You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. Moody's Said "What?" And... It's A Saturday Chart Party10 Charts... 10 Stories... One Party... and a dive into Moody's "liquidity crisis" statement.Editor’s note: For New Readers, welcome to Me and the Money Printer. In this Substack, I explain how liquidity, incentives, and momentum move markets, so readers can trade and invest with the tide rather than against it. I explore the global financial markets with the respect and reverence they deserve, which is none. What do you get out of it? I answer that here. Finally… each weekend, we have a Chart Party… I look at a chart… and celebrate it. But first… some more on private credit…

Dear Fellow Traveler: My two-sentence forecast for 2026 was simple…

Well… Moody’s Marc Pinto went on CNBC on Friday and said that private credit is facing “a liquidity crisis, not a credit crisis.” That’s technically possible, and also a little strange. If this isn’t a credit crisis, then what exactly is the “credit” in private credit referring to? The industry built a credit product where the only real risk anyone talks about is the liquidity of the wrapper around the credit. I’m dizzy already. That’s a bit like telling me the fire department doesn’t deal with fires. I was just happy that someone on CNBC said “crisis” and admitted where we are. But I think it’s worth understanding what Pinto’s distinction means, because the difference is smaller than it sounds. A credit crisis happens when loans are bad, borrowers can’t pay, and the money’s all gone. That was 2008... Among other things, there was a ton of bad underwriting, falsified income, and adjustable-rate mortgages resetting in waves of default. The loans themselves were the problem (though some later just blamed poor people). In a liquidity crisis, the loans might be fine. However, the structures built around them can’t handle everyone wanting their money back at the same time. Liquidity, in the textbook sense, means the ability to convert an asset to cash quickly without materially affecting its price. (We use a second definition at Money Printer.) In this case, the assets are real and borrowers are paying interest… However, these private vehicles promised quarterly liquidity. Now, too many investors are demanding money back all at once. This creates “liquidity mismatches.” (If you’re new here, I’ve written countless recent articles for you on these issues. Please check them out.) That mismatch scenario is what Pinto’s describing. So… on a technical level, he’s right. But... That’s How It Starts… (We Go Back to Your House)…Credit crises rarely announce themselves as credit crises at the start of a major event. They usually start as liquidity problems. They only later become solvency problems once markets are forced to price the assets honestly. That pattern is predictable enough… The distinction should make you curious at best and concerned at worst... Liquidity stress forces asset sales because a fund needs cash to meet redemptions. Forced sales create price discovery on assets previously marked by models built by people who chose financial engineering over mechanical engineering. Price discovery could reveal that the original marks were generous, because they always are when nobody is forced to sell. The thing is that a liquidity crisis can become a credit crisis because the assets aren’t worth what you told everyone they were. That dynamic has shown up in certain marks. Blackstone had already cut the value of its Medallia loan to about 87 cents on the dollar, and later marked it down again to around 78 cents. One of BlackRock's business development corporations (BDCs) just wrote a $25 million loan at 0 cents, three months after valuing it at par. Those are two examples, not proof of a full systemic blowup, but it does illustrate how price discovery begins. When stress rises, spreadsheet values inch at market reality… then suddenly… Funny how price discovery works… isn’t it? Everything is worth par until somebody actually has to sell it. Even before a forced sale, the direction of price discovery is always lower, right? A man shows up at a pawn shop with a watch and says… “This is a Rouchefoucauld. The thinnest water-resistant watch in the world. Singularly unique, sculptured in design, hand-crafted in Switzerland, and water resistant to three atmospheres. This is the sports watch of the '80s. Six thousand, nine hundred and fifty five dollars retail!” “You got a receipt?” the pawn shop owner says… “In Philadelphia… it’s worth $50.”  Is Private Credit the Equivalent of MBS in 2008?I’ve been thinking a lot about Michael Batnick’s question on comparing private credit to mortgage-backed securities (MBS). As I said… There were many similarities. But I thought of a better example that I think we should all consider… I will say 2008 probably isn’t the BEST comparison… If you want the uncomfortable historical comparison, you have to go back to a time when the financial system ran on top hats, whiskey, and J.P. Morgan’s checkbook. The Panic of 1907 wasn’t called a “credit crisis” either.

