Dear Reader,

Dr. Mark Skousen here.

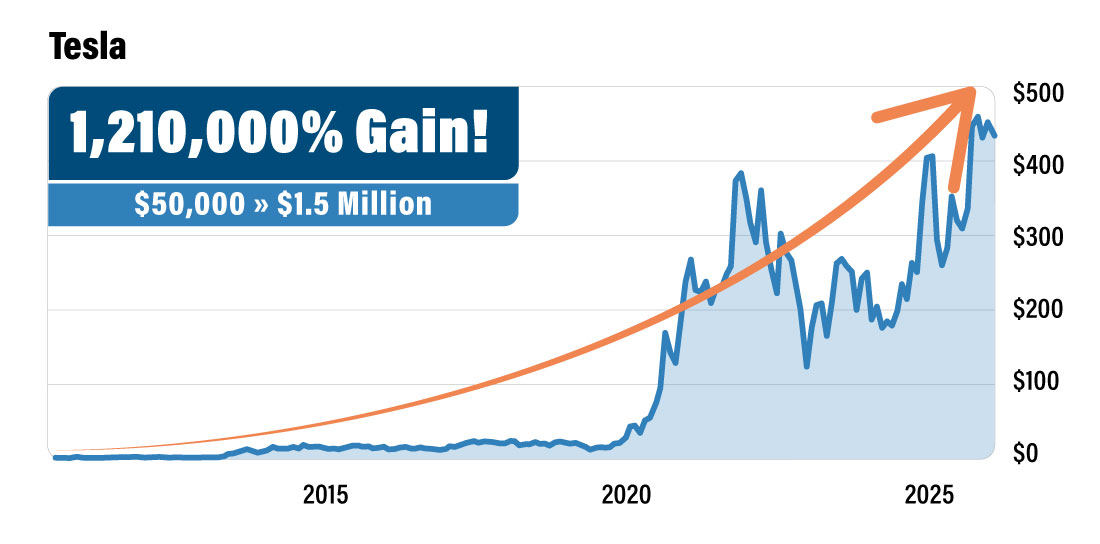

Remember Tesla's IPO?

It launched at $17 a share….

Most people laughed.

Electric cars? That quirky guy who built PayPal?

No chance.

Of course, not getting in on Tesla was a huge mistake…

Today those $17 shares are worth over $250.

Early investors who got in pre-IPO and held on could’ve turned a $50,000 investment into $1.5 million over the next decade.

|

How many people do you know who actually bought?

Almost nobody, right?!?

Well, I was one of the lucky few.

I got into a Tesla-heavy fund back when everyone thought Elon's car company would never make a dime. That early bet added nearly seven figures to my net worth over a decade.

Now I believe Elon's doing it again. This time with SpaceX.

The stakes couldn’t be higher…

And I'm betting on him again.

Industry experts are calling the SpaceX IPO a "seismic event" — a $1.5 trillion valuation that could be the biggest listing in Wall Street history.

Based on my meeting with Elon — combined with my own research — I'm convinced he'll announce the IPO on April 20th.

That's less than two weeks from today.

If you missed getting in on Tesla pre-IPO... don't make that same mistake twice.

And don’t worry. Normally, non-accredited investors are locked out of these types of Pre-IPO opportunities.

But…

I've found a backdoor that lets you grab a pre-IPO stake before Elon makes the big SpaceX IPO announcement.

And I'm sharing the ticker for free.

Just click here to see how to get positioned before the big SpaceX announcement.

Yours for peace, prosperity, and liberty, AEIOU,

Dr. Mark Skousen

Macroeconomic Strategist, The Oxford Club

P.S. Bloomberg just reported that S&P is considering a rule change, which could fast-track SpaceX into the index after the IPO. That means billions in forced buying. Get in before that happens. [Click here.]

What's in a Name? Shoe Carnival Plans Rebrand as 2026 Guidance Resets Expectations

Reported by Chris Markoch. Published: 3/27/2026.

Key Points

- Shoe Carnival stock dropped after weak 2026 guidance overshadowed mixed Q4 results, including declining EPS and flat revenue expectations.

- The company’s shift to the higher-end Shoe Station concept is driving growth, but will slow in 2026 as management refines its strategy.

