Dear Fellow Investor,

Mark this date: May 29th, 2026.

While the media is distracted by the latest headlines out of Iran, a 90-year-old federal law is quietly closing a trap on Wall Street's biggest bullion banks.

For 55 years, they've sold "paper gold" they didn't actually have.

But on May 29th, the legal "First Notice" deadline hits.

It's the moment of truth where paper promises must turn into physical bars—bars that the London and Shanghai vaults simply do not have.

When the "Paper Leash" snaps, gold won't just move... it will teleport.

I've identified one "Shadow Miner" sitting on a "King's Vault" of physical metal that could surge 1,000% as the paper market defaults.

See the 90-year-old law and the ticker symbol here >>>

"The Buck Stops Here,"

Dylan Jovine, CEO & Founder

Behind the Markets

P.S. This isn't just an exchange rule—it's federal law. 7 U.S.C. § 13(a)(2) carries a penalty of up to 10 years in prison for price manipulation. On May 29th, the bankers have to choose: deliver the physical gold they promised, or admit the vaults are empty. Click here to see the "Shadow Miner" ticker that wins either way. >>

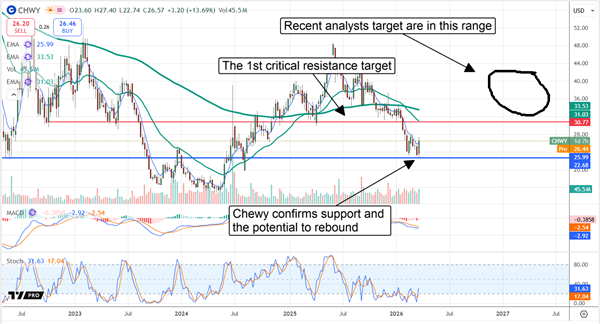

Chewy Gobbles up Market Share in 2026: Poised to Advance in Q2

Written by Thomas Hughes. Date Posted: 3/27/2026.

Key Points

- Chewy is on track to rebound in 2026 as its growth, margin, and cash flow invigorate buyers to action.

- Industry-leading growth and market share gains underpin the outlook.

- Optimistic earnings outlook triggered a buying event, confirming support at a critical level.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

Chewy (NYSE: CHWY) stock faces headwinds in 2026, as do many retailers. Still, its digital-first, asset-light model is working: Chewy is gaining share and posting industry-leading growth. The company consistently outpaces peers and the broader pet-care industry, driven by rising digital penetration globally and greater consumer emphasis on nutrition and pet healthcare. The takeaway for investors is that the stock rallied by double digits after an otherwise tepid release, signaling market support and potential for further gains this year.

Chewy Leads Market in Q4: Guides for Strength in 2026

Chewy delivered a solid quarter despite a tough year-ago comparison and elevated analyst expectations. The company reported $3.26 billion in net revenue, up 0.5% on an as-reported basis and 8.1% on an adjusted basis (the adjustment reflects an extra week). Results were driven by a 4% increase in active customers, a 2.2% increase in sales per active user, and a 4.8% increase in autoship sales.

Here's why you can thank Musk for your electric bill rising 42%... (Ad)

Your electric bill is up 42% since 2019, and utilities requested $31 billion in rate hikes last year alone. The culprit: AI data centers consuming power at a scale the grid was never designed to handle.

The last time a bottleneck like this formed, three overlooked infrastructure stocks surged 1,700%, 1,900%, and 900% before Wall Street caught on. One analyst has identified the next candidate - earlier in the cycle, smaller, and positioned at a chokepoint that even the largest players cannot build around.

See the one infrastructure stock Wall Street is about to chaseAutoship is central to Chewy's business model, representing sticky monthly revenue tied to food, medicine, and healthcare products. At roughly 84% of net revenue, autoship gives Chewy a solid foundation for predictable growth and revenue visibility heading into 2026.

Margin performance was mixed. The company widened its margins, producing a 30.4% increase in adjusted EBITDA, a 72% increase in net income, and a 47% increase in free cash flow (FCF), though some metrics fell slightly short of expectations.

Adjusted earnings per share (EPS) declined by one cent year over year and missed the consensus, but results still allowed Chewy to build cash on the balance sheet, maintain low leverage, and continue share repurchases.

Chewy's buybacks are modest and did not materially reduce the share count in fiscal 2026; however, they largely offset share-based compensation and are likely to increase over time. Management is forecasting margin improvement and an accelerated pace of earnings growth. The long-term outlook implies a high-teens to low-20s percent compound annual EPS growth rate, which translates to the stock trading at roughly 9x its 2031 EPS forecast. Although valuation remains a concern today, this multiple suggests meaningful upside potential over the coming years.

Guidance was the catalyst for CHWY's post-release price action. The company's revenue forecast was in line with expectations, and its earnings outlook was optimistic—forecasting FY2027 adjusted EPS of about $13.68, roughly a dime above MarketBeat's reported consensus.

