When Elon's SpaceX IPO officially hits — which could be just days from now — two things will happen.

Elon's 40% stake will immediately earn him around $625 billion in new wealth. Then millions of small investors will buy SpaceX's stock, hoping to strike it rich.

Unfortunately, many of them will be disappointed.

That's why I'm urging you to take advantage of this pre-IPO SpaceX play while you still can.

Sincerely,

Tim Bohen

Trash to Treasure: 3 Waste Removal Stocks to Minimize Volatility

Written by Dan Schmidt. Originally Published: 3/22/2026.

Key Points

- Waste removal stocks often perform well in volatile times due to inelastic demand for services and long-term contract agreements.

- While the industry is highly-concentraded, the incumbents have unique advantages due to regulatory compliance hurdles.

- Waste Management, Republic Services, and Clean Harbors are three waste removal companies with upside in the current market environment.

- Special Report: Elon's "Hidden" Company

If you hate taking out the trash, welcome to an exclusive club: everyone. Trash removal is always a consideration when renting or buying a new home because we all produce it and need it picked up in one form or another. Since demand for trash removal is largely inelastic, the companies that provide these services typically generate steady, if unspectacular, revenue. The waste removal industry, however, has a few other advantages that set it apart from typical consumer staples companies:

- Regulatory and environmental burden - Removing trash from a home is usually straightforward, but managing waste for businesses and governments is another matter. The waste disposal industry is highly regulated, with strict standards and high barriers to entry. Opening a new landfill is a multi-year process, so incumbents operate with oligopolistic pricing power.

- Long-term revenue streams - Waste removal companies typically operate under long-term contracts that lock in consistent revenue and tend to hold up during economic slowdowns. Businesses usually book contracts for one to three years, while larger companies and municipalities often sign five- to seven-year agreements. Contracts can be flat or variable rate and frequently include clauses for regulatory fees and fuel surcharges (increasingly important as oil prices change).

This combination of essential demand and regulatory barriers often makes the sector a solid defensive investment. Historically, waste management firms have performed relatively well during market corrections and periods of volatility. With the Iran conflict ongoing and the S&P 500 hovering near its 200-day moving average, market fluctuations are likely to continue, making waste service companies intriguing options for investors.

3 Steady Waste Removal Stocks With Upside

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Click here to get the details and I'll show you how to claim your stake…The industry's oligopolistic structure means only a handful of waste-removal companies trade publicly on U.S. exchanges, limiting investment choices. With that in mind, here are three companies that offer an attractive mix of upside potential, consistency, and dividend income, while also helping to limit exposure to fluctuating fuel costs.

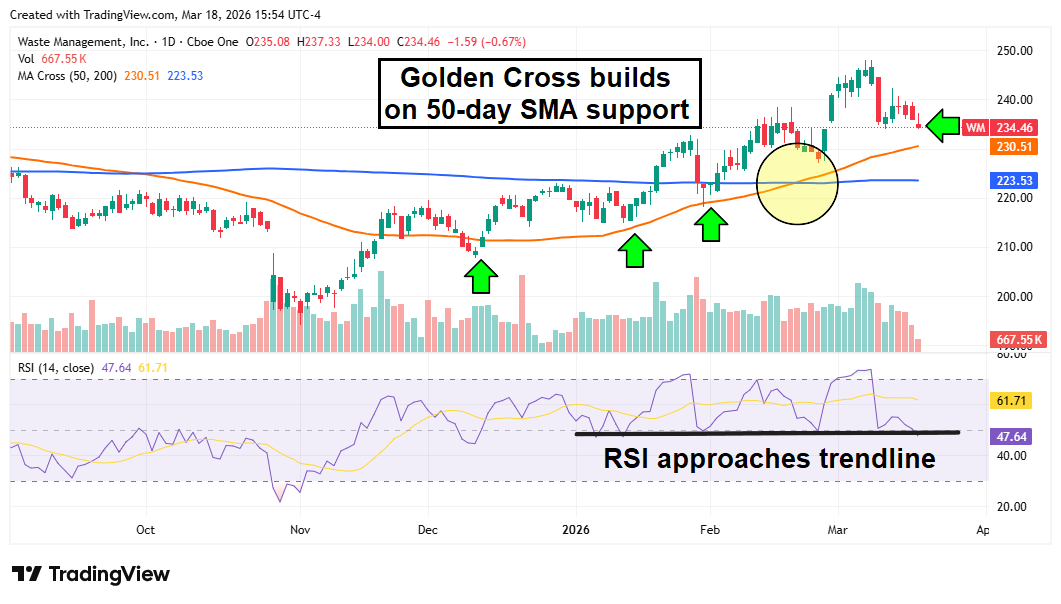

Waste Management: The Cashflow King

Waste Management Inc. (NYSE: WM) is the largest waste removal company in the U.S., both by market cap (about $94 billion) and by the number of landfills, transfer stations, and recycling facilities it operates.