- Despite near-term concerns, SCVL offers a debt-free balance sheet, rising dividend, and a low valuation near five-year lows.

- Special Report: Elon's "Hidden" Company

Shoe Carnival Inc. (NASDAQ: SCVL) stock is down nearly 10% after releasing solid—but mixed—results in its Q4 2025 earnings report.

The company met earnings expectations of 33 cents per share, but revenue slightly missed estimates and both figures were down from the prior year.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Click here to get the details and I'll show you how to claim your stake…The bigger concern was the company's guidance for fiscal 2026. Shoe Carnival forecast adjusted earnings per share (EPS) between $1.40 and $1.60, below expectations. The midpoint ($1.50) is roughly 20% lower than the $1.90 reported in fiscal 2025.

The revenue outlook was also disappointing. Management expects net sales to change between a 1% decline and a 1% increase year-over-year (YOY). They also forecast profit margin to fall to around 34% — a decline of roughly 260 basis points — driven by higher tariff-related costs and increased promotional activity.

In an earnings season that has split retail stocks into clear winners and losers, Shoe Carnival's report undercut the roughly 6.5% pop SCVL had enjoyed the week before the release.

The stock's post-earnings drop is a reminder that timing can matter as much as the headline numbers. Shoe Carnival's fundamentals weren't dire, but the report landed on a day when geopolitical tensions returned to the forefront, weighing on investor sentiment.

Shoe Carnival Branding Taps the Brakes

What's in a name? For Shoe Carnival, quite a lot.

The retailer has been rebranding many stores to the Shoe Station name. At fiscal-year end, Shoe Station locations represented 34% (144 of 426) of the company's stores, up from 10% at the start of the year.

This is more than a cosmetic rebannering; it's a strategic repositioning. In November, Shoe Carnival's board approved changing the company's name to Shoe Station Inc., pending shareholder approval in June.

Shoe Carnival historically appealed to lower-income, urban customers, relying on an in-store, "carnival-like" atmosphere. That format has become harder to serve profitably, in part because the explosive growth of e-commerce gives value-oriented shoppers many options when price is the main consideration.

The Shoe Station banner targets higher-income households that prefer an upgraded store experience and brand-focused assortments.

The transition is showing results: Shoe Station stores generated net sales of $236.7 million in fiscal 2025, accounted for about 21% of total revenue and delivered organic growth of 2.7% YOY.

Why Management Is Taking a More Measured Approach

Despite the early success of the Shoe Station concept, the company said it will slow the pace of conversions to the Shoe Station brand in 2026, citing significant variability in individual store performance.

Management's stated goal is to collect more data to:

- Identify which consumer demographics respond most favorably to the Shoe Station format

- Determine which marketing channels most effectively drive new-customer acquisition

- Refine product assortments in rebannered stores to improve in-store conversion

Debt-Free Balance Sheet Supports Long-Term Case

There are clear reasons for investor skepticism, reflected in the stock's recent weakness. Still, for patient investors there are arguments for holding the shares.

For one, the company remains debt-free — a rarity for a retailer with a market cap near $400 million. Shoe Carnival has operated without debt for 21 years.

On March 3, Shoe Carnival increased its dividend by 33%. The new 17-cent-per-share dividend will be paid on April 20 to shareholders of record on April 8. This marks the 14th consecutive year of dividend increases.

Valuation also looks attractive: the stock trades at roughly 7x forward earnings and is near five-year lows. Cheap stocks can stay cheap for good reasons, but dividend growth from a debt-free retailer can be appealing to some investors.

That said, this remains a retail trade. With short interest above 18%, many investors may prefer to wait for a clear bullish reversal before adding exposure.

Winnebago's Q2 Earnings Show It Navigating a Tough Landscape

Author: Chris Markoch. First Published: 3/26/2026.

Key Points

- Winnebago’s Q2 FY2026 earnings beat expectations, but revenue growth driven by pricing rather than volume is raising sustainability concerns.

- Macroeconomic uncertainty, including interest rates and geopolitical tensions, is weighing on consumer confidence ahead of peak RV season.

- Analysts remain bullish on WGO stock with over 20% upside, but increased institutional selling signals caution in the near term.

