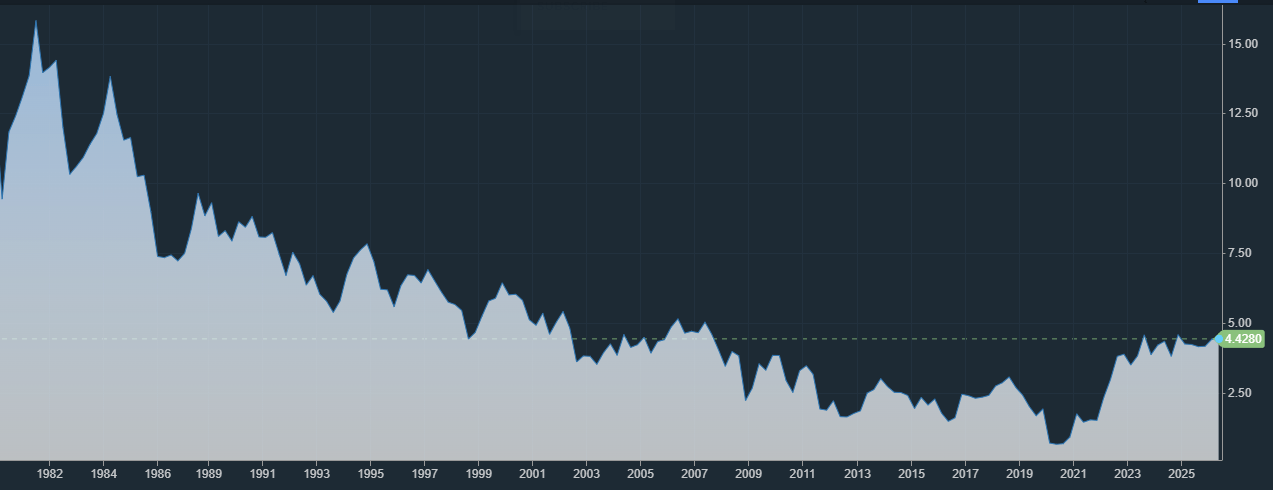

The 10-year Treasury yield hit 4.42% in March 2026 and is on track to reach a 19-year high. | | This shouldn't be happening. The Fed is trying its level best to hold rates steady. Inflation was also supposed to be under their control, but it is not. The economy is weakening. | Normally, Treasury yields are supposed to fall in this environment, but they're rising instead. | Something fundamental changed. Three forces are crushing the bond market simultaneously. Investors need to understand what the driving force behind these changes is. Being informed would make a world of difference for the investors. |

|

| | | | | | | | Elon Musk is about to take SpaceX public as part of his plan to unlock the full power of artificial intelligence. | Elon is predicting this will help unleash a $1 quadrillion new wealth wave. | That would be enough to send a check for $2.8 million to every single man, woman, and child in America. | That's how big this opportunity is. | | And I'll show you how to claim your stake… starting with just $500. |

| |

| | |

| | The Three Forces Destroying Bonds | Force 1: Inflation isn't dead. It's back, driven by geopolitical shocks the Fed can't control. Force 2: Supply is overwhelming. The government needs to sell unprecedented amounts of debt to fund massive deficits. Force 3: Foreign buyers are disappearing. Countries and pension funds that always bought Treasuries are selling instead.

| Each force alone would push yields higher. All three together? The Treasury market is repricing risk. |

|

| | Force 1: The Iran Shock Killed Disinflation | February 2026 changed everything. Military tensions involving Iran escalated. Oil spiked past $112 per barrel. | This wasn't a temporary blip. It was a geopolitical risk premium that immediately hit inflation. | Wholesale prices (PPI) surged 1.1% in one month — the largest gain since August 2023. | The breakdown: | Price Component | Monthly Change | Impact |

|---|

Food prices | +2.4% | Severe cost pressure | Energy prices | +2.3% | Immediate pass-through | Vegetables | +48.9% | Transport/fertilizer costs | Diesel fuel | +13.9% | Logistics inflation |

| This isn't monetary inflation. It's cost-push inflation from supply shocks. The Fed can't fix it by raising rates. | But the Fed can't cut rates either. Cutting into an oil shock would embed inflation expectations permanently. | Result: the Fed is stuck. Markets expected three rate cuts in 2026. The Fed now projects maybe one cut in December. |

|

| | Force 2: Too Much Supply, Not Enough Buyers | The U.S. government ran a $1.78 trillion deficit in fiscal 2025 — 5.8% of GDP. | To fund this, the Treasury Department must sell massive amounts of bonds. At the same time, the Federal Reserve is selling bonds through quantitative tightening. | More supply is hitting the market. Fewer automatic buyers. | The deficit trajectory: | Fiscal Metric | FY 2025 | FY 2026 Projected | 2036 Projection |

|---|

Annual deficit | $1.78T | $1.90T | $3.1T | Debt as % of GDP | 100% | 101% | 120% |

