it every single year. The Exits Don’t ExistI’ve said a lot so far… and I’m aware that there will be pushback… First, there will be those who argue that “Immigration fixes this.” No, immigration doesn’t fix the math. It just slows the slope. Immigration redistributes workers across borders. It doesn’t create NEW ones. None of these arguments changes the dependency ratio itself. They only delay its consequences. The high-fertility nations that supply workers are urbanizing… which means their birthrates are declining as well. And I remind people that immigrants age, too. They qualify for the same benefits systems over time. So, that statement doesn’t solve the dependency ratio. It just rents more time… And I’m not trying to buy or rent more time… I’m trying to show you what to do about this. Next, there will be people who say that “Productivity has always saved us.” Yes, every major productivity revolution has been remarkable. But do you know what the ages of tractors, electrification, and computing also aligned with? An expanding labor force. The U.S. labor force has been ticking higher, but participation is falling…

We’re looking at a period where we’ll need productivity to carry the load while workforces shrink faster. Today, services dominate U.S. GDP. You know what services resist more than manufacturing does? Productivity gains. That’s the big bet here on Generative AI… The compounding nature of productivity is real, but it’s not exponential. That’s the promise we keep hearing… that it will be. But it still doesn’t solve the entitlement crisis. Next, the MMT crowd will just say, “Sovereign debt doesn’t matter because governments print their own currency.” That’s… my point. We have a printing press… BRRRR… A sovereign nation can always fund financial obligations in its currency. That’s the problem. They’re telling you that the system is “working” because it’s not formally defaulting on its obligations. I’m simply telling you who ends up paying for all of this. The person who holds that currency… every single time… the person whose past, present, and future is being taxed by an extractive currency system. Finally... to anyone who says “This is just pessimism dressed as math...“ Bring me other math. Show me a competing model, or a different set of numbers. I've seen the proposals for robot and AI taxes, and the arguments about how AI will create new human jobs. But even if you tax the machines, someone has to write the tax code, set the rate, and enforce collection on technology that evolves faster than any legislature can keep up with. And if AI does create new jobs, those jobs still need to generate enough taxable income to fund obligations designed for a workforce twice the size. You're not solving the math. You're renegotiating the terms of the same losing equation. Discomfort isn’t a rebuttal. I’d rather people have time to get in front of this than feel comfortable ignoring it.

The Back PageA lot of people say… “The system is broken.” But it really is working as it’s designed. It has always extracted from the young, the inexperienced, and the uninformed. It’s always delivered to the older, leveraged, and connected members of society. Over time, the ratio will get worse, the currency will get lighter, and the people holding it will lose time, energy, and money in ways they can’t fully see on a timeline that they don’t really feel. I’m going to be very candid. No politician or agency is coming to fix this. You must remove yourself from the parts where extraction is rampant. The tools exist. And the information in this section is free. This isn’t about fear. It’s about refusing to be surprised… Build income streams that don’t depend on a single payroll. Employers in a shrinking labor market will automate and merge. Side income, freelance contracts, and small digital businesses give workers real options. You might need to work for several clients. Do it. That’s freedom and eliminates any single points of failure. Also, learn how to maximize your time using the tools that are arriving on the market each day. Learn a skill that serves an aging population. Follow the money… Healthcare, elder care, estate planning, medical technology... these industries expand for decades regardless of what happens to the broader economy. In an AI-driven world, this will be where the dollars flow, and services will expand around this part of the population. They vote, and the money is earmarked. Turn some of your focus here. Stop assuming Social Security will exist in its current form. It may pay 77 cents on the dollar by 2033. You need to stop pretending that the government is going to solve this… or someone has the political will to do so. You need to own productive assets... equities, real estate, businesses... that generate cash flow independent of what might have been promised to you. Follow liquidity expansion/contraction and momentum moves in the market When they print, asset prices move higher. When capital and credit become more difficult to access, asset prices fall. I track this stuff for a living and give a lot of this insight away for free to anyone who is intellectually curious and wants to protect themselves against these trends. Read more here. The Sovereign MoveSo what do you do with a thesis like this? You don’t try to stop it. You don’t vote it away. You don’t wait for reform. You position yourself where the money is forced to go. This isn’t a call on economic growth. It’s a call on demographic gravity. Aging societies don’t just print money... they also spend it. And they spend it on things they cannot avoid, defer, or automate. That means healthcare, energy, food logistics, defense, regulated utilities, and asset management that is sitting between retirees and capital markets. These aren’t growth stories. They’re extraction stories... seen from the other side. Every category above represents a chokepoint where aging populations must send dollars, regardless of which party is in power, what the Fed does, or how AI impacts our workforce. The money flows because the people demand it. A highly durable candidate is healthcare real estate tied to the 75-and-older population. Think senior housing, skilled nursing, outpatient care facilities... these are assets rooted in inelastic demand driven by the same demographic math we just spent a mile of words describing. This isn’t a country-growth bet. It’s a demographic inevitability bet. Go long on what aging societies cannot avoid paying for. This week… we introduce a pure-play investment for this trend in a stock that offers a 6% yield and significant upside amid an aging population and increased monetary expansion to pay for it all… In addition, subscribers get access to our weekly portfolio, which includes the following investment types and their returns since our recommendations.

This portfolio is averaging double-digit gains while the S&P 500 has returned about 1% since the start of the year. For full access, enjoy a 60% discount and additional benefits coming this year as we continue to focus on key chokepoints as long-term appreciation, income, and inflation protection plays. Stay positive, Garrett Baldwin About Postcards from the Edge of the WorldThe Postcards Doctrine holds that wealth, power, and stability do not persist through innovation, morality, institutions, or financial sophistication, but through control of chokepoints that remain productive across regime change. Civilizations rise and fall. Ideologies rotate. Technologies obsolete themselves. Financial instruments are rewritten, repudiated, inflated away, or nationalized. What survives is not what performs best in good times, but what continues to function when systems fail, rules change, and authority resets. The doctrine begins with a simple observation: extraction always migrates toward what people cannot avoid. Early on, extraction flows through trade. Then finance. Then regulation. Then platforms. Then metered access. Eventually, it settles on inputs that cannot be substituted, deferred, or digitized. Postcards are sent from the edge of these transitions. Each one documents a moment when the system tightens, when optionality narrows, and when value stops flowing to innovation and starts flowing to ownership. Enjoy.

|

Post a Comment

Post a Comment