It is also very shareholder-friendly, a trend likely to continue after reporting strong free cash flow of $2.94 billion in Q4 2025.

Management expects free cash flow to grow by more than 30% in 2026 and is backing that forecast with a 14.5% dividend increase and $3 billion in share buybacks.

The company is further insulated from Strait of Hormuz-related energy disruptions through surcharge mechanisms that pass diesel and compressed natural gas (CNG) price increases on to clients.

WM shares show the makings of a solid technical uptrend, with a bullish Golden Cross and healthy support at the 50-day moving average.

A move into overbought territory on the Relative Strength Index (RSI) triggered a brief pullback. The share price is once again approaching the 50-day moving average support level, which could be a favorable entry point for new buyers. The dividend now yields 1.62%, with a 56% dividend payout ratio and a 22-year streak of payment increases.

Republic Services: Low Leverage and Dividend Resilience

Republic Services Inc. (NYSE: RSG) often plays second fiddle to WM because of its smaller market cap, lower dividend yield, and fewer locations.

Still, RSG offers some advantages WM does not: an earnings beat in Q4 2025 and a cleaner balance sheet.

RSG carries less debt and has engaged in less M&A activity, which can mean slower growth but also lower financial leverage and risk.

RSG's dividend yield is lower at 1.13%, but its DPR is a healthy 36%, suggesting room for future dividend increases.

RSG uses a fuel-surcharge model similar to that of its larger competitor, helping to mitigate the impact of rising oil prices.

RSG shares have lagged WM so far in 2026, and the technicals show some tension between buyers and sellers on the daily chart. If volatility remains elevated, RSG could continue the breakout that began last November.

The stock appears to have found support at the 50-day moving average, and the RSI has returned to levels that previously marked short-term lows. A sustained move above the 200-day moving average could be the next catalyst.

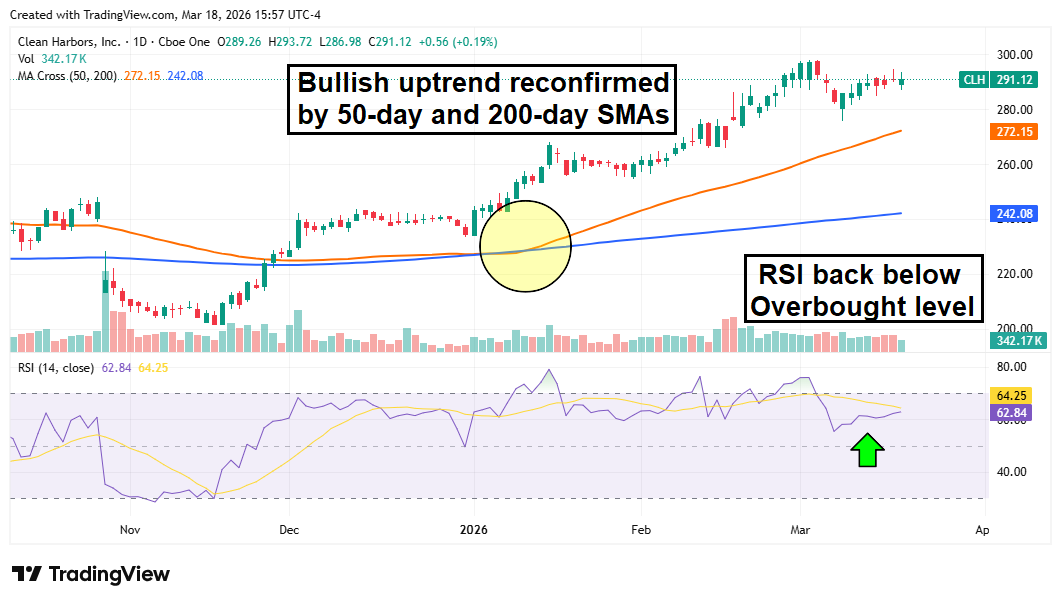

Clean Harbors: Upside From Government Contracts

Clean Harbors Inc. (NYSE: CLH) isn't a traditional collection-and-disposal company like RSG or WM, but it offers more upside potential.

More than 75% of the company's revenue comes from Environmental Services, a more cyclical segment than Collection and Disposal. Still, Clean Harbors benefits from reliable, multi-year government contracts.

The company has a multi-year agreement with the Department of Defense for polyfluoroalkyl substances (PFAS) filtration services, with an option to expand each year.