The National Bureau of Economic Research (NBER) even published a paper on this. The comparison and title prove it’s fine to drink before noon. The authors drew a line from trust companies to the shadow banking system that blew up in 2008… As the NBER put it, trust companies were “less regulated than commercial banks, held low cash reserve balances, and did not belong to the city's private clearinghouse, which could act as a lender of last resort.” [Page 2]. With the right type of squint and scotch, you can draw that same line straight through to private credit BDCs and private credit in 2026. Replace “trust companies” with “interval funds,” and that sentence rhymes today. Now… private credit funds aren’t by definition trust companies, and today’s investors can’t line up outside the building to withdraw their money tomorrow morning (they have designated redemption periods that are clearly outlined). But the structure and its vulnerability are familiar… We have illiquid assets paired with promises of liquidity in vehicles that sit outside the system's safety net. As I noted yesterday, crises don’t start with the crisis “thing” itself. That thing needs a trigger. The trigger in 1907 wasn’t even a credit event. In their abstract at NBER, the authors note:

A primary trigger for 1907 was a failed attempt by two speculators to corner the copper market. That failure was linked back to the Knickerbocker Trust through the owners’ personal relationships, not through the Trust’s actual loan book. When confidence broke, the National Bank of Commerce refused to clear for Knickerbocker. Then, depositors yanked millions from it in a day. The trust suspended operations. The loans may have been fine, but they didn’t matter anymore. The problem soon spread to healthy trusts with no accounting issues because they all shared the same structural challenge. JP Morgan had to step in because there was no Federal Reserve. The Panic of 1907 is the primary reason why the Fed was created in 1913. And after the Fed was created, official language shifted away from the old vocabulary of panic, even though the phenomenon never disappeared. We still had bank runs in the 1930s and moments Ben Bernanke himself described as “a classic financial panic” in 2008, and the regional banking crisis of 2023 was a textbook “panic” event (this time involving social media). But the preferred terms of our time are now crises, recessions, corrections, dislocations, contagion events, and my favorite… “periods of market stress.” They created the Fed to shift away from the threat of old-fashioned, no-backstop Panics. I think it’d be great to bring back the word “Panic…” It’s a great word. It fits the post-2008 world well. “PANIC” forces us to confront non-stop policy accommodations that benefit Wall Street and impact everyone else through the Cantillon Effect of monetary expansion. But “Panic” is a scary word to politicians and policy makers… So when a Panic really comes, the Fed and Treasury will probably tell us we’re just experiencing “a modest repricing of liquidity expectations”… while the rest of us start boiling our boots. Private credit in 2026 has recreated a rhyme of the pre-1913 problem. These funds operate outside the Fed’s safety net. That doesn’t mean the Fed can’t stabilize markets indirectly. It often does… and blatently over the last 18 years… and then they just pat us on the head and call their actions anything but QE or Yield Curve Control. (It’s just maintenance. my boy…) But these interval funds don’t have direct access to a lending window or safety net. If confidence breaks and redemptions cascade, who plays JPMorgan? Boaz Weinstein offering 65 cents on the dollar? Should Blackstone make everyone go into a library for a weekend and create private bailouts like Morgan did… or Paulson did with bank leaders in September 2008? Or does it even matter… and should I just be outside throwing a ball my dog won’t even fetch, then just stare at me, thinking… “What does this guy want from me?” As John Tuld says in Margin Call… “It's just money; it's made up. Pieces of paper with pictures on it, so we don't have to kill each other just to get something to eat. It's not wrong. And it's certainly no different today than it's ever been.”

