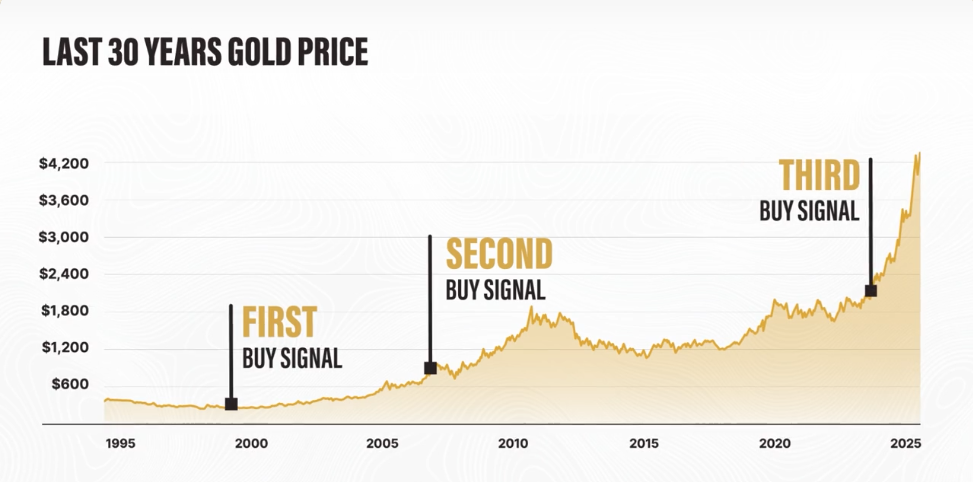

Three times over the last 30 years.

That’s how often I’ve received the signal to go “all-in” on gold.

The first time was back in the 2000s…

The dot-com mania was nearing its peak, money was flooding into any and all tech stocks, and equity valuations were trading at nosebleed levels.

I was in my mid-20’s. Just starting my first business.

And although I didn’t have much capital to spare, I scrounged together as much money as I could to load up not on tech stocks… but on gold coins.

At the time, gold was despised by Wall Street.

Goldman Sachs called it “a 19th-century asset.”

One of Merrill Lynch’s top investment analysts said that it was only for “grandmothers and conspiracy theorists.”

And two of America’s leading economists at the time called it a “barren asset.”

Yet, I chose to go in at under $300 an ounce.

My second signal came in 2008 when, amidst the chaos of the financial crisis, gold prices dropped briefly below $800 an ounce… and I once again went “all-in” on gold.

And a little over a year ago, I did it again…

I moved roughly 50% of my liquid net worth into gold and Bitcoin:

Three “all-in” decisions… Each of which seemed crazy to most at the time.

But for me… it was the most obvious move to make.

Why?

It’s all thanks to an incredible secret I learned from famed economist Kurt Richebächer - the last of the true Austrian economists.

What he taught me has been incredibly accurate at predicting the price of gold over the years.

It’s helped me make an absolute killing each of the three times I went “all-in.”

And right now, it is again predicting a shocking new price for gold in the near future.

Click here to see my full prediction for gold now.

Good Investing,

Porter Stansberry

Alibaba Stock Is Getting Hit Again, but Qwen and Cloud Growth Are Surging

Authored by Leo Miller. First Published: 3/20/2026.

Key Points

- Alibaba’s latest quarter showed modest revenue growth but a sharp drop in adjusted profit as the company continued spending heavily to defend its China commerce position.

- Cloud revenue growth accelerated, reflecting strong demand for AI-related products, even as broader concerns persist about talent retention and longer-term AI execution.

- Alibaba’s outlook hinges on whether near-term margin pressure from fast delivery and other initiatives can be balanced by sustained cloud and AI monetization.

- Special Report: Elon Musk already made me a "wealthy man"

For Chinese e-commerce giant and cloud provider Alibaba Group (NYSE: BABA), the past six months have not been kind.

Over that period, Alibaba shares have fallen more than 30%. Market share losses in Chinese e-commerce and questions surrounding the firm’s artificial intelligence (AI) leadership have been two significant headwinds for the stock.

less than two weeks to prepare? (Ad)

A $1.5 trillion valuation. That is what industry experts are projecting for the highly anticipated SpaceX IPO, expected to be announced on April 20th — potentially surpassing the combined market caps of the six largest U.S. defense contractors.

Consider what Tesla's IPO meant for early investors: a $50,000 position held for 10 years grew to $1.5 million. The SpaceX IPO is projected to be even larger.

Before April 20th, there is still a backdoor way to secure a pre-IPO stake in SpaceX. Here is how to get positioned.

Claim Your Pre-IPO PositionMost recently, BABA’s latest earnings report pushed shares down roughly 7%.

Still, Alibaba remains one of the most important companies in China and a serious player in AI through its cloud business. That combination makes it difficult to ignore, even after a rough stretch for the stock. The latest quarter sharpened the story: Alibaba is spending aggressively to defend its commerce franchise now, betting that accelerating cloud and AI demand can rebuild profitability over time.