- Special Report: Elon's "Hidden" Company

Winnebago Industries Inc. (NYSE: WGO) is one of the leading recreational vehicle (RV) manufacturers in the country. Despite its market position, when the company reported earnings on March 25 the results—while solid—illustrated that revenue gains are being driven more by price increases than by higher volume.

Investors reacted skeptically. After digesting the Q2 2026 earnings report, the market punished WGO, with shares falling nearly 7% by the close.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Click here to get the details and I'll show you how to claim your stake…The results topped expectations on both the top and bottom lines. Revenue of $657.4 million beat the $628 million consensus and rose nearly 6% from $620.2 million in Q2 2025. Adjusted earnings per share of $0.27 matched estimates and were up 42% year‑over‑year.

These results are notable given that Q2 is a historically light quarter outside peak RV season. Here is what else current shareholders and prospective investors can take from the company's Q2 report.

Earnings Highlight Consumer Uncertainty Heading Into RV Season

Winnebago isn't a broad consumer bellwether like major automakers, but as a member of the consumer discretionary sector its results offer useful insight into consumer confidence.

As Winnebago enters peak RV season, consumers appear hesitant about large purchases. The Conference Board's Consumer Confidence Index reported last month that measures remain well below the four‑year peak reached in November 2024.

That was not the case earlier in the year, when lower gas prices, larger tax refunds and softer interest rates contributed to rising sentiment. Those factors supported bullish consumer behavior and helped lift confidence.

But as Q1 ended, consumers and investors faced more uncertainty. Geopolitical tensions involving Israel, the United States and Iran show no clear path to resolution, which can keep oil prices elevated and erode the purchasing power of tax refunds.

On top of that, the direction of interest rates remains uncertain. While opinions vary, no analyst can predict with certainty where rates will land for the remainder of 2026.

Winnebago is navigating this difficult backdrop and could be well positioned if the economy grows steadily as expected. Still, geopolitical and macroeconomic uncertainty makes short‑term forecasting challenging.

Winnebago Balances Slower Growth With Strong Financial Discipline

To get a balanced view, note that the company delivered year‑over‑year revenue and earnings growth in each of the last three quarters — evidence that it is not struggling outright.

That growth, however, pales compared with the surge in 2020–21 during the pandemic, when RV ownership spiked. RVs tend to be one‑time purchases and the market has become more saturated since then, but the continued YOY gains show demand persists.

Winnebago can't control the macroeconomy, but it is taking steps to strengthen its financial position. The company reduced net leverage even though cash on hand declined year‑over‑year.

Management is also supporting shareholder value. The board maintained its quarterly dividend of $0.35 per share (a $1.40 annualized payout), which is supported by next year's earnings projections. The company also has $180 million remaining under its prior stock buyback authorization, underscoring a focus on returning capital to shareholders.

WGO Stock Outlook Hinges on Analyst Optimism vs. Institutional Selling

Winnebago's Q2 report did little to resolve the tug‑of‑war between analyst optimism and institutional selling. Analysts have been relatively bullish: MarketBeat's one‑year price target consensus is $42.80, implying roughly 30% upside at the time of writing.

That target is down from about $60 a year ago but has been stable for the last nine months. Of 11 analysts covering the stock, the consensus rating is Hold; only four issue Buy ratings.

Meanwhile, institutional owners have been net sellers over the past 12 months. Winnebago has seen approximately $1.45 billion in outflows versus roughly $275 million in inflows — the heaviest institutional selling since Q1 2024.

While the absolute volume isn't extreme, the pace of selling has picked up in the last two quarters. It may reflect analysts getting out ahead of institutions; investors should watch analyst revisions and institutional flows in the weeks ahead.

The recent pullback appears driven more by macroeconomic factors than by company‑specific issues. Patient investors can collect the dividend while waiting for an improved economic backdrop. Prospective buyers may watch the 50‑day simple moving average — a close and hold above that level could signal a momentum shift.

This email content is a sponsored email provided by The Oxford Club, a third-party advertiser of MarketBeat. Why was I sent this email?.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here

If you have questions or concerns about your subscription, please don't hesitate to contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place, Suite 620, Sioux Falls, S.D. 57103. United States of America..

Post a Comment

Post a Comment