Postcards From the Edge of the World (Vol. 11)Let's get out of America for a little while... What do you say?

To Whom It May Concern (You): I originally wrote a different lede for Volume 11 of Postcards. But two nights ago, I started reading a working paper on economics. It stopped me in my tracks. After reading The Debasement Index: Inflation’s Missing Twin, written by Vincent Bühler, a second time, I tore up my first draft of this letter. I spent my Saturday overhauling this. A few quick points before we get started… First, Bühler is a CFA Charterholder and an alum of the London School of Economics. Second, it’s still a working paper and not a finished product. It hasn’t been peer-reviewed in the traditional academic sense. There will be criticism from purists - especially those who argue no debasement is happening. But I’ve read it two times now, and it’s forced me to think hard about everything we’re told about money. I’m not talking about what money is… I’m focusing on how it’s measured. In previous issues of Postcards, we dove into the Cantillon Effect and how they extract our currency over time. This paper challenges conventional thinking. If it’s right, an entire advisory and academic world may be navigating the financial system with the wrong compass. This paper cuts to the core of what we know is wrong in our gut, but we can’t quite quantify it. How the curated government statistics argue that things are under control, but they’re clearly wrong… That we see the truth with our own eyes, even when we’re told that we shouldn’t believe our intuition. Welcome back to the Edge of the World.

The Ways They TakeI appreciate that this author puts a number on the dilution of fiat currency. This isn’t a standard government metric. It’s a lens. But sometimes a lens shows you what the official scoreboard ignores. Bühler’s insight begins with a formula that’s almost too simple for the scale of what it reveals about our monetary world... The Debasement Index = Money Supply / Real GDP. Take all the money in the system and divide it by the nation’s real economic output. And we can do this with a wide range of measures… M2.… M3… or the reading that Michael Howell offers from Global Liquidity. Go wide… If the ratio rises, the currency is being diluted further. This ratio reveals the quiet mechanism of extraction that’s been running for over a century. It’s been hiding in plain sight behind the one thing nobody ever questions... the assumption that a dollar is worth a dollar. If the ratio rises persistently, purchasing power tends to erode over time. The Pound Sterling is one of the oldest currencies in the world and is still widely used. With a millennium of use, that currency offers an ideal data set. Yes, pre-20th-century money supply data relies on historical reconstruction. The precise number may vary a bit depending on the methodology. But the long-term direction is unmistakable.

That figure isn’t inflation or what the Bureau of Labor Statistics reports. It’s the expansion of the money supply relative to real economic output… That dynamic carries consequences. Now, remember… inflation and debasement are not the same thing. Inflation measures the prices of a basket of consumer goods. Debasement measures the dilution of the currency through money creation. And it doesn’t matter if that dilution shows up in consumer prices tomorrow. Inflation is a symptom… Debasement is the mechanism by which it’s created. There can be long periods when consumer prices remain stable while debasement surges quietly in the background. Where does it go? When liquidity expands faster than goods production, excess money often finds its way into financial assets before it shows up in consumer prices. You’ve lived through this for the last six years. Stocks have gone up. Housing prices have gone up. Art prices and baseball cards have gone up… Meanwhile, the CPI moderates. Economists and those protecting the system call this “price stability.” Let’s call it what it really is: It functions as a form of extraction. What’s Beneath the NoiseThe paper doesn’t offer direct investment advice… That’s important. But I’ve inferred what works and what doesn’t if you’re trying to outrun a currency's debasement. Bühler breaks total asset returns into three components:

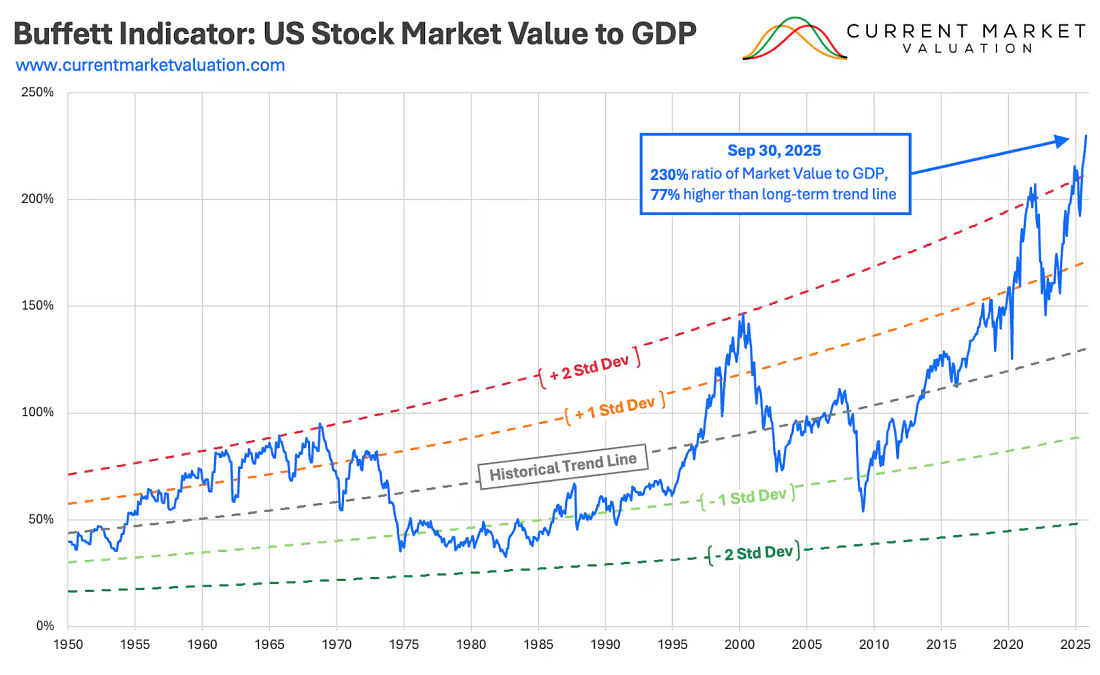

His UK data shows 6.7% annual debasement in the fiat era. That’s a number that looks familiar. Michael Howell, the founder of CrossBorder Capital and one of the most respected researchers on global liquidity flows, has argued that U.S. dollar debasement has been running closer to 8% per year since 1971. Howell’s logic is that U.S. national debt has been compounding at roughly 8% annually. Historically, debt growth and broad money expansion have tended to move in similar ranges. Sustained debt growth often coincides with sustained currency expansion. Apply that framework to U.S. markets, and the implications are worrisome. The paper implies a meaningful share of the S&P 500’s long-run nominal return is linked to the debasement component.. so a meaningful portion of what we call “stock market gains” isn’t innovation… It’s not earnings or productivity. It’s the unit of measurement that’s losing weight. It’s very possible that one of Wall Street’s favorite metrics - The Warren Buffett Indicator, a measure of Market Performance to GDP - might actually be showcasing the debasement of our currency in real time as well.

Something to think about… It turns out, equities have historically cleared the debasement rate. Even after accounting for money’s dilution, stocks deliver positive trends and speculative returns on top of the debasement lift. They’re one of the few asset classes that consistently outrun the printing press. Long-duration government bonds have struggled to keep pace with debasement, even after adjusting for monetary expansion. Bühler’s data suggests bonds “barely break even” after debasement in developed countries. So, if you’re holding a 10-year Treasury bond that yields 5%, but debasement runs from 6 to 8%, you’re falling behind. Oh, and if you’re paying a manager to deliver those returns, you’re even worse off… In periods of heavy monetary expansion, bonds have struggled to keep pace with debasement. In tight-money regimes, they can outperform. During what he calls “public waves”... periods of heavy government-driven money creation like post-2008 and post-2020... bonds may lose ground. Then, there’s the other important thing to own… WRITE THIS DOWN. Scares assets win and outperform. But abundant commodities don’t win. And this would be a huge blow to one of my academic degrees… and to anyone who thinks that farmers will be driving Lamborghinis... (Jim Rogers is a primary reason why I ended up with an agriculture degree.) After stripping out debasement, gold, palladium, and crude oil showed positive real trends of roughly 0.5% to 3% annually, according to the paper. But… agricultural commodities like wheat, corn, cotton, and sugar have shown negative trends. This implies that productivity gains have driven their real prices down over time. We’re very good at growing food in this world (and that’s a good thing.) Scarce assets with pricing power outpace the rate of debasement. Abundant ones don’t… What a simple framework… How Do We Win Once And For All?You beat debasement by owning things that are either productive or scarce. That’s it… If Bühler’s analysis is right (and I firmly agree with this analysis), you lose by holding cash equivalents and fixed-income instruments if their yields aren’t anchored to the debasement rate. (A lot of government programs are tied to CPI). Meanwhile, the Cantillon Effect shows asset holders benefit from debasement before wage earners ever see inflation-based adjustments, especially retirees living off fixed income and looking for the government to raise COLA standards. A generation of financial advice was built on the assumption that bonds provide “safety.” But what the hell is the safety from? Against volatility… okay… that’s fair. But against currency debasement? Ha. That said - as I’ll explain - bonds do pay off at one specific point in the liquidity cycle… meaning there is a time to load up on bonds. But more on that later.