Margin Pressure Deepens as Fast-Delivery Spending Rises

In its fiscal Q3 2026, Alibaba reported revenue of $40.73 billion, a 2% year-over-year (YOY) increase. This moderately missed estimates of $40.95 billion, which implied growth closer to 3%.

The bigger issue was earnings. Alibaba posted adjusted earnings of $1.01 per ADR, missing the analyst estimate of $1.65 and declining 67% from a year earlier. An ADR, or American depositary receipt, is a bank-issued U.S. security that represents Alibaba’s underlying shares and lets U.S. investors trade the stock in dollars on U.S. exchanges.

Management attributed the profit decline to heavier spending on quick commerce, user-experience initiatives, and technology, with improved cloud performance only partially offsetting the impact.

The company is also operating in a tougher competitive environment in China’s e-commerce market, which has raised the cost of defending its market share.

PDD (NASDAQ: PDD) has been winning the value-shopping segment, while ByteDance’s Douyin (the Chinese version of TikTok) has become a leader in discovery-based shopping, where users purchase products after seeing them in their social feeds. Meanwhile, Meituan (OTCMKTS: MPNGF) remains dominant in food delivery and related services. Alibaba is still the largest player but must invest heavily to defend that position, and those investments have weighed on profitability.

Quick commerce—delivering products in one hour or less—has become a cornerstone of its e-commerce strategy. There were some positive signals in the quarter: quick commerce revenue was up 56% YOY.

Additionally, the company added 150 million annual active customers (AAC) in 2025, defined as users who made at least one purchase during the year. However, these new users tend to be lower quality, making smaller purchases and buying less frequently.

Alibaba is betting on winning this battle over the long haul, and does not expect its quick-commerce business to be profitable until fiscal year 2029.

Cloud Growth Accelerates as Qwen Sees Strong Developer Adoption

Alibaba’s Cloud Intelligence Group delivered one of the clearest positives in the quarter. Revenue rose 36% YOY to $6.19 billion, marking the unit’s ninth consecutive quarter of accelerating growth and its fastest pace in three years. Management pointed to AI demand as a key driver, with AI-related product revenue growing at a triple-digit rate for the tenth straight quarter. The segment also remained profitable, with an adjusted EBITA margin that was described as “relatively stable” at 9%.

The company’s foundational model, Qwen, is the most widely used open-source model on Hugging Face, with more than 1 billion downloads. Hugging Face is a platform where developers can download and tune models to build applications on top of them.

That open-source adoption matters because broader developer usage can translate into demand for inference and tooling within Alibaba’s cloud ecosystem. As more developers build on Qwen, more usage shifts to running and serving those models at scale through inference and related services.

Hugging Face also shows that Qwen is a popular base for customization, with developers creating more than 113,000 derivative models tuned from Qwen.

That is more than the next two closest competitors, Alphabet (NASDAQ: GOOGL) and Meta Platforms (NASDAQ: META), combined.

The takeaway is straightforward: Qwen has gained significant traction with developers, and that traction can support growth in Alibaba’s cloud business as more applications are deployed and used.

Alibaba has set aggressive goals for its cloud and AI push. CEO Eddie Wu has said the company is targeting more than $100 billion in combined external cloud and AI revenue within five years, underscoring how central AI monetization has become to the long-term plan.

Alibaba's Solid Balance Sheet Helps Fund Longer-Term Priorities

Notably, Alibaba’s free cash flow has been negative in many of the past several quarters. Over the last nine months, free cash flow was negative $4.2 billion; however, it returned to positive territory this quarter at $1.62 billion.

Despite the recent cash outflows, Alibaba’s balance sheet remains strong. The company reports cash and other liquid investments of $80.1 billion and debt of about $37 billion. That leaves the firm with considerable firepower to keep investing in strategic priorities.

The company did not address the recent resignation of Qwen’s head of artificial intelligence, Lin Junyang. Any further changes at the top of the AI organization will be important signals about whether the firm can maintain its strong position.

Alibaba clearly has high hopes for its long-term future. Near-term issues are weighing on its e-commerce business, but its progress in AI supports a constructive outlook. With AI monetization still in the relatively early stages and shares down materially, the investment case for BABA shares looks more attractive than it did several months ago.

More Than Just Brains: The AI Revolution's Nervous System

Written by Jeffrey Neal Johnson. Date Posted: 3/18/2026.

Key Points

- Lumentum's strategic partnership with NVIDIA validates its technology and solidifies its essential role within the growing artificial intelligence supply chain.

- Nokia is strategically pivoting to capture the AI market with end-to-end optical networking solutions designed for hyperscale data center operators.

- The fundamental shift to optical networking for AI represents a multi-year supercycle, creating a durable tailwind for foundational hardware providers.

