You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. GameStop Crosses the Rubicon and Other Things I Think I Think...The economy breaks when the upper "income" earners

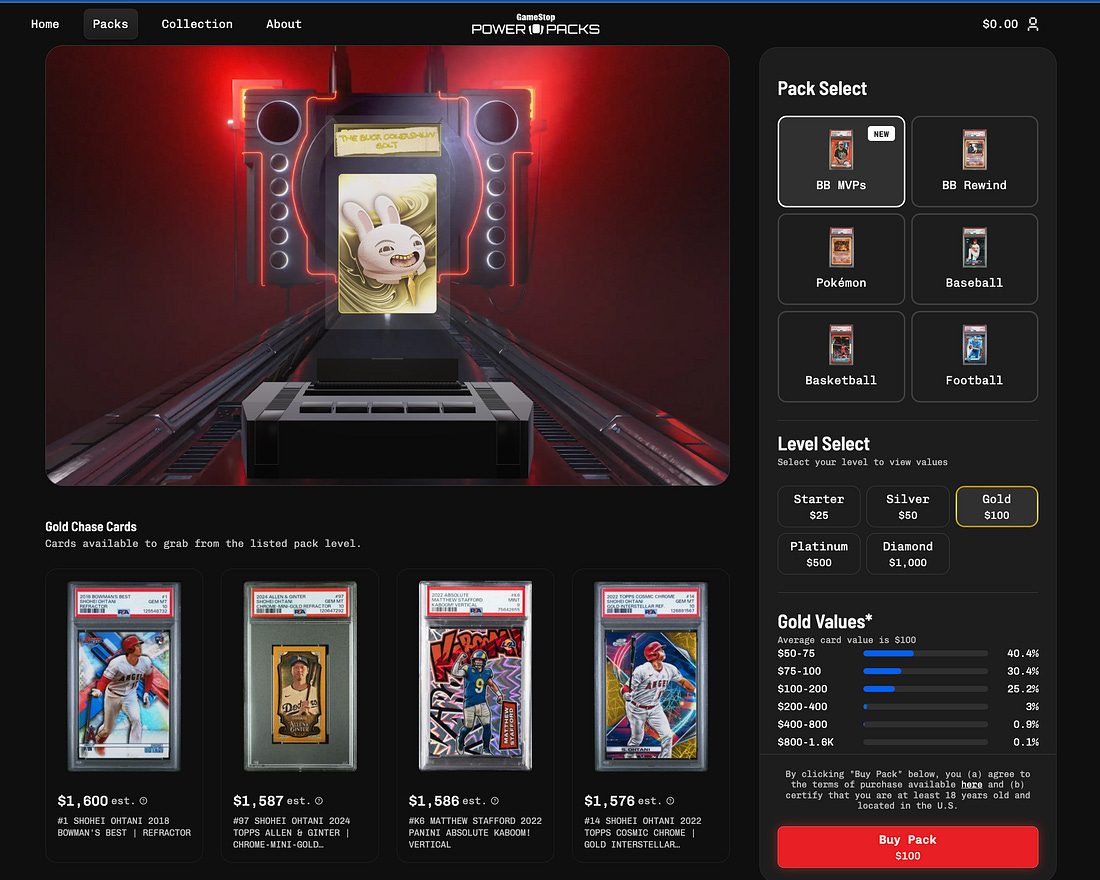

Dear Fellow Traveler: Imagine for a moment that you went to your online brokerage. It says… for $100… You can open a surprise box… and inside will be a single share of a stock. You don’t know what it is.

Would you take that bet? Well… that’s a business model in another world of “investments.” That’s what GameStop (GME) has done with its increasingly popular PowerPacks product. This is a digital screen where you can buy a “Pack” of a single baseball or Pokémon card for $100… and those are the payout odds of the card you’d receive.

