Trump's Nuclear Bet Could

Trigger a Market Melt-Up Dear Reader,

We’re now 12 days into the war with Iran… and with every day the conflict drags on, the greater the risk that something “breaks.”

The International Energy Agency was concerned enough to announce an emergency oil release of 400 million barrels, the largest in history. It amounted to a third of the entire 1.2-billion-barrel reserve.

Of course, under normal circumstances, around 20 million barrels of crude oil per day pass through the Strait of Hormuz. Iran has effectively made the Strait unpassable… so the 400 million in emergency reserves will be burned through in about four weeks.

I’ve said from the beginning that the war probably won’t drag on much longer than that. President Donald Trump has said that he expected the operation to last five or six weeks, and we’re already two weeks into it.

Since this is a war of choice, Trump has the ability to walk away.

We’ll see how things develop. Wars are unpredictable, and this one could escalate to the point that walking away becomes difficult.

But for now, the most likely scenario is a ceasefire within a few weeks. With an election coming later this year, Trump won’t want to risk a prolonged energy and food crisis.

Once the smoke clears, you’re going to see one clear trend develop.

It became obvious years ago that renewable energy sources like solar and wind are too intermittent to replace baseload power. You need something that is “always on.”

Coal is too dirty to be politically feasible, and oil and gas supplies can be choked off by war. We saw it in 2022 following the Russian attack on Ukraine, and we’re seeing it again today.

The only viable solution – particularly given the massive new energy needs from AI – is nuclear energy. There’s simply no other way.

The Trump administration has acknowledged this reality, and they’re going all in — committing to a radical plan that could catapult America’s nuclear energy output to 4 times its current level.

That’s a historic level of government support & investment for the domestic nuclear industry, and it’s coming at the most pivotal moment of our generation. Make no mistake; Donald Trump’s radically transformative nuclear policy is creating one of the defining economic moments of his presidency — and he’s going to make billions for investors along the way.

I’ve created a four-part plan to profit from Trump’s “Midterm Melt-Up,” and I'm sharing it LIVE right now at this link.

Click HERE at any time after 1:00 p.m. Eastern time to view my full webinar on how Trump’s nuclear policy is triggering a tidal wave of investment in US stocks, and why the clock is already ticking on capturing some of the biggest winners of the upcoming decade.

be looking at stocks that have been newly rated as “Bullish” on my Green Zone Power Ratings system.

There are some real surprises this week.

The brick-and-mortar retail economy has been struggling for years, particularly since the pandemic.

Shopping patterns have changed, and nagging inflation combined with a broader cost of living crisis hasn’t helped.

And yet… we’re seeing some old-school retail names that suddenly look investable again.

Let’s get to it! | Trump's moves in 2025 created massive winners and losers.

Solar stocks lost $20 billion from a single announcement, while Palantir soared 140% when Trump made AI a national priority.

Now Larry Benedict – who helped his readers profit during Liberation Day's chaos – says Trump's preparing something even bigger.

He calls it "Project 2026."

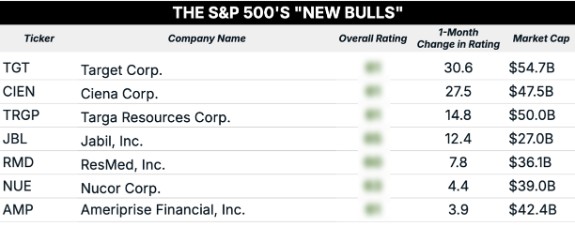

Click here to discover the ONE ticker positioned to capture the gains... and get on the right side before Trump makes his move. | S&P 500 New Bulls I ran my usual screen for S&P 500 Index companies that popped up as “Bullish” this week, and this is what I came up with:  At the very top of the list is Target (TGT), which saw a massive 30.6-point jump in its Green Zone rating over the past month.

Target has really been stuck in a rut.

The company has posted 13 consecutive quarters of flat or declining year-over-year sales. Inventory problems have weighed on margins.

Target historically relied on a higher percentage of discretionary sales than competitors like Walmart, so the consumer focus on bare necessities over the past few years has cut deep.

Store traffic continues to slide as shoppers defect to competitors, and a new CEO now faces the daunting task of restoring the brand's once-iconic “Tarzhay” appeal.

Despite these complications, the company’s Green Zone rating suggests better times might be around the corner.

The stock rates exceptionally well on its value factor. After years of underperformance, the shares are now objectively cheap. Since bottoming in late November, TGT shares are up almost 40%.

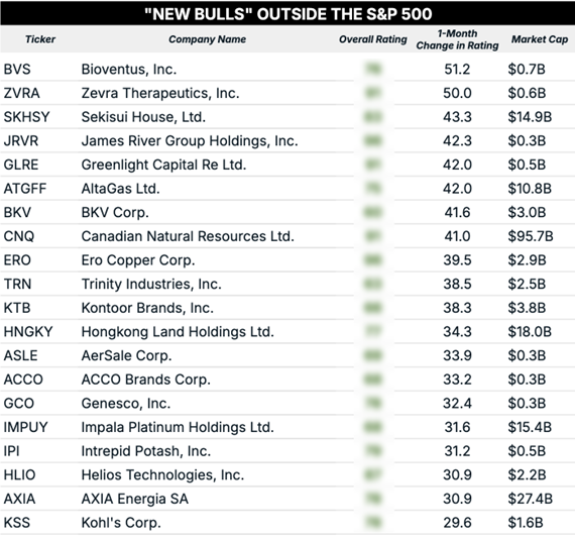

It may be a while before we start to see real revenue growth again, particularly if the fallout from the Iran war pulls us into a recession. But the market is pricing in a healthy recovery. New Bulls Outside the S&P 500 Let’s cast the net a little wider and look at the newly “Bullish” stocks outside of the S&P 500.

I ran a screen for the top 20 stocks with the largest score increases over the past month.  Continuing the theme of this year, we see a lot of energy, materials and mining stocks in the mix, including Canadian Natural Resources (CNQ), Ero Copper (ERO) and Impala Platinum (IMPUY).

Intrepid Potash (IPI) also made the list. I mentioned earlier this week that the Strait of Hormuz is a major global choke point not just for oil, but also for roughly half of the world’s urea-based fertilizer shipments.

With the Strait closed, fertilizer prices have gone through the roof.

This was one of my rationales for recommending one of Intrepid Potash’s competitors in the last issue of Green Zone Fortunes. We’re up 32% in less than two weeks.

Returning to retail, Kohl’s Corp (KSS) just barely made the list. The affordable clothing retailer saw its Green Zone rating jump nearly 30 points over the past month.

Kohl’s is an interesting case study in a traditional brick-and-mortar store chain making itself relevant in the era of near-instant delivery.

Starting in 2019, the company partnered with Amazon (AMZN) to serve as a return center for Amazon merchandise, believing this would increase foot traffic at its stores. The results have been somewhat mixed, but the partnership showed a willingness to innovate.

Kohl’s isn’t a growth dynamo and may never be one again. Its growth factor rating is a pitiful 4 out of 100. But the stock is extraordinarily cheap, with a perfect 100 on its value factor rating.

You might want to be careful entering a position in Kohl’s, as the shares have been trending lower since early December 2025. Be patient and wait for the stock to establish an uptrend before buying shares.

Given just how cheap the shares are, they could really fly once they start trending higher. Kohl’s is a heavily shorted stock, and it could be a good candidate for a short squeeze under the right circumstances.

To good profits,

Adam O'Dell

Editor, What My System Says Today

|

Post a Comment

Post a Comment