Dear Fellow Investor,

Recently, a $200 billion bet was placed against every data center in America.

And almost nobody saw it coming.

I’m George Gilder. I’ve been calling tech revolutions for over 40 years.

Smartphones in 1991. Streaming in 1994. Amazon in 1996.

Early investors in those calls could have seen gains of 249,900%… 112,700%… and 216,100%.

Now I’ve identified something that could make all of them look small:

A radical new chip architecture – backed by the Trump administration and its $200 billion bet…

That processes data up to 100X faster using 90% less energy.

Three companies are converging to make today’s AI data centers obsolete.

Wall Street hasn’t connected the dots yet.

But the smart money – Vanguard, BlackRock, Morgan Stanley – has already poured billions in.

Once the third company IPOs, the window slams shut on the biggest profits.

>> Get all three company names before the fuse is lit <<

To the future,

George Gilder

Editor, Gilder’s Technology Report

Macy's Beats Expectations Again, But Guidance Spooks Investors

Written by Jennifer Ryan Woods. Originally Published: 3/24/2026.

Key Points

- Macy’s stock surged more than 140% from its April 2025 low to a December high above $24 as investors gained confidence in the company’s “Bold New Chapter” turnaround strategy, but shares have since pulled back sharply in 2026.

- The company delivered another strong fourth-quarter report, beating earnings and revenue expectations for the fourth consecutive quarter, a sign that the turnaround strategy is gaining traction.

- Despite the solid results, Macy’s conservative full-year guidance and uncertainty around discretionary spending prompted several analysts to lower price targets, leaving the stock with a Reduce consensus rating.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Macy’s Inc. (NYSE: M) was a must-have stock for many investors in 2025 as Wall Street applauded the retailer’s progress on its turnaround and a string of better-than-expected reports. Recently, however, the shares have fallen out of favor.

Shares pulled back sharply in 2026 as momentum slowed amid an uncertain macroeconomic and geopolitical backdrop that has clouded the outlook for consumer spending. Although Macy’s again delivered a beat on the latest quarter, analysts grew more cautious after the company issued conservative guidance.

Strong 2025 Rally Fades as Consumer Spending Concerns Weigh on Macy’s Stock

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidMacy’s shares hit a 52-week low below $10 in April 2025 as the traditional department-store model came under pressure. The stock regained momentum later in the year as investors grew more confident that the company’s 2024 "Bold New Chapter" strategy was beginning to deliver.

The initiative aims to reposition the company by closing underperforming stores, expanding in the luxury segment and improving operating efficiency.

That confidence helped the stock surge roughly 140% from the April low, with shares topping $24 in December. Momentum has since cooled, however, as concerns about discretionary spending have moved to the forefront.

By the end of 2025 the stock settled near $22; in the first two months of 2026 it generally traded between $20 and $22. The shares began trending lower in late February and, by the time Macy’s reported its fourth-quarter 2025 earnings on March 18, had slipped below $17.

Following the earnings release, shares rose more than 6% over the next two sessions but the gain wasn’t enough to end the downtrend. Trading around $18, the stock is down roughly 15% over the past month, a move broadly in line with the retail sector, which has fallen about 16% over the same period.

Earnings Beat Again, But Cautious Outlook Tempers Enthusiasm

Macy’s fourth-quarter report offered another sign that the turnaround is progressing: adjusted earnings per share of $1.67 topped consensus of $1.55, while revenue of $7.92 billion beat estimates of $7.48 billion. It was the company’s fourth consecutive earnings beat.

Strength at Bloomingdale’s and improving results at its "go-forward" stores — those slated for upgrades and modernization — were notable positives. Macy’s mid- and upper-income customer base also helped, since those shoppers have been less affected by pressures weighing on lower-income consumers.

Despite the upside, Macy’s conservative guidance rattled investors. On the earnings call, CEO Tony Spring reiterated confidence in the company’s long-term plan but said management is "taking a prudent approach to guidance" given macroeconomic and geopolitical uncertainties that could affect discretionary spending.

The company sees full-year net sales of $21.4 billion to $21.65 billion, same-store sales ranging from down 0.5% to up 0.5%, and earnings per share between $1.90 and $2.10. Macy’s said the conservative outlook gives it flexibility to respond to changes in the competitive and macro environments.

Analysts Lower Price Targets As Most See Limited Upside

After the report, several analysts trimmed price targets, signaling that while the turnaround thesis remains intact, near-term upside appears limited.

The consensus rating on the stock is Reduce, based on 14 analyst opinions: 10 Hold, three Sell and one Buy.

That stance is slightly more bearish than the broader retail sector, which carries a consensus rating of Hold.

The average 12-month price target for Macy’s is $18.90, implying under 5% upside from current levels and suggesting the shares may remain range-bound unless discretionary spending meaningfully improves.

For now, Macy’s appears to be walking a fine line between improving execution and navigating a challenging macro backdrop.

While the company continues to deliver better-than-expected results, the combination of cautious guidance and a muted analyst outlook suggests investors may need a clearer catalyst before the stock regains widespread favor.

Chewy Gobbles up Market Share in 2026: Poised to Advance in Q2

Written by Thomas Hughes. Originally Published: 3/27/2026.