For some people, this is just an extension of what people do at “wine bag” purchases at country club or private school fundraisers. You buy a “bag” containing a bottle of wine for $25. And there’s a 3% chance that you’ll get an $80 of wine… and an 80% chance you’re drinking $12 Barefoot alone… For the skeptical… This is gambling… but we just don’t call it that… Here’s the thing… It’s technically not considered gambling… because the company says they break even on sports or Pokémon cards, since it’s all based on median outcomes. I’m not convinced… but whatever. Someone reading this was doing a parlay on their phone before they got this email. But… here’s where they make their money… If you don’t like what you get, you can sell it back at a discount of “market value” for a fee… get money in your account and then do it all over again… They obviously get a spread… And if you want to send your card to you, you pay shipping… You can start with a $100 card… not like your card that is worth $125… sell it back for $105… with a buy another… get a $78 card this time… get angry at yourself - because that’s how human psychology works… sell that card… for $65… and now buy a $50 card… and try to make your money back… AND THAT’S THE POINT. That’s WHY it’s gambling… Hide behind all the terminology you want… the ability to instantly sell a card back for another card, with fees, shows it’s tapping into the same gamification and addictive qualities, but without the terminology.

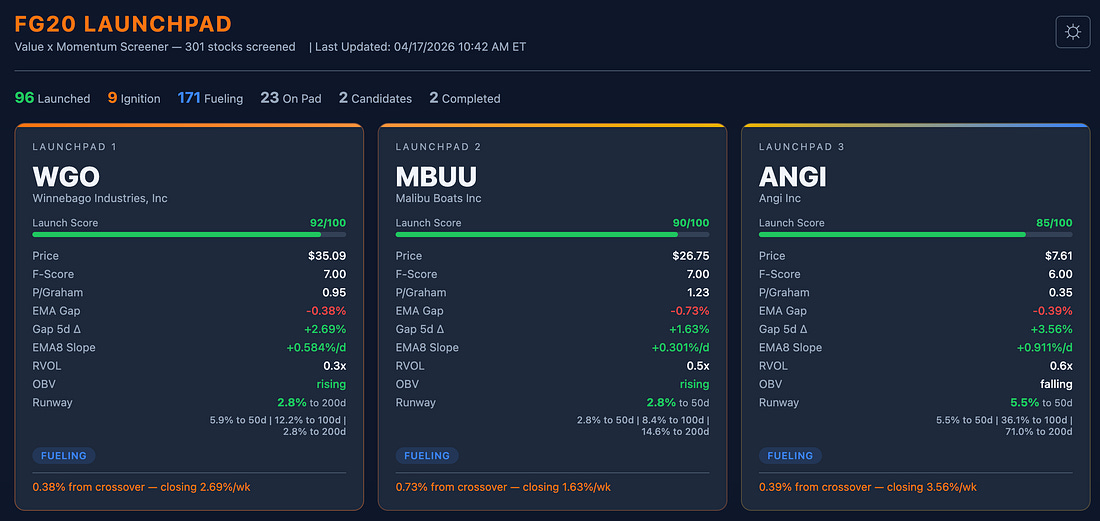

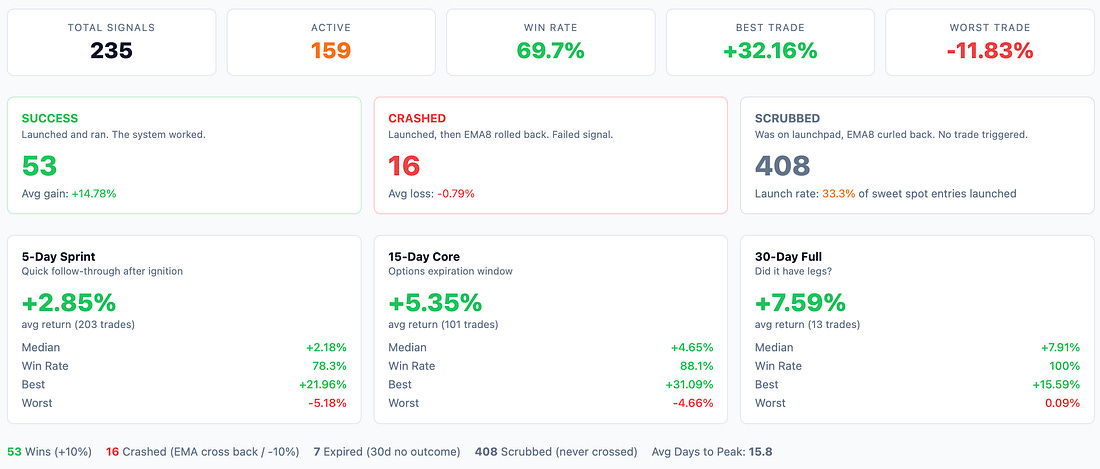

Congress and regulators are not going to get around to this one for a while… Since we live in a world where we can just change the name of monetary policy actions or private equity credit products… It’s obvious that no one cares… Pony up anywhere from $50 to $1,000 to engage in a digital draw on baseball cards that are the same thing as a gambling app mixed with a