| The 2025 Reconciliation Act added $4.7 trillion to deficits over the next decade. Defense spending, immigration enforcement, and tax cuts all require funding. | Someone has to buy all these bonds. The market is demanding higher yields to absorb the supply. |

|

| | The Auction Warning Sign | Treasury auctions used to be routine. The government offered bonds, and investors bought them at predictable prices. | Not anymore. Auctions are showing "demand cracks." | The warning signal is called a "yield tail." It happens when the Treasury has to offer higher yields than the market price to find enough buyers. | February 2026: a 10-year Treasury auction resulted in a 1 basis point tail. The Treasury had to pay more than expected to sell the bonds. | This means primary dealers (banks required to bid) are getting saturated. They're demanding higher yields to take on more bonds. | When even mandatory buyers hesitate, something's wrong. |

|

| | Force 3: Foreign Investors Are Selling | For decades, foreign central banks and pension funds provided a floor for Treasury demand. No matter what happened in Washington, foreigners bought U.S. debt. | That assumption just broke. | The ABP case: Dutch pension fund ABP (fifth-largest in the world, $500 billion in assets) sold $10 billion in Treasuries between March and September 2025. | Total holdings dropped from $29 billion to $19 billion. They reallocated to German and Dutch government bonds instead. | The reason? "Trump's unpredictability" and concerns about U.S. fiscal stability. | Danish pension funds representing teachers and academics also sold. Even Greenland's pension fund announced withdrawals. | Total foreign selling: approximately $75 billion in recent reporting periods. | Japan's 10-year Treasuries, which used to provide negative yields, are now delivering one of the highest yields since 1999. This essentially means that the carry trade is almost dead as the spread is shrinking. | | This isn't panic selling. It's a strategic reallocation away from U.S. risk. |

|

| | Why the Dollar Is Falling Despite Higher Rates | Normally, higher U.S. interest rates attract foreign capital and strengthen the dollar. Not this time. | The dollar has fallen more than 10% against major currencies since early 2025, even as Treasury yields rose. | This correlation broke because foreigners aren't just buying fewer Treasuries. They're actively selling and moving capital elsewhere. | Research suggests this pattern is consistent with a loss of "reserve currency premium." The extra demand for dollars, because they're the global safe haven, is diminishing. | If this continues, the U.S. loses the ability to fund deficits at artificially low rates. Yields must rise to attract buyers without the reserve currency advantage. |

|

| | The Demographic Time Bomb | There's a deeper structural problem making this worse. | Baby boomers spent 40 years as "super-savers," accumulating retirement assets. This created enormous demand for bonds and kept yields low. | Now they're retiring. They're shifting from savers to consumers, drawing down retirement accounts for spending and healthcare. | The transition: | Era | Demographic Pattern | Effect on Yields |

|---|

1980-2015 | Boomers saving for retirement | Yields falling | 2025-2040 | Boomers consuming in retirement | Yields rising |

| Less global savings means less capital available to buy government debt. This structural shift pushes yields higher regardless of Fed policy. |

|

| | What This Means for Investors | The "risk-free" Treasury is repricing. Yields rising means bond prices falling. | If you own long-duration bond funds, you're taking losses. A 1% rise in rates causes roughly 20% losses on 30-year bonds. | The traditional 60/40 portfolio (60% stocks, 40% bonds) assumed that bonds would rally when stocks fell. That correlation is breaking. | In 2026, both can fall together if the problem is supply-side inflation and fiscal instability rather than demand weakness. | Current environment suggests: | Avoid long-duration bonds unless betting on the Fed being forced to cut due to recession. Short-term Treasuries (1-3 years) offer 4%+ yields with minimal rate risk. Diversification beyond stocks and bonds becomes critical: commodities, real assets, international exposure.

|

|

| | The Bottom Line | Three forces are converging to push Treasury yields higher: geopolitical inflation shocks, unprecedented supply from deficits, and erosion of foreign demand. | The Fed can't cut into an oil shock. The government can't stop borrowing. Foreign investors are reallocating away from U.S. risk. | The 10-year yield at 4.42% might not be the top. If these trends continue, 5% is possible. | The era of cheap government borrowing is over. The "exorbitant privilege" of funding massive deficits at low rates is disappearing. | For investors, this means the bond market is no longer a passive allocation. Duration is a macro bet. Credit quality matters more. Diversification beyond traditional stocks and bonds is essential. | The Treasury market was the anchor of global finance. That anchor is being repriced for a world where U.S. fiscal stability is questioned, and reserve currency status is no longer guaranteed. | In the next edition, we'll break down how to choose the right bonds based on your risk profile and investment goals. |

|

| | | | | Important disclosures: This newsletter is provided for informational purposes only and does not constitute investment advice. All investments involve risk, including possible loss of principal. Please consult with your financial advisor before making investment decisions. |

| |

| | |

|

|

Post a Comment

Post a Comment