Hello, Thanks for signing up for MarketBeat Daily Ratings—we’re excited to have you on board. Every weekday, you’ll get a curated summary of new “Buy” and “Sell” ratings from Wall Street’s top-rated analysts, the latest stock news, and bonus investing content—all delivered straight to your inbox. You’re just two quick steps away from completing your sign-up: 1. Make sure our emails go to your inbox Gmail users:

Mobile: Tap the three dots (…) in the top right and select Move to Inbox or Move to Primary

Desktop: Click the folder icon at the top and select Move to Inbox or Primary Apple Mail users:

Tap our email address at the top (next to From: on mobile), then select Add to VIP Other providers:

Reply to this message and add newsletters@analystratings.net to your contacts 2. Confirm your subscription Click this link to confirm your subscription. This verifies your account and ensures you receive your newsletters without interruption instead of getting stuck in your spam filter. Confirm your subscription here. After you confirm, feel free to download our popular free report, "7 Stocks to Buy and Hold Forever" with this link. Thanks again for subscribing—we look forward to being part of your investing journey.

Matthew Paulson

Founder and CEO, MarketBeat. P.S. If you didn’t mean to subscribe, no problem—you can unsubscribe here.

Exclusive News from MarketBeat.com 3 Under-the-Radar Earnings Surprises Could Signal a New TrendSubmitted by Dan Schmidt. Publication Date: 2/17/2026.

Key Points - Earnings season is starting to wrap up as more than 75% of S&P 500 companies have reported their latest results.

- Earnings and revenue beats are in line with historical averages, but divergences beneath the surface are creating different winners and losers than 2025's market.

- These three stocks typically fly under the earnings radar in their respective industries, but their positive recent reports deserve a closer look.

- Special Report: [Sponsorship-Ad-6-Format3]