That’s just the way it is… The Structure. Always the StructureI remind you that private credit didn’t stumble into this problem by accident. This structure exists because investors wanted yield, managers wanted fees, and nobody asked serious questions about how the liquidity part works. Those who did were told they were scaremongering… or to just get on board… read the prospectus. The interval fund structure, quarterly liquidity gates, mark-to-model accounting, and the ability to borrow against illiquid assets create the appearance of liquidity. None of it is illegal or even frowned upon... They walked right up to the line that separates regulated banking from shadow banking and set up shop on the shadow side, because that’s where the fees were. The major difference between 1907 and now isn’t that the system eliminated the problem or that the Fed exists as the ultimate lender of last resort… It’s that the system became more compliant… and then they sold it to individual investors, who were chasing yield, just as depositors chased higher returns at trust companies about 120 years ago. The whole thing now features better disclosure agreements, new legal interpretations that I’ll never comprehend, and much, much longer documents. Documents that people are only now realizing what they actually signed. Yeah… that happened a lot in 2008-09 too… Let’s Wrap This Up and Look at ChartsMarc Pinto says it’s a liquidity crisis, not a credit crisis. Fair enough, for now. But the pattern in 1907 was similar… confidence broke before the underlying assets could be fully tested in the market… Then, eventually liquidity cracked… then valuation pressure followed… and then credit questions stopped being theory… The crisis only ended because one man with enough money decided to step in. We don’t have that man anymore (but Larry Fink, feel free to step on up...) We now have the Fed. Of course, the Fed doesn’t backstop private credit. The discount window is for banks. The standing repo facility is for primary dealers and banks. Private credit funds are one or two degrees removed from the Fed’s money faucet… and each degree adds strains, costs, and counterparty concerns. Even if the Fed pumped money into the system, private credit funds would still need banks willing to lend against assets that aren’t valued properly. If banks started tightening credit lines to funds rather than extending them, any Fed liquidity injection could worsen the confidence problem... and speed up the process. Those credit issues with funds were an issue in 2008. Finally, I’ve had some people tell me that I’m overreacting… or spreading fear… or that I’m missing some element of the system that justifies its existance… I explain that I’m pointing a camera at something that’s incredibly complex and difficult to explain to ordinary people, trying to make sense of this financial system. And then they’ll reply somewhat condescendingly, "it’s all fine," and tell me something that only makes the situation worse… It sounds like…

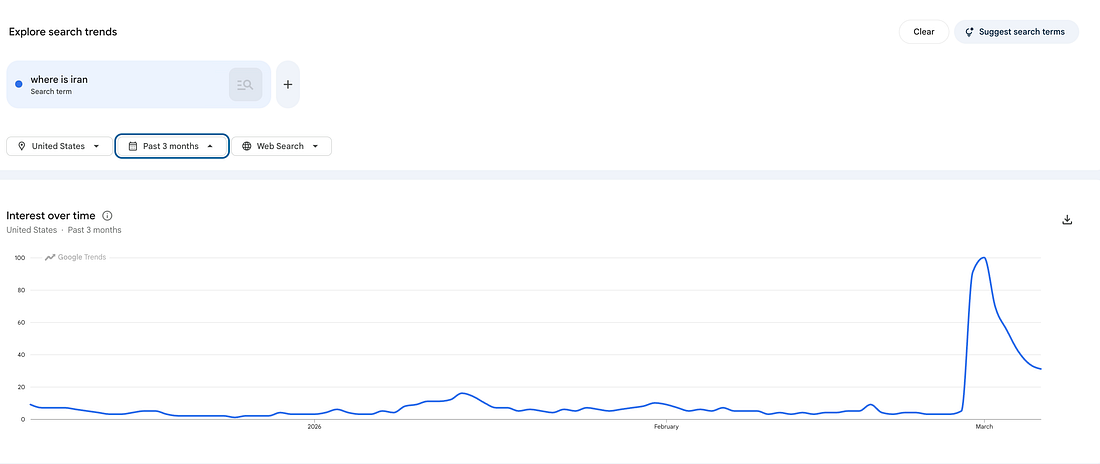

That’s a complicated way of saying “we lend money and hope they pay us back…” But you’re saying it in a way that honestly means nothing. My Lord… John Tuld was right… Let’s look at some charts… Chart 1: Come On, Man…Here are past month… Google search trends for “Where is Iran?”