Las Vegas slot machine. Maybe you’ll get a Shohei Ohtani (0.1% odds). Or maybe you’ll get the autograph of a left-handed relief pitcher in the minor leagues. What is to stop anyone from doing this with stocks? Seriously… Bet $100 for a 1% chance that you get a share of Amazon.com worth $250… Hell… Closed-end funds behave like this sometimes… I’m sure Robinhood is working on that… No. 2: The Launchpad Looks Fantastic…We added another benefit to our MoneyPrinterPro.com platform for our readers… So, they can see the Live reading of S&P 500, Nasdaq, and Russell 2000 momentum, access our breakout and breakdown stock lists, and take a dive into the current state of momentum for nearly every stock on the S&P 500… Now, we’ve added the FG-20 Screener and Launchpad. What’s that? One of the things we’ve created is a combination of Quality-Value and Momentum, using the old Thanksgiving conversations Tim and I had about the ends of bell curves… Here’s today’s launchpad, which features breakouts on the 8-20 EMA and gives us a target for each.

So far, this has executed well… This will probably evolve into a trading service and a standalone at some point… A number of publishers would have charged a fortune for this, given me a small cut, and then used insane marketing claims… I don’t need to do that. Math speaks for itself.

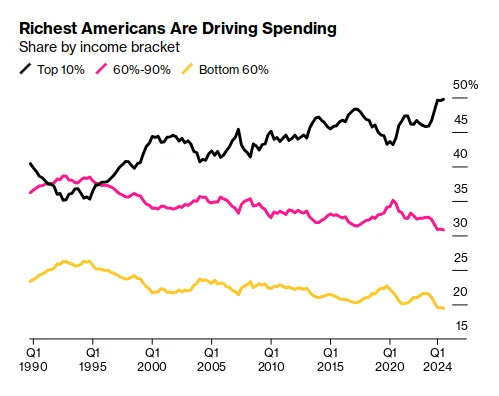

Meanwhile, Elite Members are locked in at the same annual rate and receive a momentum reading across six academic screens, along with additional liquidity and fragility indices. Eventually, I’ll do a live trading product around all of this… but for now… these are tools that set our community apart from anywhere else. No. 3: This is Where the Economy Ultimately BreaksThere was a post on Substack today showing this chart.

They argued that this is proof that “money printing” or Federal Reserve actions benefit the Top 10% at the expense of the Bottom 90%.

