Hello, Thanks for signing up for MarketBeat Daily Ratings—we’re excited to have you on board. Every weekday, you’ll get a curated summary of new “Buy” and “Sell” ratings from Wall Street’s top-rated analysts, the latest stock news, and bonus investing content—all delivered straight to your inbox. You’re just two quick steps away from completing your sign-up: 1. Make sure our emails go to your inbox Gmail users:

Mobile: Tap the three dots (…) in the top right and select Move to Inbox or Move to Primary

Desktop: Click the folder icon at the top and select Move to Inbox or Primary Apple Mail users:

Tap our email address at the top (next to From: on mobile), then select Add to VIP Other providers:

Reply to this message and add newsletters@analystratings.net to your contacts 2. Confirm your subscription Click this link to confirm your subscription. This verifies your account and ensures you receive your newsletters without interruption instead of getting stuck in your spam filter. Confirm your subscription here. After you confirm, feel free to download our popular free report, "7 Stocks to Buy and Hold Forever" with this link. Thanks again for subscribing—we look forward to being part of your investing journey.

Matthew Paulson

Founder and CEO, MarketBeat. P.S. If you didn’t mean to subscribe, no problem—you can unsubscribe here.

More Reading from MarketBeat.com Diamondback Sees Resilient Demand Despite Cautious GuidanceAuthor: Chris Markoch. Published: 2/26/2026.

Key Points - Diamondback Energy’s disciplined production outlook signals a supply environment that could help support higher oil prices into 2026.

- Strong free cash flow is funding dividend growth and share repurchases, reinforcing the company’s shareholder-return story.

- FANG stock remains technically constructive, with analysts projecting moderate upside as energy sentiment improves.

- Special Report: [Sponsorship-Ad-6-Format3]

