Hello, Thanks for signing up for MarketBeat Daily Ratings—we’re excited to have you on board. Every weekday, you’ll get a curated summary of new “Buy” and “Sell” ratings from Wall Street’s top-rated analysts, the latest stock news, and bonus investing content—all delivered straight to your inbox. You’re just two quick steps away from completing your sign-up: 1. Make sure our emails go to your inbox Gmail users:

Mobile: Tap the three dots (…) in the top right and select Move to Inbox or Move to Primary

Desktop: Click the folder icon at the top and select Move to Inbox or Primary Apple Mail users:

Tap our email address at the top (next to From: on mobile), then select Add to VIP Other providers:

Reply to this message and add newsletters@analystratings.net to your contacts 2. Confirm your subscription Click this link to confirm your subscription. This verifies your account and ensures you receive your newsletters without interruption instead of getting stuck in your spam filter. Confirm your subscription here. After you confirm, feel free to download our popular free report, "7 Stocks to Buy and Hold Forever" with this link. Thanks again for subscribing—we look forward to being part of your investing journey.

Matthew Paulson

Founder and CEO, MarketBeat. P.S. If you didn’t mean to subscribe, no problem—you can unsubscribe here.

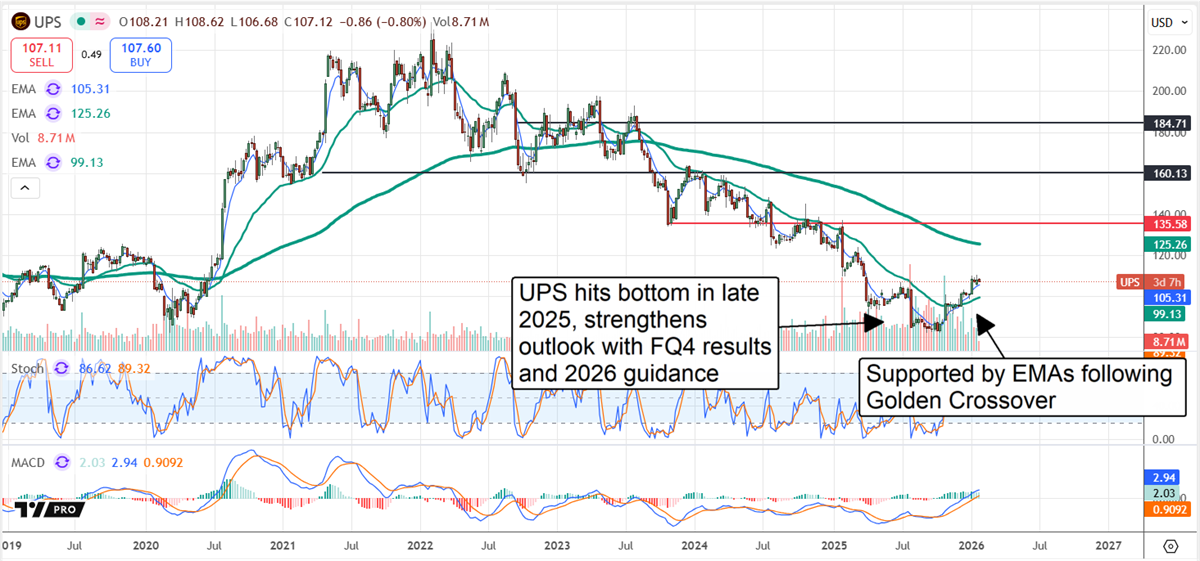

Additional Reading from MarketBeat Media United Parcel Service Transitions to Growth: Accumulation BeginsAuthored by Thomas Hughes. Date Posted: 1/28/2026.

Key Takeaways - United Parcel Service has returned to growth sooner than expected, and its stock price looks to be in rebound mode.

- An ample capital return is reliable in 2026, with distributions expected to increase.

- Analysts and institutional data align with a market bottom and reversal, and trends will likely strengthen as 2026 progresses.

The long-awaited bottom in United Parcel Service (NYSE: UPS) stock appears to be in, and a rebound is underway. Backed by stronger results, improved operational execution, and a growth-oriented outlook, the recovery could be substantial for long-term holders. After a period of heavy distribution and downward pressure from analysts, UPS has moved into an accumulation phase that may strengthen as the year progresses. Analysts and Institutions Have Shifted to Bullish The shift is visible in analyst activity. The analyst group still lists a consensus Hold, but analysts began raising price targets in late 2025. Americans are discovering a rare "29% Account" that pays 72X more than what your bank offers.

It's NEVER been advertised to the general public… the big banks and financial giants have kept it to themselves for decades.

Now it's available to everyday Americans - and banks are NOT happy about it. Discover the "29% Account" here before they try to ban it. Those bullish revisions continued into the first weeks of 2026 and look likely to gain momentum now that the 2026 guidance is public. The company forecasted $89.7 billion in net revenue — roughly 300 basis points above MarketBeat's reported consensus — signaling growth a year earlier than previously expected. Margins are also projected to remain healthy, pointing to a leveraged earnings rebound. Institutional activity is supportive as well: institutions own about 60% of this high-yielding stock and were net buyers in Q4 2025. There were sales that coincided with the stock's low, but late-quarter accumulation carried into January 2026 and appears to be strengthening. Together with Q4 strengths and the 2026 guide, this underpins a reliable capital-return program for investors. Dividend Strength and Buybacks Reward Investors Trading near COVID-era lows, UPS yields more than 6% and is expected to continue raising distributions in the coming years. The 2026 guide forecasts payments slightly above 2025 levels, suggesting another low-single-digit increase is likely. Share buybacks reduced the share count by roughly 0.7% in 2025 and are expected to continue in 2026. UPS Accelerates Stock Reversal With Strong Results UPS delivered a solid Q4 performance despite reporting a net contraction. Revenue declined 3.2%, but that was better than expected — roughly $500 million above estimates — as strength in revenue per package and international markets offset weakness in domestic volume and supply-chain solutions. Adjusted operating margin contracted as anticipated and aligned with forecasts, leaving adjusted earnings above consensus by a similar margin. That combination creates an opportunity for investors to enter early in the rebound. The earnings outlook, potential for outperformance, and shifting analyst posture all point to a cycle of bullish revisions and improved market sentiment. Under this scenario, UPS could reach the high end of early-2026 target ranges — approximately a 40% gain from the pre-release close — as upgrades and higher price targets attract buyers. UPS Advances Following Strong 2026 Guide UPS stock ticked up after the 2026 guide, finding support near its 30-day exponential moving average (EMA). That EMA is rising along with the 150-day EMA after a golden cross formed in December 2025. This technical signal aligns with accumulation and improving market conditions, and if these EMAs continue to hold, a more significant price rebound may follow.

Key catalysts in 2026 include persistent growth, margin recovery, and outperformance. UPS's push into digitization, automation and AI should gain traction as business quality improves. The decline in Amazon-related volume is expected to stabilize as the company shifts its mix toward higher-margin consumer and enterprise traffic. Industry-specific focus — notably healthcare — should also drive growth, with UPS targeting specialized, time- and temperature-sensitive transportation solutions.

|

Post a Comment

Post a Comment