- Special Report: Elon Musk already made me a "wealthy man"

The investment conversation around artificial intelligence (AI) has focused on sophisticated software and the graphics processing units (GPUs) that act as the brains of the operation. While those components are essential, a potentially more durable investment opportunity is emerging in the physical layer of technology. A new bottleneck has appeared — not in raw processing power, but in the networks that must connect thousands of processors so they operate as a single, cohesive supercomputer.

Generative AI and large language models require a level of inter-processor communication that is unprecedented. The massive datasets used to train these models mean network speed — the system's nervous system — is now a primary driver of overall performance.

less than two weeks to prepare? (Ad)

A $1.5 trillion valuation. That is what industry experts are projecting for the highly anticipated SpaceX IPO, expected to be announced on April 20th — potentially surpassing the combined market caps of the six largest U.S. defense contractors.

Consider what Tesla's IPO meant for early investors: a $50,000 position held for 10 years grew to $1.5 million. The SpaceX IPO is projected to be even larger.

Before April 20th, there is still a backdoor way to secure a pre-IPO stake in SpaceX. Here is how to get positioned.

Claim Your Pre-IPO PositionTraditional copper cabling, long the standard in data centers, cannot handle these bandwidth demands without introducing crippling latency. That physical limitation has sparked a multi-year upgrade cycle to high-speed optical networking. This optical supercycle creates a sustained tailwind for the companies building the indispensable plumbing of AI, offering a foundational way for investors to participate in the ecosystem's growth.

Lumentum: Supplying the Speed-of-Light Components

Lumentum Holdings Inc. (NASDAQ: LITE) has emerged as a major beneficiary of this optical upgrade — a status recently reinforced by the undisputed leader in artificial intelligence.

In early March, NVIDIA (NASDAQ: NVDA) announced a multi-billion-dollar strategic investment and purchase commitment with Lumentum to secure a long-term supply of advanced laser components and 800G transceivers, which are essential for connecting clusters of AI systems.

That deal does more than guarantee future revenue; it serves as a clear validation of Lumentum's technology and cements its role in the AI supply chain, creating a meaningful competitive moat.

The strategic validation is already translating into strong financial performance. In its most recent quarterly report, Lumentum posted a 65.5% year-over-year revenue increase and beat earnings-per-share expectations by $0.26. Its forward guidance projects revenue growth of more than 85% for the next quarter — a signal that growth is not only continuing but accelerating.

This momentum comes as the market itself expands. Lumentum is a key supplier to the global optical transceiver market, a sector forecast to more than double to nearly $22.4 billion by 2029. As data center operators rush to build AI infrastructure, demand for Lumentum's high-margin components is rising. Adding to the investment case, Lumentum was recently added to the S&P 500 index, which tends to prompt buying from large index funds and increase the stock's institutional ownership, providing a firmer base of demand.

Nokia: Building the Intelligent AI Superhighway

While Lumentum supplies critical components, Nokia Corporation (NYSE: NOK) is leveraging deep networking expertise to build the complete, intelligent systems that form the AI data superhighway. Nokia has made a deliberate strategic pivot to capture this growing market.

On March 16, Nokia announced a suite of coherent optical solutions and routing platforms specifically designed for AI-era networks. The move targets large, integrated contracts from hyperscale cloud providers and data center operators that prefer end-to-end solutions from a single, trusted vendor.

The strategy is already showing results. Nokia's Network Infrastructure division has been a growth driver, with its Optical Networks unit expanding 17% year over year in the last reported quarter. That growth indicates Nokia's push into high-speed optical systems is translating into tangible financial results and market-share gains.

Wall Street has taken notice. Major firms such as Morgan Stanley have recently named Nokia a top pick, citing rising demand for AI infrastructure. This shift in analyst sentiment suggests the market is beginning to price in this new growth vector. Nokia is using its global scale to pursue a share of the data center networking market, which is projected to grow from roughly $44 billion in 2026 to over $114 billion by 2034. As a provider of comprehensive systems, Nokia is well-positioned to benefit from this wave of capital expenditure.

Two Sides of the Same High-Growth Coin

The upgrade to optical networking is not a short-term trend but a foundational, multi-year supercycle required for AI to advance. The physical limits of older technology have created inescapable demand for optical bandwidth, presenting a clear, data-driven investment opportunity for those looking beyond the usual headlines.

Lumentum and Nokia provide two complementary ways to play this shift. Lumentum is a high-growth, component-level play — directly validated and funded by the leader in AI and tied to providing essential, high-margin parts for the buildout.

Nokia offers a systems-level, value-oriented play on the same trend, with a strategic pivot that is gaining market recognition. For investors seeking exposure to the essential hardware layer of the AI revolution, the companies building the industry's indispensable plumbing offer a compelling and foundational path to growth.

This email communication is a paid sponsorship for Porter & Company, a third-party advertiser of MarketBeat. Why did I get this email?.

If you have questions or concerns about your account, feel free to contact our U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place #620, Sioux Falls, S.D. 57103-7078. USA..

Post a Comment

Post a Comment