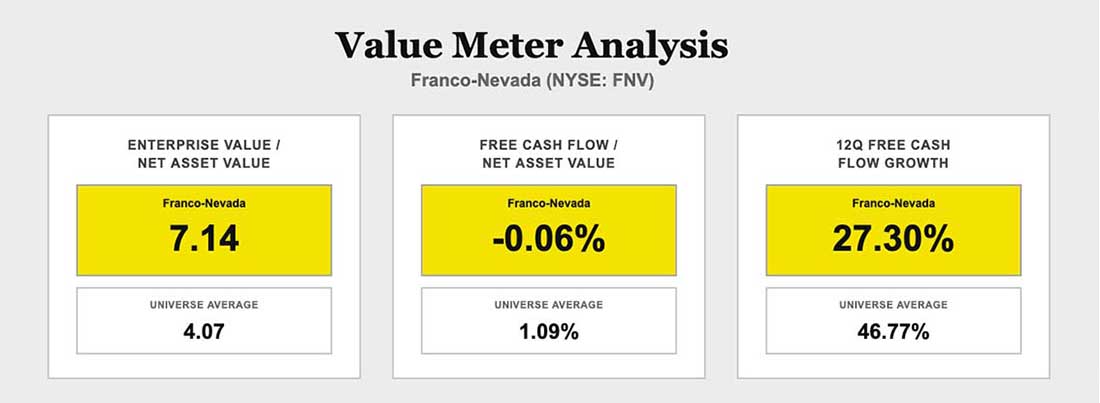

| Last week, we reviewed a gold royalty and streaming company: Royal Gold (Nasdaq: RGLD). Many of you asked about other names in the space, so this week, we're looking at a major competitor. Franco-Nevada (NYSE: FNV) operates the same core model. It provides capital to miners in exchange for royalties or streams tied to future production. Again, that means it does not operate the mines directly, limiting its cost risk and keeping its margins high. This structure allows Franco-Nevada to maintain a strong balance sheet. Diversification across assets and jurisdictions lowers single-asset risk. The company is widely viewed as a high-quality way to gain exposure to precious metals. Clearly, the stock reflects that perception. It's up more than 20% year to date and 82% in the past year. But we don't grade stocks by optics. We test whether price matches the underlying reality. Let's see if it does for Franco-Nevada. The company's enterprise value-to-net asset value (EV/NAV) ratio sits at just over 7.1, whereas the broad market averages just under 4.1. That is a very clear premium, but paying more for a company's assets can make sense if those assets convert into cash at a superior rate. Here, they do not. Franco-Nevada's free cash flow-to-net asset value (FCF/NAV) stands at about -0.1% against a market average of 1.1%. Investors are paying a large asset premium while receiving a negative - albeit only slightly - cash yield per dollar of NAV. That shifts the burden to growth. Over the last 12 quarters, free cash flow has grown quarter over quarter just 27.3% of the time, compared with a market average of just under 46.8%. What does all of this tell us about the stock's current valuation? |

Post a Comment

Post a Comment