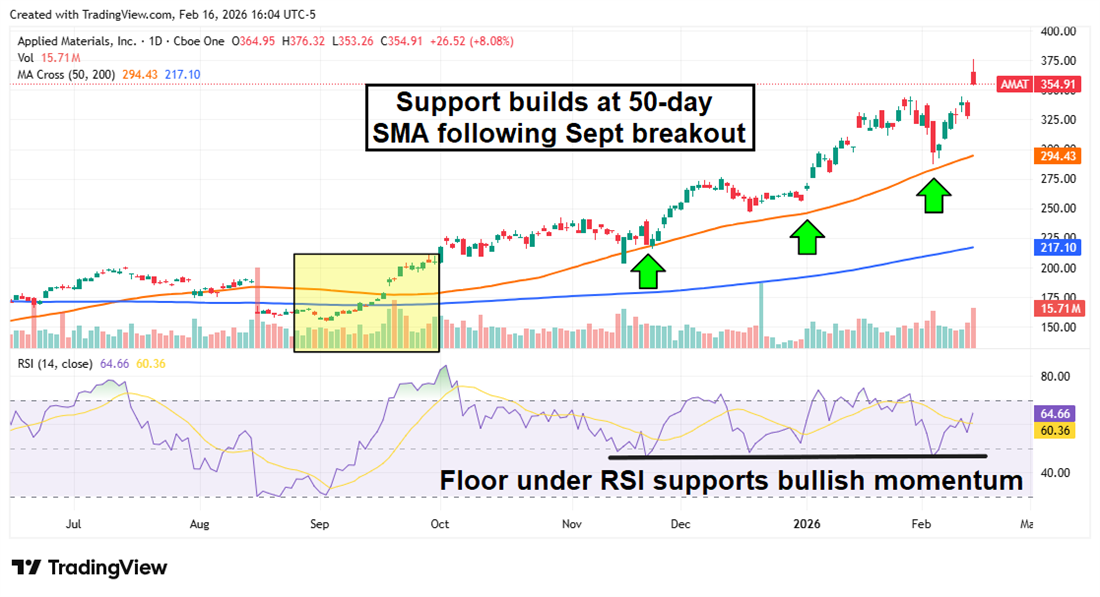

Earnings season is winding down, and more than three-quarters of the companies in the S&P 500 have reported their latest results. According to FactSet, roughly 74% of firms reporting so far have beaten analysts' EPS estimates, and 73% have beaten revenue estimates. While these overall figures are within the five- and ten-year averages, wide dispersion between winners and losers left aggregate earnings growth essentially flat for the season. Many of last year's success stories have underperformed in 2026, while some laggards have posted dramatic gains. Three companies whose earnings reports don't typically grab headlines still warrant attention for the figures in their most recent reports. Are these one-time standouts or the start of a larger trend? Applied Materials: Semiconductor Demand and Guidance Power Double-Digit Gains Applied Materials Inc. (NASDAQ: AMAT) is probably the most "on-the-radar" name here given its roughly $280 billion market cap and about $28 billion in annual sales. As a picks-and-shovels play in the semiconductor industry, Applied Materials often reports in the background while NVIDIA Corp. (NASDAQ: NVDA) or Alphabet Inc. (NASDAQ: GOOGL) dominate headlines. This most recent report, however, deserves attention: AMAT shares jumped about 12% after the release on strong guidance and robust equipment demand. The company reported its fiscal Q1 2026 results on Feb. 12 and beat analysts' expectations on both EPS and revenue, with EPS coming in roughly 7% above forecasts. The commentary that really excited investors came on the conference call, when CEO Gary Dickerson projected 20% sales growth in calendar 2026 — a pace that exceeded even the most optimistic analyst estimates. Most of Applied's revenue comes from its Semiconductor Systems division, which provides equipment for memory and logic manufacturing (flash, DRAM, transistors, etc.). Dickerson guided to Q2 revenue of about $7.65 billion and noted continued rapid growth in the Applied Global Services business. Price-target increases arrived quickly after the upbeat results, and the stock picked up two upgrades from Hold to Buy at Summit Insights and KGI Securities. The average target among the 17 analysts who raised their estimates is now $435, implying roughly 20% upside from current levels.

AMAT shares have been in an uptrend since September, when price crossed both the 50-day and 200-day simple moving averages (SMAs). The 50-day SMA has acted as reliable support on pullbacks. The Relative Strength Index (RSI) remains below the overbought threshold of 70 despite the earnings-driven pop, suggesting this rally could have staying power. Advance Auto Parts: Turnaround Efforts Starting to Show Results Advance Auto Parts Inc. (NYSE: AAP) may finally be returning to investability after losing more than 50% over the last five years. The past 12 months were particularly turbulent for the company (and the automotive sector broadly): it reported a steep loss in Q4 2024 and then faced tariff headwinds following the administration transition. CEO Shane O'Kelly has focused intensely on cutting costs and getting "back to basics," and those efforts are beginning to show results. Advance Auto Parts' Q4 2025 results beat expectations. Revenue modestly topped analyst projections ($1.97 billion vs. $1.95 billion expected), and EPS of $0.86 was more than double the consensus. Same-store sales grew about 1% for the year, and management closed 17 underperforming locations. Management's 2026 guidance also helped the stock: it forecasts 1–2% comps (comparable-store sales), roughly 45% gross margins, EPS between $2.40 and $3.10, and roughly $100 million in free cash flow generation.

Some profit-taking followed the release, since the stock had already climbed nearly 50% year-to-date. Still, the technical picture remains constructive: the share price has cleared both the 50-day and 200-day SMAs, and the Moving Average Convergence Divergence (MACD) shows a bullish crossover with the MACD line rising above the signal line and histogram during the breakout. Rivian: Narrowing Losses Point to 2026 Catalysts Friday the 13th was anything but scary for Rivian Automotive Inc. (NASDAQ: RIVN). The company beat both top- and bottom-line estimates in its Q4 2025 report. Year-over-year (YOY) revenue fell about 25% due to the expiration of EV tax credits, but sales still topped expectations and the company narrowed its loss to $0.66 per share. Smaller losses were driven by roughly a $5,500 increase in average vehicle selling price, while the cost of vehicles sold declined by about $9,500 on average. The quarter marked the company's first year of positive gross profit, and the more affordable midsize R2 model is slated to begin deliveries in Q2 2026. Rivian expects to sell between 62,000 and 67,000 vehicles in 2026, with the low end implying about a 47% increase over 2025 volume.

RIVN shares rallied as much as 20% in a volatile session after the report, though the intraday gain later retraced. The stock now sits at the 50-day SMA, which previously acted as support when shares rallied late in 2025. A bullish MACD crossover adds to the positive technical picture, but a successful R2 rollout will likely be necessary to sustain the momentum into 2026.

|

Post a Comment

Post a Comment