So… I guess nothing has really changed in our geographical prowess, huh America? Back in 2014, a survey asked 2,066 Americans to locate Ukraine on a map. Only 16% got it right… Here’s the heat map… As you can see, a bunch of people went to pick what’s actually Iceland, Greenland, and - checks notes - Iowa?

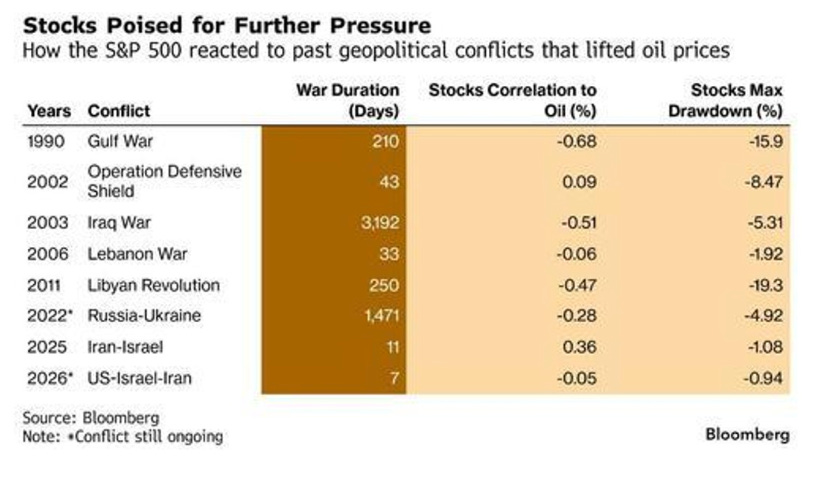

This country is awesome… Chart 2: Get Your War OnSo… where is this market heading with the War in focus. History, according to Bloomberg, suggests that we’re looking at some drawdowns here… right?

Well… If that’s the case… Just change the word “Iraqi” for “Iranian,” I guess…

Here’s the thing about that chart above. They’re aligning the Libyan Revolution that started in February 2011… with the European Credit crisis that followed much later. Remember… triggers. The Libyan Revolution didn’t create the Eurozone Crisis, but it did fuel inflationary pressures, driven by rising oil prices and the threat of pushing the Eurozone into a recession… Things got weird after that… The Treasury Department will soon announce a new program to combat rising oil prices. I think the plan was to send people checks from tariffs… But that’s out the window.