This won’t be a popular take… But let me explain how little people really understand about who makes what in this nation… The money printing benefits a much smaller audience. It’s through the Cantillon Effect… not through the income distribution. I promise. Because the people who live at the 10%, 9%, and 8% levels of what they earn a year are largely INCOME earners. Yes, they’re making $250,000 to $350,000 a year with a W-2 and pay taxes that scale up according to state and Federal levels. A person at the $350,000 range who is self-employed in a city like Chicago, Illinois, will pay up to 40% of their total income due to tax brackets, and on the double “taxation” of Social Security and additional fees and costs associated with various thresholds. And I haven’t even factored in the sales tax, which is just flat out nuts in terms of the impact on consumption (10.25%) These are not hedge fund manager salaries… They’re doing well… And they’re also the “marginal” part of this Top 10% level that really leaves this economy on edge, in my opinion. These are the people who are the workhorses; they’re likely in the prime earning years, and they are not benefiting largely from capital gains income. The issue is that they’re increasingly being hit by property taxes, income taxes, rising Social Security thresholds, inflation (debasement), and are susceptible to the same behavioral pressures in the equity markets, too (selling when fear is at its maximum). They’re doing fine, but… these are the people who will get squeezed from both sides, and that’s the marginal group in the top levels that I worry could really crack the economy. The issue is that if they pull back - they’re the ones no longer trying to keep up with the Joneses… We see a lot of articles about people in New York City who make $400,000 a year and are worried about the future. They reached a certain level and expected security and stability. They’re finding out what tax brackets are… and how they’re the easiest targets for tax increases - because no one really cries for anyone making $400,000. But this is a group that bureaucrats love to tax because they can tax them at every single place… Property, income, sales, travel, you name it. And these are the marginal levels that will make or break this economy in the future. This isn’t a political or economic statement… But all roads point to a world where the bureaucrats shift the bulk of the costs to balance and plug local budgets onto the people in the Top 6% to Top 20% because capital is mobile… and these people will become increasingly less mobile. Meanwhile, the ultra-wealthy who are already benefiting from capital gains can go anywhere. And Congress won’t take aim at them on the “capital gains” taxes… because Congress is them… I’d try my best to argue again that we have a spending problem… but it’s hard to satisfy the growing group of people who are looking to reach into someone else’s pocket. Again… Blood from a stone. This is why it’s so important to be heavily invested in tax-efficient places over the long term. This whole situation is only going to get dumber. No. 4: One More Time for the People in the BackBuy some gold… they’re going to print money… and engage in fiscal dominance.

