Hello, Thanks for signing up for MarketBeat Daily Ratings—we’re excited to have you on board. Every weekday, you’ll get a curated summary of new “Buy” and “Sell” ratings from Wall Street’s top-rated analysts, the latest stock news, and bonus investing content—all delivered straight to your inbox. You’re just two quick steps away from completing your sign-up: 1. Make sure our emails go to your inbox Gmail users:

Mobile: Tap the three dots (…) in the top right and select Move to Inbox or Move to Primary

Desktop: Click the folder icon at the top and select Move to Inbox or Primary Apple Mail users:

Tap our email address at the top (next to From: on mobile), then select Add to VIP Other providers:

Reply to this message and add newsletters@analystratings.net to your contacts 2. Confirm your subscription Click this link to confirm your subscription. This verifies your account and ensures you receive your newsletters without interruption instead of getting stuck in your spam filter. Confirm your subscription here. After you confirm, feel free to download our popular free report, "7 Stocks to Buy and Hold Forever" with this link. Thanks again for subscribing—we look forward to being part of your investing journey.

Matthew Paulson

Founder and CEO, MarketBeat. P.S. If you didn’t mean to subscribe, no problem—you can unsubscribe here.

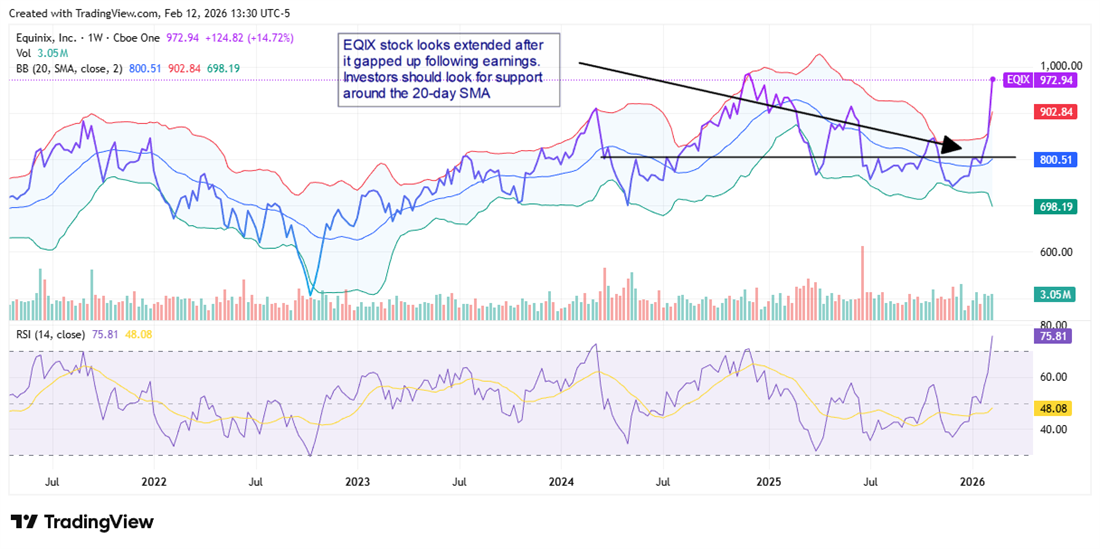

Today's Featured Story Guidance, Not Earnings, Sends Equinix Stock HigherWritten by Chris Markoch. Article Posted: 2/12/2026.

Key Points - Equinix stock rallied despite an earnings miss as 2026 guidance pointed to accelerating revenue and FFO growth tied to AI infrastructure demand.

- The company’s global interconnection platform positions it as a central hub for AI workloads, cloud access, and edge deployment.

- After a sharp post-earnings move pushed EQIX into overbought territory near analyst price targets, investors may benefit from waiting for a pullback while collecting a growing dividend.

- Special Report: [Sponsorship-Ad-6-Format3]

Equinix Inc. (NASDAQ: EQIX) stock is up more than 12% after the company reported earnings after the market closed on Feb. 11. The real estate investment trust (REIT) missed on the top and bottom lines, but it was the guidance that sent investors bidding the stock higher. Equinix projected full-year 2026 revenue in a range of $10.12 billion to $10.22 billion. That's only slightly above the consensus estimate of $10.07 billion, but it serves as confirmation that growth is accelerating. Funds from operations (FFO) is a key metric for REITs, and Equinix now projects FFO to grow by 10.5% in 2026—well above the 5% growth estimate it provided in June 2025. It's easy to see why investors liked what they heard. But after such a strong move higher, is this the time to buy EQIX stock, or should investors exercise caution? A Hub for AI Infrastructure Equinix is primarily a data center operator with 280 data centers in 36 countries. The company owns 176 of those facilities, and more than 80% of its recurring revenue comes from either owned properties or leases that don't expire until 2041 or later. Equinix specializes in "interconnection"—facilitating direct, private links between businesses, cloud providers, networks, and other digital infrastructure. In the current AI infrastructure buildout, Equinix's data centers act as hubs for multiple parts of the AI workflow. - Network hub — where you aggregate and access data

- GPU colocation — where you train and run models

- Edge gateway — where you deploy models close to end users

Companies can host all three within Equinix's ecosystem, with fast, private connections between each piece. It's the difference between having an office, factory, and distribution center in the same industrial park versus scattered across multiple cities. Equinix's guidance is also a reminder that parts of the AI story are grounded in tangible infrastructure demand—something some observers of the AI hype may be overlooking. Can Equinix's Growth Continue to Outrun Estimates? This is the question investors must consider if they're not already in EQIX stock. The post-earnings gap up has pushed the shares into an overbought range, which argues for short-term caution. Technical signals only tell you what a stock is expected to do, not what it will do. Short interest is slightly higher in 2026 but still represents only about 2% of the float. With roughly 94% of the stock owned by institutional investors, heavy short pressure seems unlikely. That said, the stock is trading around $980 per share—only a shade below the $1,000 price target Jefferies set on Feb. 12. MarketBeat's collection of analyst forecasts shows the highest price target of $1,050 coming from HSBC. Combining overbought technicals with analyst targets that imply limited upside suggests the next move could be lower.

Get Paid to Wait A compelling feature of many REITs is the dividend requirement: REITs must distribute at least 90% of their taxable income as dividends. With the share price approaching $1,000, Equinix yields about 1.96%—not a high yield by REIT standards. Still, the payout is notable. The company recently raised its quarterly dividend to $5.16. If that level is maintained for the year, the annual per-share payout would total $20.64. Equinix has raised its dividend for 10 consecutive years, with an average three-year growth rate of 11.11%. Investors who believe in the company's growth trajectory may reasonably expect total returns that move closer to the stock's long-term averages; over the past decade, Equinix's total return has averaged roughly 28% annually.

|

Post a Comment

Post a Comment