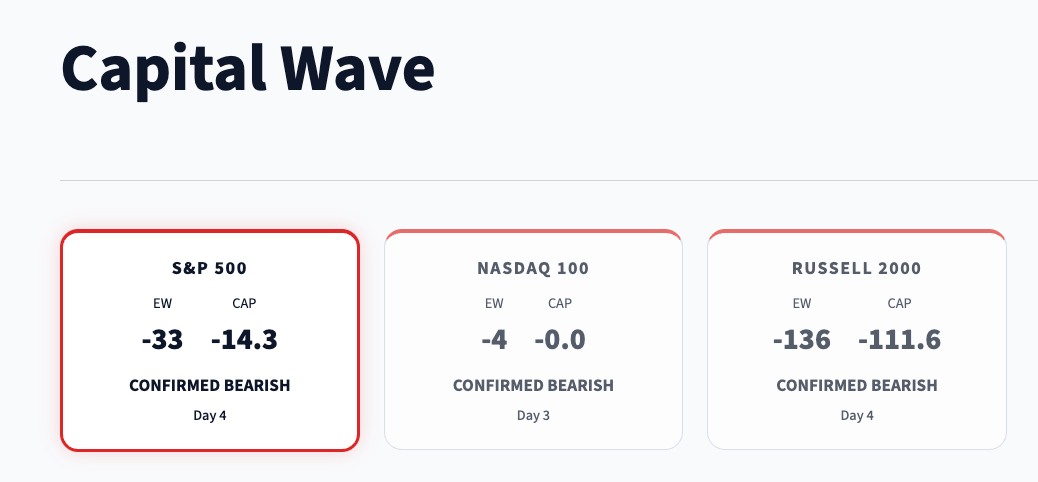

Details of the program weren’t announced, since I assume they only just started putting it together after announcing it. CAN’T WAIT! Chart 3: The State of Momentum…Just in case you’re new here… we use a reading based on the work of many academic studies on reversion momentum and market risk… We score the Nasdaq… but the more important figure is built around the S&P 500…

We’re not saying to sell everything when it’s red… but understand that risk is very elevated in those periods… For more on this reading… go here. Chart 4: Something Is Coming… It’s a Matter of WhenRemember… It’s not just the FNGD… which we watch for deleveraging… The FAZ is the Financial 3X Bear ETF… It will tell us if there’s stress… and we don’t like this over its 50-day or 100-day.

They’ll keep telling us everything is fine… But FAZ is saying we’re having a bad time.

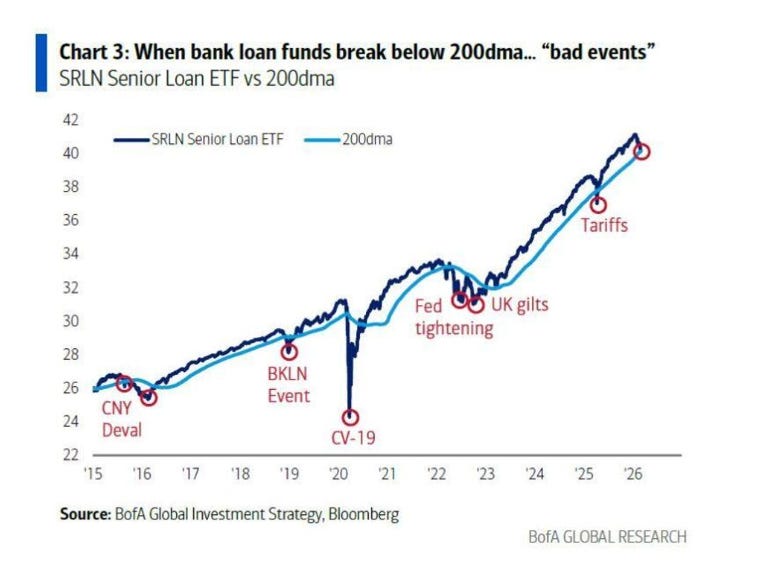

Bank of America said the other day that when bank loan funds fall under their 200-day moving average, things aren’t going well… It leads to significant events like…

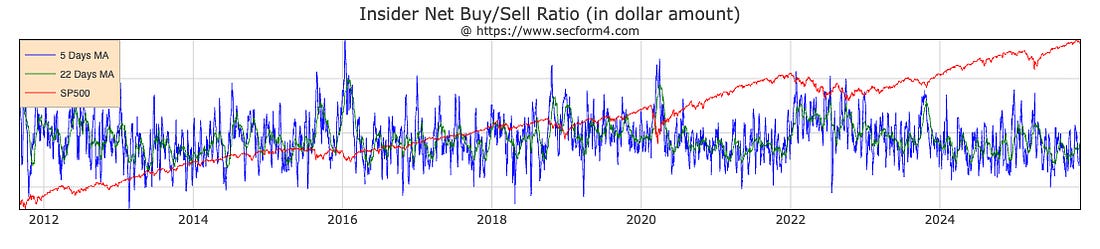

China’s currency devaluation in 2015… or the GILT crisis in England in 2022… Private credit, writes Syz Group, might be an early indicator of something bigger. Something that sounds familiar… like something I might have written… Hey… you know what's happened in every scenario, though? A policy accommodation… followed by MASSIVE levels of insider buying… as measured on the five-day moving average of the buying-to-selling ratio in real dollars (Form 4, direct purchases).