Key Points

- Chewy is on track to rebound in 2026 as its growth, margin, and cash flow invigorate buyers to action.

- Industry-leading growth and market share gains underpin the outlook.

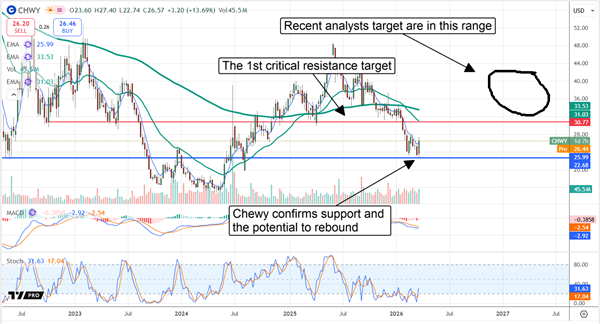

- Optimistic earnings outlook triggered a buying event, confirming support at a critical level.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Chewy (NYSE: CHWY) stock faces headwinds in 2026, as do many retailers. However, its digital-first, asset-light model is working and the company continues to gain share, as evidenced by an industry-leading growth pace. Chewy consistently outgrows peers and the broader pet-care industry, driven by rising digital penetration globally and a greater focus on nutrition and pet healthcare. The takeaway for investors is that this stock rallied by double-digits following an otherwise tepid release, indicating market support and the potential for additional gains this year.

Chewy Leads Market in Q4: Guides for Strength in 2026

Chewy delivered a solid quarter despite a tough comparison to last year and mixed expectations. The company reported $3.26 billion in net revenue, a 0.5% gain on an as-reported basis and an 8.1% increase on an adjusted basis (adjusted for an extra week). The results were driven by a 4% increase in active customers, a 2.2% rise in sales per active user and a 4.8% increase in autoship sales.

Do this before SpaceX IPOs or be sorry (Ad)

When Elon's SpaceX IPO officially hits — which could be just days from now — two things will happen.

Elon's 40% stake will immediately earn him around $625 billion in new wealth. Then millions of small investors will buy SpaceX's stock, hoping to strike it rich.

Unfortunately, many of them will be disappointed.

That's why I'm urging you to take advantage of this pre-IPO SpaceX play while you still can.Autoship sales are a critical element for the business because they represent sticky, monthly revenue tied to food, medicine and healthcare products. Autoship accounted for 84% of net sales, giving Chewy a solid foundation to accelerate growth in 2026 and provide investors with clearer revenue visibility.

Margin news was mixed. The company widened its margins across the board, contributing to a 30.4% increase in adjusted EBITDA, a 72% increase in net income and a 47% jump in free cash flow (FCF), but some metrics still fell slightly short of expectations.

Adjusted earnings per share (EPS) declined by a penny year over year and missed consensus, but were sufficient to support cash build-up on the balance sheet while maintaining a low debt level and continuing share repurchases.

Chewy’s buybacks aren’t robust, and they did not materially reduce the share count in fiscal 2026; however, they offset share-based compensation and are likely to increase over time. Management is forecasting margin improvement and an accelerated pace of earnings growth. As it stands, the long-term outlook is for a high-teens to low-20% compound annual EPS growth rate, which has the stock trading at roughly 9X its 2031 EPS forecast. While valuation is a concern today, that projection implies meaningful upside potential over the next few years.

Guidance was the key catalyst for CHWY’s post-release price action. Revenue guidance was in line with expectations and the earnings outlook was upbeat. The company forecasts FY2027 adjusted EPS at about $13.68, nearly a dime above MarketBeat’s reported consensus.

Analysts Put Bottom in Chewy Stock: Institutions Pose Risk

The analyst response to the release was mixed, mirroring the results. Early updates included positive commentary on earnings strength and 2026 guidance but were offset by reductions in price targets. The net effect left Chewy with a Moderate Buy rating and an 80% Buy-side bias, though the consensus price target was moderated. That consensus still implies roughly 60% upside this year, but many of the post-release revisions landed at the lower end of the range.

Even so, the new targets suggest there is still upside potential, with most forecasts clustering in the 20% to 50% range. These targets support Chewy stock's potential to rebound, leaving room for positive revisions later this year if momentum continues.

Institutional activity is a key risk. Institutions own more than 90% of Chewy’s shares and reduced positions in early Q1. If that selling persists into Q2 2026, CHWY may struggle to clear key resistance. As March closes, the near-term resistance is around $20.75 and could be tested before the quarter ends. The opportunity would come if institutions return to accumulation, which would help establish a stronger market bottom and open the door for a rebound.

Chewy’s catalysts include successful execution of its high-margin strategies, such as Chewy Vet Care, private-label expansion, AI-driven efficiencies and growth in its advertising business. Chewy enables manufacturers to advertise directly to consumers on a pay-per-click basis and uses AI across its platform to improve efficiency. Private labels are a growing area, driving both margin expansion and market-share gains versus premium brands.

This email communication is a sponsored email provided by Eagle Publishing, a third-party advertiser of MarketBeat. Why did I receive this email message?.

If you have questions or concerns about your account, please feel free to contact MarketBeat's U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place, Suite 620, Sioux Falls, South Dakota 57103-7078. United States of America..

Post a Comment

Post a Comment