Earnings Report Card:

A Narrow Rally Fuels Earnings Growth Dear Reader,

We are on the cusp of the next quarterly earnings season, and early estimates look promising.

Despite the Iran war and high inflation creating headwinds in the market, analysts are now more optimistic about earnings for first-quarter 2026 than they were just three months ago.

Analysts have increased earnings estimates for S&P 500 Index companies by 0.4% since December 31, 2025.

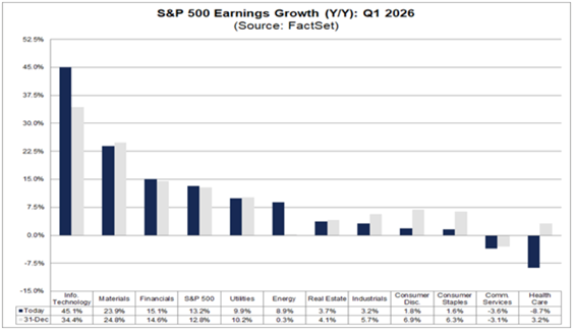

However, that optimism is constrained…  A large share of the S&P 500's earnings growth is coming from just two sectors: information technology and energy.

Both have the largest expected increase in dollar-level earnings of the 11 sectors in the benchmark.

On a year-over-year (YOY) basis, the S&P 500 is expected to report earnings growth of 13.2%. If that holds, it would mark the index’s sixth straight quarter of double-digit earnings growth.

Now, before I jump into “bullish” and “bearish” earnings calls for next week, I want to revisit a company I singled out last week… PVH Picks Up Earnings Win Last week, I focused on PVH Corp. (PVH), which popped up as a potential “bullish” earnings stock.

In fact, here’s what I wrote in last week’s earnings report: PVH has a strong history of surpassing earnings and revenue estimates — beating both in each of the last five quarters.

The trend shows that over the last three years, its best sales and earnings performance happens in the fourth quarter… most likely thanks to holiday season shopping.

I expect PVH to come in right in line with, or slightly above, analysts’ estimates for this quarter.

The owner of popular clothing brands Calvin Klein and Tommy Hilfiger did just that.

PVH reported earnings per share (EPS) of $3.82 on revenue of $2.5 billion for fourth-quarter 2025.

That constituted a 16.8% YOY increase in earnings, exceeding analysts’ expectations of $3.31 per share.

Its revenue also exceeded the $2.43 billion estimate.

As a result of the earnings beat, PVH shares rose more than 9% in trading after the announcement.

I anticipate its “bearish” rating on Adam’s Green Zone Power Ratings system will improve over the next few weeks following its earnings beat and subsequent stock price hike.

Now, let’s look at potentially “bearish” earnings for next week… | Many are calling him The Next Elon Musk…

His first company made investors 6,566% before the age of 25…

Now, he’s building one of the most-anticipated companies in the world… with $26 billion in government contracts already in place.

And one rare 4-letter ticker gives you early access — before the IPO.

Click here now to watch the briefing. | “Bearish” Earnings to Watch For our “bearish” earnings screen, we’re only looking for two things: - 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter's EPS is less than the previous quarter's.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a quarter-over-quarter decline in earnings.

I expanded this screen to include companies not listed on the S&P 500.

Here are four companies that passed this screen:  The big surprise here is Delta Air Lines Inc. (DAL).

Despite recent issues at airport checkpoints due to a Homeland Security funding freeze imposed by Congress, passenger demand jumped 6.1% in February compared with 2025.

The biggest thing hanging around the neck of Delta… and other airlines for that matter… is the price of jet fuel.

According to the International Air Transport Association, jet fuel prices are up 101.8% YOY.  For the week ending February 27, the average price of a barrel of jet fuel was $99.40. By the end of the last full week of March, that cost rose to $195.19.

The trend has been a steady rise in jet fuel prices since February, which will certainly cut into Delta’s earnings.

Delta’s trend has been to beat EPS estimates in each of the last five quarters, but this quarter is unique due to higher fuel costs.

Travel is up, but airlines like Delta have to raise fares to cover the massive jump in fuel prices.

Therefore, I can see Delta coming in right at, or even slightly below, the median EPS estimate of $0.61 for the quarter.

Anything below $0.61 per share will have a negative impact on DAL’s “Bullish” rating on Adam’s Green Zone Power Ratings system.

As for “bullish” earnings, because we are at the end of the earnings season and rolling into another, our screen turned up no potential “bullish” earnings calls for next week.

However, never fear, they are coming.

That’s all for me today. I hope everyone has a great Easter weekend.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, What My System Says Today

|  April 20th, 2026 could be the very last chance you have to profit from the SpaceX IPO. While Bloomberg predicts it will be worth $1.75 trillion… As you’ll see in this video, what Elon has planned for April 20th could lead to massive gains. But only if you make this one move right now. Click here to watch this video on how to get in position. April 20th, 2026 could be the very last chance you have to profit from the SpaceX IPO. While Bloomberg predicts it will be worth $1.75 trillion… As you’ll see in this video, what Elon has planned for April 20th could lead to massive gains. But only if you make this one move right now. Click here to watch this video on how to get in position.

| |

Post a Comment

Post a Comment