And then… as the red line shows (the S&P 500), another move higher…

So let’s watch policy makers and the insiders… and let’s look for fun time rallies… Chart 5: Go Higher… Would Ya?Submitted without much comment… This chart starts in March 2024, when we released The Hedge of Tomorrow Report, which discussed the coming surge in monetary inflation and Treasury actions…

Gold, silver, and real assets were all on the list… Hedge of Tomorrow 2.0 is coming out this month… I’ll let you know more soon. But I don’t think the GDX is done running yet. Chart 6: Oil… That’s SomethingSubmitted without comment… Seems that oil prices are up… Checks notes… according to Syz Group… this is the largest weekly jump in WTI crude oil prices since 1990...

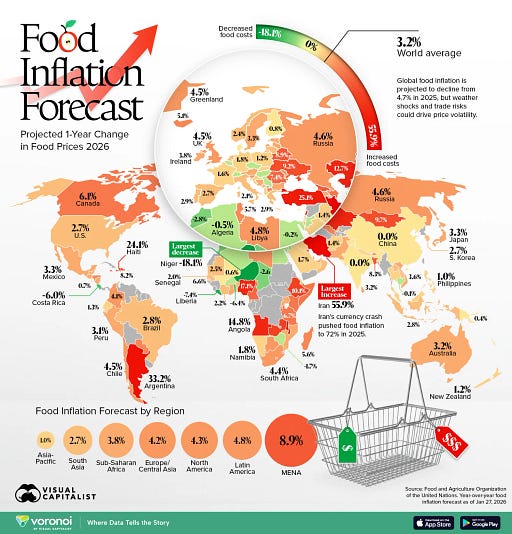

What I find more interesting, though, is that the Energy Select Sectors SPDR ETF (XLE), which tracks the largest players in the upstream and downstream spaces, barely moved in response to this. The XLE was actually DOWN 2.1% on the week. It is… however… up 30% since late December. Two things on this… First… blindly betting on energy stocks during a period like this doesn’t suit anyone. It seems like common sense that rising oil prices will help Exxon (XOM), which was down 5% for the week. But that’s just the human mind playing tricks on you… Second… remember that the purpose of a market is to sell. The XLE is up 30%… and that was something that happened in 2022 during the Ukraine War… Energy and material stocks burned higher and higher… until one day hedge funds and CTAs just dumped. That day was June 8, 2022… a huge negative momentum event. Risk-off is a huge threat in periods like this… Keep your stops tight, speculators. Chart 7: Bonner Research Talks Food Riots…I was checking my email, and it seems Dan Denning was the first to hit my inbox, talking about the possibility of Food Riots by the fall of this year. Well… I’m gonna go put my foot in the toilet and see if I can flush myself out of this one… I studied agricultural economics at Purdue as part of my academic odyssey in the 2010s, but I’ve been busy focusing on the Fed and all these other macro-things for the better part of three years at Money Printer… So, let me see if the hat still fits. The issue Bonner’s team explains is that fertilizer prices have spiked since so much of it comes from the Middle East, and we’re having problems in the Strait of Hormuz. Where is that? Ask Google… everyone else has been for the last month.