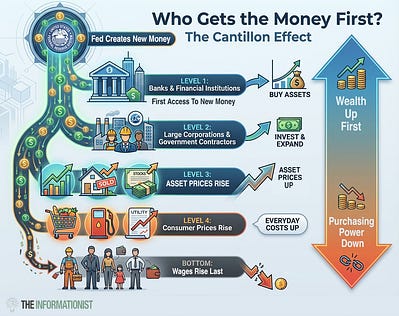

How Power Really WorksHere’s where debasement connects to the extraction framework we’ve been building at the Edge of the World since Volume 1. Debasement is, at its core, a public policy choice. Governments borrow money… Central banks create money… or allow shadow banks to create forms of credit. Commercial banks multiply it through lending… even years after a catastrophic financial crisis. Let me make this really clear. These institutions don’t have many incentives to slow down the process… regulate the process… overhaul the process… or self reflect. The government benefits because it can spend today and push the real cost into the future. We covered that in Volume 10... Remember, deficits are claims on hours that haven’t been worked yet, by people who haven’t walked through the doors yet. Central banks benefit because they manage a system that only exists because of fiat money creation and they maintain the role as lenders of last resort. Commercial banks benefit because every loan they issue creates new deposits, which the Bank of England itself has confirmed. Everyone in the top of the chain is rewarded for monetary expansion. The penalty falls on the last person in line... That’s the Cantillon Effect in its modern form.

This also explains a question that has nagged so many people for years… Why does economic inequality keep rising even when inflation appears “under control”? The answer is a terrific exercise in Occam’s Razor. We’ve been using an incomplete measurement… and incentives. Debasement is not the only driver of inequality. Technology, globalization, tax policy, and regulation matter too. But when asset prices rise faster than wages, currency dilution amplifies the gap. Bühler shows a strong visual correlation between the debasement-inflation gap and the Gini coefficient in the UK over centuries of data. When debasement outpaces inflation, asset prices rise faster than wages, and capital owners pull ahead of labor. The system has deviated over the decades, driven by institutional incentives that favor asset owners while only telling people about the role of inflation… That is how power really works... Not through edicts or decrees, but through mechanisms so boring and technical that nobody pays attention until the consequences are irreversible... And therefore… through omission of statement. The Everyday HustleIf it feels like we’re running faster and arriving nowhere, we are... Bühler’s data shows the pound’s annual debasement at 6.7% in the fiat era. Michael Howell puts the dollar at 8%. Even if you split the difference and call it 7%, your savings account pays less than the debasement rate. Our cash is on a treadmill... Yes… it looks like it’s standing still… But it’s just a sad fact that the floor is moving backward under it. When someone says “the market gains 8% a year annually,” you hear growth. But rip that number down to the studs, and you find that a big piece of those annual gains comes from debasement. Once you subtract that part out, the headline return shrinks. Safety, in the author’s debasement framework, can be misleading. The standard advice for decades has been: “As you approach retirement, shift from stocks to bonds for safety…” In a debasement-adjusted framework, that advice is the equivalent of easing off the gas while the road accelerates beneath you. The Real EconomyIf your measuring stick is shrinking, the smartest thing you can do is stop using the same ruler for everything. Most Americans have 100% of their financial life denominated in U.S. dollars... their salary, savings, stocks, bonds, house, and retirement account, all priced in a single fiat currency that has been continually eroded since 1971. That’s a huge concentration risk. We don’t talk about it much because it’s controversial. We don’t bring it up because it’s largely invisible to us. Bühler’s paper makes the invisible visible. If debasement rates differ by country, then geographic diversification is not just a portfolio strategy. It becomes a necessary form of self-defense. We’ve talked about how, in other turbulent times, rich families would own assets outside their regions. Wealthy families in Rome owned land in Spain. The elite in France in the 1700s didn’t keep everything under one kingdom (as we saw, that didn't work…). We want to focus on the intersection of two maps… We want nations with strong economic freedom and abundant natural resources. We want to invest in places that respect private property, have responsible court systems (comparatively), and have limited corruption (again, comparatively). We also want these nations to be rich in those very scarce assets that we discussed. The list isn’t that long… but it’s a good starting point. A short list includes Australia, Canada, Norway, and Chile. Of course, no nation is immune to cycles. But notice what’s not on this list? The most resource-rich countries in the world... Russia, Venezuela, the DRC, or Iran. They all rank poorly on economic freedom because resource wealth can enable bad governance and corruption. The free countries above are exceptional because they have the resources and strong institutions. Remember, the goal is not to abandon the dollar. However, we want to stop betting everything on a single measuring stick that has been shrinking by design for over a hundred years.