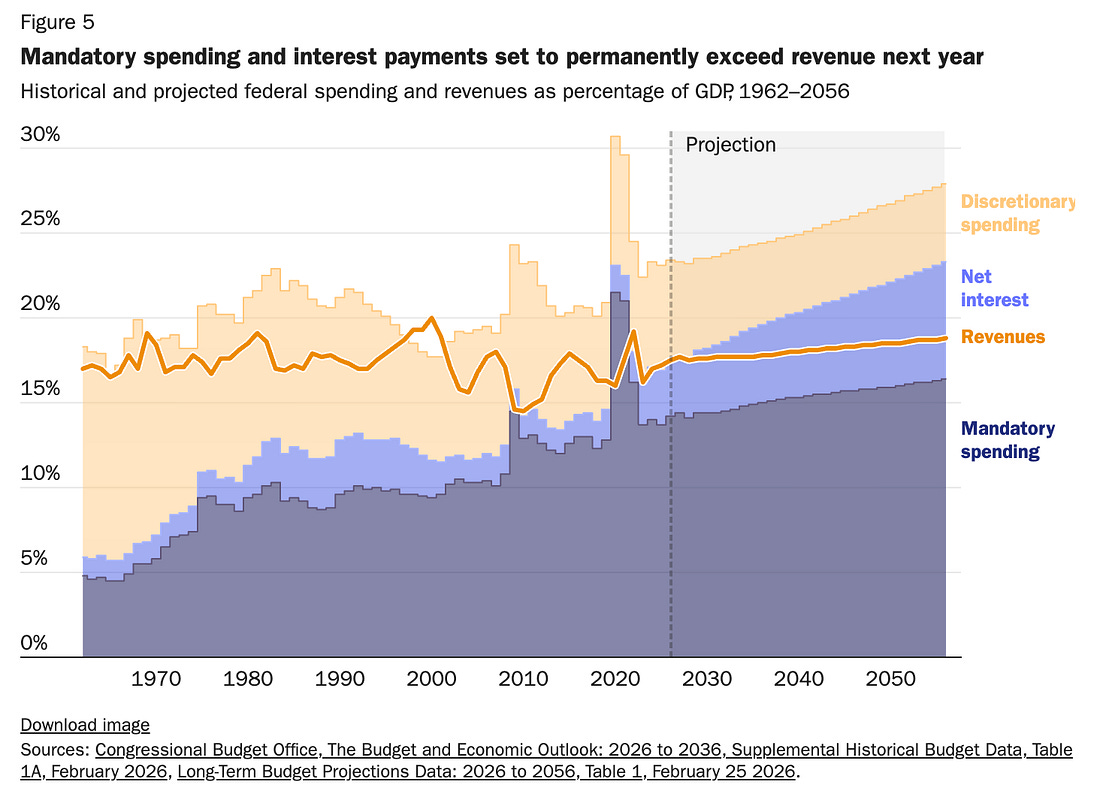

Mandatory spending and interest payments will exceed U.S. government revenue next year. We have a spending problem… This is why the liquidity cycle will face pressure… The government has to refinance all of this. So, they’re going to really go hard on fiscal dominance NOW… which could explain where we’re heading the rest of the year… Or we do face that refinancing wall… Right now… this cycle is hinting toward more dominance. They are claiming they’re reducing the $40 billion-a-month print to $25 billion. But that might go back up. I remind you… Someone said to me the other day… that the Fed isn’t doing QE. “Is it… because our own Federal Reserve doesn’t have the faith to buy our bonds and is instead doing the front end instead?” That’s a hell of a way of looking at it, isn’t it… No. 5: And Finally… It’s Good to See Gold and Silver Making Their Moves…It’s been a tough few weeks… but I said this morning that it’s important to revisit what we’re discussing in the Hedge of Tomorrow. You see, we recommended gold and silver in March 2024 because we saw the road to monetary expansion hitting a new leg… Well, here we are. The Treasury Department is involved… It’s not QE, but it leads to QE-like outcomes… But many people are suggesting that gold and silver are going down. How? Because Kevin Warsh will be the Fed Chair? Gold prices crashed in late January… and the headlines blamed Warsh. But it was systemic leverage that had built up, rampant speculation, and a huge decline fueled by passive funds (leveraged ones too) that had experienced forced activity. That led to a momentum selloff… The monetary expansion is still on tap. The “printing” is still here, but it has a different name. Unfortunately, people think that gold and silver could repeat the January events… And they have mentally anchored their minds to “all time highs” from January… with gold at $5,500 and silver above $120. Don’t do that. Focus on the longer-term trend… which would have gold and silver in current ranges if not for that speculative bout and frenzy that shook out a lot of retail investors. Understand that gold and silver have been steadily rising above key long-term moving averages. The trends are clear. Central banks will keep buying… investors will continue to hedge against the dollar… and markets will look for trusted places to put new liquidity. Gold will fit one of those buckets. As always, I return and highlight the Sprott Physical Gold and Silver Trust (CEF), a fund that has no middle man, just an anchor to a sizeable storage facility of gold and silver… I’ll be talking about it this weekend again in Postcards from the Edge of the World. If you haven’t had a chance to check out that publication, you can do so here… And Finally…I know the SpaceX IPO is fast approaching. That isn’t my lane. I’m not into space stocks, Star Trek, Star Wars, or the moon… I focus on the “edge of the world…” Next week, I want to introduce you to a friend who has a great understanding of what’s on tap. I’d rather defer to his expertise, as we just had a conversation about the IPO the other day, and he convinced me that there are three or four names in this space that are really poised to benefit… I’ll get you the details next week. Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Post a Comment

Post a Comment