This chart from Visual Capitalist shows extreme price movements in the Middle East, especially in Egypt. It’s been a while since I wrote about grain prices - especially wheat - but the thing to understand is something called Engel’s Law. This goes… the richer a nation gets, the more money it spends on food in absolute terms, but it spends a smaller percentage of its income on it. Western nations tend to spend about 10% of their disposable income… It pops to 35% to 40% in Egypt… 40% in 50% in Nigeria… I’d say that the real issue will be the flow of wheat - a primary staple in the Middle East - and the origins of flows. China’s not sending anyone food… as they have their own issues domestically to address. The Ukraine War is still ongoing… and that breadbasket was always critical. Russia may need to step up on wheat exports… But what’s their incentive… I’m a believer that it’s not going to get that bad… But I can understand the stress… As I said yesterday, we just live in suspended animation, moving from one crisis to the next… don’t we. Denning’s piece is compelling… But let’s talk about something else… Chart 8: Everyone Everywhere Soon an Expert on Fertilizer

The U.S. is on track to produce about 94 million acres of corn this year… And, everyone, everywhere, is about to become an expert on fertilizers… Let me give you some things that might make your conversations about food prices a little different… Back in 2025, Senator Grassley wanted to open a conversation about the soaring price of inputs into agriculture… Well… maybe they should have started with the Federal Reserve, because when input and output prices are rising at the same time, the problem is likely linked to monetary expansion. But I know D.C., and I see where this is heading… We’re about to start having really stupid conversations again about agriculture with people who “grew up on a farm” but don’t know what a bunkline or heifer is… In the debate on fertilizer this will go one of two ways…