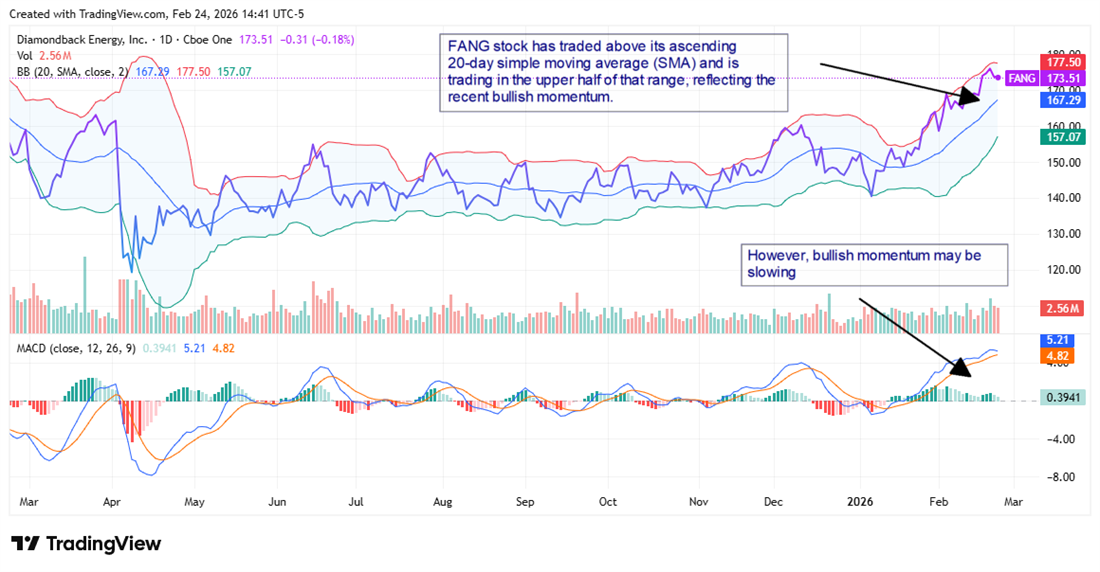

Diamondback Energy Inc. (NASDAQ: FANG) stock has almost recovered all its pre-market losses after delivering its Q4 2025 earnings report on Feb. 23. The headline numbers were mixed, with a slight earnings miss offset by a topline beat. However, the company issued cautious guidance that may have dampened initial enthusiasm. It's a reminder that underpromising and overdelivering is something investors applaud — once companies actually overdeliver. Still, there was plenty to like in Diamondback's report, including a more optimistic view on the supply-demand outlook for crude oil in 2026. Diamondback believes demand will remain resilient. The company delivered a cautious initial read of its 2026 guidance, which keeps output roughly in line with the final three months of 2025. That forecast, however, may not fully account for potential upside in crude oil prices in the coming months. Disciplined Production Could Support Higher Oil Prices As of this writing, the April contract price of West Texas Intermediate (WTI) crude oil is $65.94 — roughly 20% above the price at the beginning of the year and about 40% higher than some analysts had expected. That matters for Diamondback's earnings. Rising crude prices have lifted the whole energy sector, but concerns about a supply glut still weigh on producers — especially those responsible for bringing oil to market. In its report, Diamondback noted that demand has remained resilient, suggesting December 2025 may have put a floor under crude prices. Several points in Diamondback's presentation support the case for a sustained move higher in crude. First, the company's 2026 production guidance of 500–510 Mbo/d represents only modest growth from 2025, signaling a disciplined industry posture that could keep supply from overwhelming demand. Second, Diamondback's scenario analysis shows that even at $70 per barrel the company expects to generate over $5.5 billion in free cash flow. That implies management views meaningful upside from current prices as a realistic base case rather than a stretch target. There is also a structural gas story that could indirectly support oil. Diamondback is expanding its long-haul gas pipeline commitments, raising its forecast from roughly 350,000 MMBtu/d today to 800,000 MMBtu/d by Q4 2026. That expansion would reduce the WAHA pricing drag that has historically weighed on Permian producers' realizations. As that headwind fades, Permian economics improve, reinforcing the case for continued capital discipline across the basin. Fewer wells drilled industry-wide tends to tighten supply, which can push prices higher. Dividend Growth Reinforces Long-Term Investor Appeal The cyclical nature of energy stocks — oil names in particular — is one reason many pay attractive dividends. A highlight of Diamondback's report was a 5% increase in its quarterly dividend, marking seven consecutive years of dividend hikes. That payout appears well supported by the company's growing free cash flow. Diamondback said the dividend is secure as long as crude oil prices remain above roughly $37 per barrel. The company also repurchased approximately 2.9 million shares in Q4 and has about $2.3 billion remaining on its authorized $8 billion share-repurchase program. Technical Indicators Point to Consolidation, Not Reversal On Feb. 20, the last trading day before its earnings report, FANG stock popped to its 52-week high, capping a rally that began at the start of the year. This pattern has been true for many energy stocks, which have been range-bound in recent years as demand lagged record output. That made any slip — like the slight earnings miss — likely to produce a pullback. Volume is slightly above average on the day, and the initial dip appears to have been driven by algorithmic trading. Traders began buying that dip midway through the session. FANG remains above its rising 20-day simple moving average (SMA). The Bollinger Bands are notable: the upper band sits at $177.50 and the lower band at $157.07, while the stock at $173.51 trades in the upper half of that range, reflecting recent bullish momentum.

The moving average convergence/divergence (MACD) also paints a broadly constructive picture: the MACD line at 5.21 remains above its signal line at 4.82, though the narrowing gap suggests near-term momentum may be fading. Momentum appears to be slowing, which could see the stock pull back toward the SMA — currently around $167.29 — before making its next move. Analyst forecasts for Diamondback Energy on MarketBeat show a consensus price target of $187.33, about an 8% upside from the stock price at the time of writing. Sentiment has been bullish since the start of the year, and that tone continued post-earnings with TD Cowen upgrading FANG to a Strong Buy.

|

Post a Comment

Post a Comment