Household Moves... Reduce What They ExtractNot everyone is in a position to invest right now… I knew that when I started this letter. Part of my job is to help you play defense first, so the slow leak stops before you try to build. Here are moves that apply the debasement framework at the household level.

If your income is fixed... salaried, hourly, pensioned... You are structurally short against debasement. Look for ways to build variable income streams, even small ones.

Every dollar of variable-rate debt you carry is a bet that rates will stay low while the system continues to dilute. That bet has been losing for three years in a row.

Six months of fixed expenses in cash or near-cash isn’t about earning a return. It’s about making sure you never have to sell an asset or take on debt at the worst possible moment.

Get rid of subscriptions, memberships, auto-renewals, insurance policies you haven’t reviewed in years... These are small, steady claims on your stored time. Cancel anything you haven’t used in 61 days.

In a world drowning in data, the scarcest resource is judgment. AI can summarize and simulate, but it cannot own the outcome of a decision. The Sovereign MoveEach week, I offer a stock or asset I believe can provide you with a solid opportunity in the future. A way to protect against debasement or generate enough capital through a total return that you beat that fiat extraction figure. This week, we are leaving the United States. We have already showcased the value of Vale SA (VALE). But this week, I have something different… Not only does it pay a 11% gross yield, but it also trades at a discount to the sum of its parts… This is a sovereign move for investors serious about protecting themselves against a world of perpetual currency destruction. This week’s recommendation sits at the intersection of everything we’ve discussed. The debasement framework tells us what works…. investing in productive equities and scarce real assets. The geographic analysis tells us where to diversify into resource-rich, economically free nations outside your home currency. The total return logic tells us how to position for yield while you wait and for upside when the market catches up. Let’s Get ActiveThe average Postcards Portfolio position is up 8.7% since we launched in December 8, 2025. That’s beating the S&P 500 by a significant factor.

Our focus? Defense and tapping into the chokepoints of the economy and world. Today, I’m highlighting a fund that pays more than 10% and offers a discount to the sum of its parts. It invests in one of the biggest oligopolies in the financial world, one of the top gold producers, and various other companies that have built massive chokepoints across one of the world’s freest economies. To access the full portfolio and our latest pick, please join Postcards… I’ve made it easier than ever with a 60% discount and the opportunity to lock in this low annual price for as long as you’re a member. Once you’ve joined… CLICK THIS LINK FOR THE FULL COMMENTARY. Stay positive, Garrett Baldwin About Postcards from the Edge of the WorldThe Postcards Doctrine holds that wealth, power, and stability do not persist through innovation, morality, institutions, or financial sophistication, but through control of chokepoints that remain productive across regime change. Civilizations rise and fall. Ideologies rotate. Technologies obsolete themselves. Financial instruments are rewritten, repudiated, inflated away, or nationalized. What survives is not what performs best in good times, but what continues to function when systems fail, rules change, and authority resets. The doctrine begins with a simple observation: extraction always migrates toward what people cannot avoid. Early on, extraction flows through trade. Then finance. Then regulation. Then platforms. Then metered access. Eventually, it settles on inputs that cannot be substituted, deferred, or digitized. Postcards are sent from the edge of these transitions. Each one documents a moment when the system tightens, when optionality narrows, and when value stops flowing to innovation and starts flowing to ownership. Enjoy.

|

Post a Comment

Post a Comment