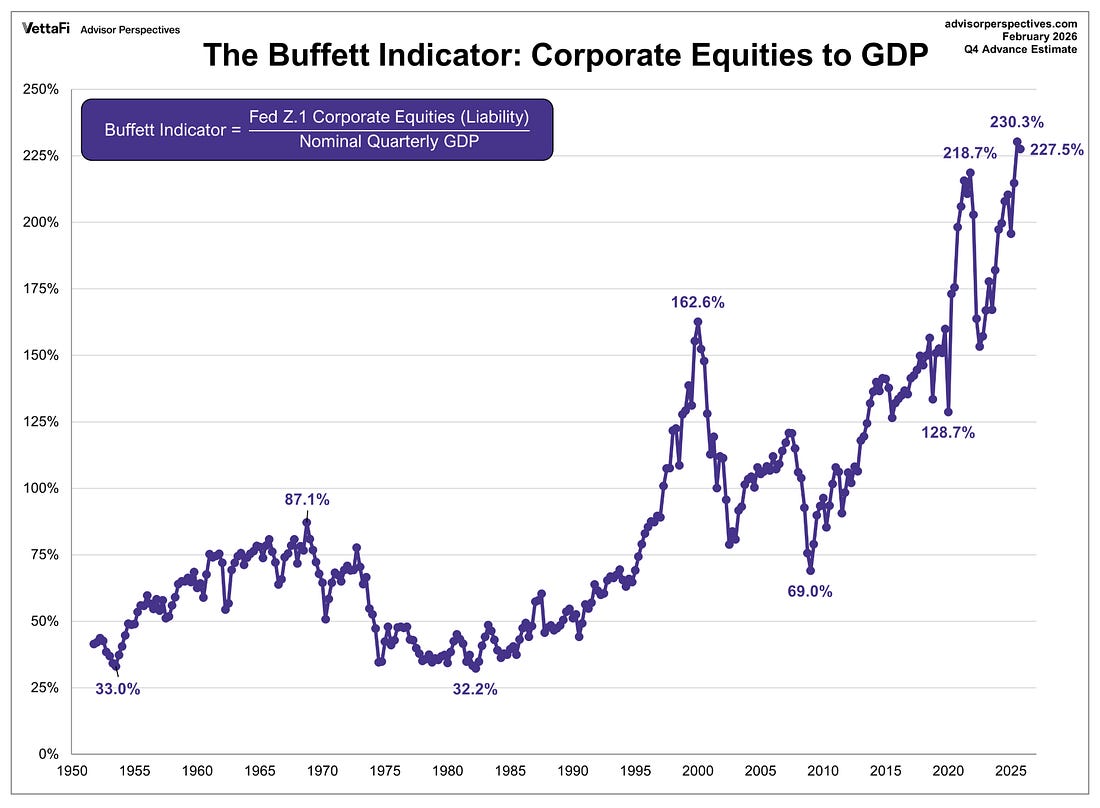

Advocates like small victories and small scalps. So they’ll focus on very small things to try to save fertilizer and the impact on food prices. Expect some advocacy shop to start barking at some point that one of the things that uses too much fertilizer that could be going to food is… “Golf Courses.” I’m serious. It’ll happen during campaign season if food prices start to rise fast. Here is some ROUGH MATH. Seriously… back of the envelope… In 2021, golf courses used about 110,000 tons of fertilizer… That’s enough (with the right seed, water, and weather conditions) to maybe, theoretically, produce about 90 million bushels of corn. Let’s say that feeds 11 million people for a year. Sounds like a lot… But you know what we already do with 35% of our corn today… And I’m talking about 5.5 BILLION BUSHELS OF CORN A YEAR? It’s turned into ethanol. And that’s where the reformers will start screaming… and get nowhere. Two out of every five bushels of corn grown in America ends up in ethanol plants… Assume 2,000 calories per day… per year. That amount of corn could theoretically feed the American population for two years. But most Americans don’t eat corn. In fact, the amount we use for food, seed, and industrial purposes is about 10% to 11% of our supply. It’s ultimately used as animal feed (even after conversion to ethanol). And ethanol replaces tens of millions of gallons of gasoline each day… Now, don’t spend your day doing this math… and don’t debate the policy too much, or you’ll hit your head on the desk, and they’ll find you on Monday. It’s all back of the envelope, and it’s precise. My point is that we produce enough food to reduce stress… but there are tradeoffs. Policy debates should center on incentives… supply chains… and moving some of our food past warlords. But there’s too much money and power in screaming on television. Chart 9: Is the Buffett Indicator Just a Liquidity Indicator?I showed Howell’s Global Liquidity Index yesterday… And it seems to be producing a very similar flight path. Seems that capital excess is exceeding actual production… but that’s the same as it ever was…

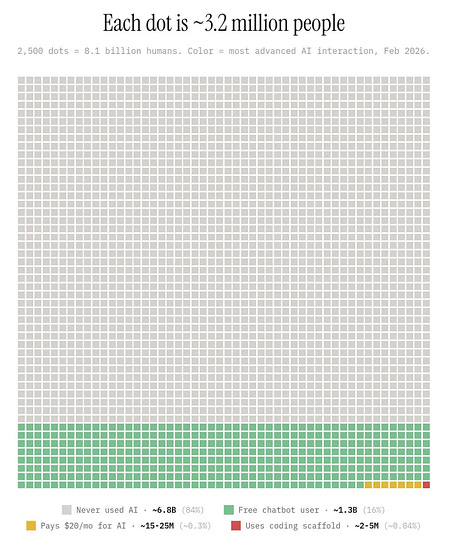

This is what a financialized economy looks like in one graph. Maybe we can hit 300% with more private credit vehicles and triple leveraged ETFs around Solana… Chart 10: Is AI A Bubble? You Be the JudgeAnd finally, I have always been a fan of Howard Marks, the head of Oaktree Capital Management. His Memos have always been must-reads. He’s been on a journey asking about whether AI is in a bubble… But someone else stole the spotlight this week in an assessment of Marks writing… highlighting that all the mental models the financier has built over time are like AI… built on the arguments he learned. This is a fascinating article by Robert Dee Asci… that accompanies this chart.

Seems like I’m in one of the red dots… wait seriously? Looks like we’re just getting started? All right… that’s all for today… It’s my 11th Anniversary… so I’m going to go hang out with my wife now. I hope you have a great day. The new Postcards arrive tomorrow. And Hedge of Tomorrow 2.0 will arrive around mid-month. Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

– blog.biocomm.ai")

Post a Comment

Post a Comment