PFAS are dangerous "forever chemicals" that may contaminate water at more than 700 military bases. Clean Harbors is the only company capable of providing all three phases of PFAS filtration, remediation, and incineration, giving it a deep moat for these services and an edge when pursuing additional government work.

Investors tend to favor companies with steady government contracts, and CLH shares have gained more than 20% year to date. The stock is in a strong uptrend, trading well above both the 50-day and 200-day moving averages, and the RSI has cooled from overbought levels.

With the DoD now involved in a prolonged conflict with Iran, defense budgets may rise further beyond the administration's initial requests earlier in the year, which could translate into additional revenue for Clean Harbors' coffers.

Is Oracle the First of the AI Bubbles to Pop?

Authored by Sam Quirke. Posted: 3/28/2026.

Key Points

- Oracle shares have sunk 60% from last year’s highs, raising fresh questions about whether the AI hype cycle is already unwinding.

- However, despite the selloff, recent earnings and analyst commentary suggest the underlying story may be more resilient than the market is pricing in.

- With sentiment deeply negative and expectations close to rock bottom, the setup is starting to look more attractive than it has in months.

- Special Report: Elon's "Hidden" Company

Tech giant Oracle Corporation (NYSE: ORCL) has shifted from being one of the biggest beneficiaries of the artificial intelligence (AI) rally to one of its most notable casualties.

After surging above $345 last September as the AI boom accelerated, the stock has tumbled to just above $140 — a decline of nearly 60%.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Click here to get the details and I'll show you how to claim your stake…That rally and the subsequent fall didn't happen in a vacuum.

They were driven by aggressive investor positioning around AI infrastructure, with Oracle increasingly viewed as a core beneficiary of rising demand for cloud and enterprise AI workloads.

Expectations peaked last September, and the stock followed suit. Now the dynamic is working in reverse, raising a clear question: is Oracle the first major AI name whose bubble has burst, or has the market overcorrected and created a compelling entry opportunity?

Let's take a closer look.

The Bear Case Is Hard to Ignore

On the surface, the bear case is straightforward. Throughout last summer and into early fall, Oracle was swept up in broad AI enthusiasm. In the months that followed, tougher questions emerged about the company's strategy. To capture the opportunity, Oracle has had to invest heavily in AI infrastructure—particularly cloud and data-center capacity—which requires significant capital.

Last month's report that the company was planning to raise upwards of $50 billion to build additional capacity was met with skepticism rather than excitement, with many investors concerned that spending is running far ahead of returns.

Broader market dynamics have amplified those worries. Rising yields and a reduced appetite for risk have made investors less willing to pay for long-duration growth stories, especially those with heavy upfront investment needs.

In that context, Oracle's selloff looks less like an anomaly and more like a reflection of a shifting market environment. If the AI trade continues to unwind amid persistent investor skepticism, it wouldn't be surprising to see peers come under pressure as well.

But the Outlook Is Still Bullish

There's a credible counterpoint. Despite the share-price decline, Oracle's recent earnings reports have generally beat expectations, and several analyst updates have turned bullish.

Bank of America, for example, rated the stock a Buy this week, echoing earlier upgrades from Mizuho, Guggenheim and Citigroup. Many on Wall Street argue that the most bearish concerns should ease after the last earnings report.

Taken together, these developments suggest that while sentiment has deteriorated sharply, upside potential remains. Some recent price targets reach as high as $400, implying roughly 185% upside from current levels.

It's also notable that Oracle isn't trying to win the AI race the same way some hyperscalers are. Instead, it is positioning itself as a critical infrastructure layer—providing cloud capacity and the enterprise software backbone that many AI applications require. That distinction means Oracle can benefit from broad AI adoption regardless of which platforms or models ultimately prevail.

If that thesis holds, the current pullback may prove to be more of a sentiment reset than a full breakdown.

The Next Move Will Come Down to Confidence

Going forward, the key question for Oracle's stock isn't whether AI matters, but whether investors believe the company can convert the opportunity into sustainable growth. That makes the next earnings report in June particularly important. With much of the AI-driven upside already priced out, expectations are markedly lower than they were a few months ago.

If Oracle shares can stabilize around a support level and the company delivers a solid report, it would go a long way toward restoring confidence in its growth trajectory. Conversely, any sign that growth is faltering or that spending isn't translating into returns would reinforce the bearish narrative and keep pressure on the stock.

This email communication is a sponsored message for Timothy Sykes, a third-party advertiser of MarketBeat. Why did I get this email content?.

If you have questions or concerns about your account, feel free to contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

Copyright 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Place, Suite 620, Sioux Falls, S.D. 57103-7078. United States..

Post a Comment

Post a Comment