Analysts Put Bottom in Chewy Stock: Institutions Pose Risk

The analyst reaction was mixed: early commentary highlighted earnings strength and encouraging guidance, while many analysts trimmed price targets. The net effect left Chewy's Moderate Buy rating and an 80% buy-side bias intact, although the consensus price target was lowered. That consensus still implies roughly 60% upside this year, but post-release revisions have clustered toward the lower end of the range.

Even so, many new targets still suggest upside in the 20%–50% range, supporting the view that Chewy could rebound and attracting positive revisions later in the year if momentum continues.

Institutional ownership is a key risk. Institutions own more than 90% of Chewy and were net sellers in early Q1. If selling persists into Q2 2026, CHWY will have difficulty clearing important resistance levels. As March closes, critical resistance sits near $20.75 and could be tested before quarter end. The opportunity is that institutions may return to accumulation, which would strengthen the market bottom and enable a potential rebound.

Chewy's key catalysts include execution of its high-margin strategies: Chewy Vet Care, private-label expansion, AI-driven efficiency, and its advertising business. The company enables manufacturers to advertise directly to consumers on a pay-per-click basis and leverages AI across its digital ecosystem. Private labels are expanding, improving margins and helping Chewy gain market share versus premium brands.

How Maven Turns Palantir's Biggest Risk Into Its Biggest Strength

Authored by Chris Markoch. Article Posted: 3/27/2026.

Key Points

- Palantir’s Maven program becoming a Pentagon system of record strengthens the long-term outlook for PLTR stock by turning government reliance into a durable revenue stream.

- The rapid expansion of Project Maven, now representing up to $13 billion in potential contracts, highlights growing demand for Palantir’s AI-driven military platform.

- Despite concerns about valuation, Palantir stock benefits from a widening competitive moat as deep adoption across U.S. military branches increases switching costs and recurring revenue visibility.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

Despite a drop of around 2% in the five trading days ending March 26, Palantir Technologies Inc. (NASDAQ: PLTR) stock is up more than 8.5% since closing at a low of about $128 in late February.

Although the sell-off was broad-based across the tech sector, it renewed questions about Palantir's lofty valuation.

Here's why you can thank Musk for your electric bill rising 42%... (Ad)

Your electric bill is up 42% since 2019, and utilities requested $31 billion in rate hikes last year alone. The culprit: AI data centers consuming power at a scale the grid was never designed to handle.

The last time a bottleneck like this formed, three overlooked infrastructure stocks surged 1,700%, 1,900%, and 900% before Wall Street caught on. One analyst has identified the next candidate - earlier in the cycle, smaller, and positioned at a chokepoint that even the largest players cannot build around.

See the one infrastructure stock Wall Street is about to chaseThe ongoing conflict with Iran is a key reason for the reversal. No matter what investors think about the company, any U.S. military action showcases Palantir's capabilities, particularly in the age of artificial intelligence (AI).

The product at the center of that attention is Maven. Originally launched as a Pentagon initiative to apply AI to the intelligence process, Maven has evolved into an operational platform that helps military teams sort through large volumes of data, fuse inputs from multiple sources, and turn that information into actionable workflows for tracking and targeting.

Operation Epic Fury, which began Feb. 28, offered a live demonstration of Maven's capabilities, with reports indicating the platform helped process 1,000 targets within the first 24 hours of operations.

That high-profile validation matters on its own, but it arrived alongside a more durable catalyst: on March 9, the U.S. Department of Defense designated Palantir's Maven Smart System as a program of record across the military services. That formal step typically signals institutional adoption and a steadier funding path. The designation is expected to take effect by September 2026.

A frequently leveled criticism of Palantir is that the company is too dependent on U.S. government revenue, particularly from the military. The argument has some merit: that revenue is often tied to contracts that come up for renewal. If those contracts aren't renewed, it could, in theory, pull the rug out from under millions in annual revenue and potentially billions in forecasted revenue.

The Maven announcement creates a more long-term funding structure, but for a stock trading at over 80x sales it doesn't eliminate concerns — it doesn't change the raw valuation math.

Still, it may change how investors think about that math. For a company that posted 55% U.S. government revenue growth in 2025 (to $1.855 billion), the structural underpinning of that growth just became significantly more durable.

Maven’s Expansion Was Already Underway

Current Palantir shareholders are familiar with Project Maven, but this news may pique the interest of those watching from the sidelines. Project Maven launched in 2017 as a way for the Pentagon to use AI to help analysts process massive volumes of surveillance imagery and video.

Since then, it's evolved into a broad military intelligence and targeting platform by fusing data from satellites, drones, and ground sensors to identify objects, assess threats, and support operational decisions in real time. NATO formalized its own Maven adoption in March 2025, making Palantir's platform a trans-Atlantic standard, not just an American one.

The latest announcement about Maven isn't a complete surprise; the program's (and Palantir's) footprint has expanded in the last four years through a series of escalating awards:

- The U.S. Army inked an initial $480 million, five-year Indefinitely Delivered, Indefinitely Quantity (IDIQ) contract with Palantir in May 2024.

- In May 2025, Pentagon leaders boosted the existing contract ceiling by $795 million on the expectation of a significant influx in demand from military users over the next four years.

- In 2025, the Army also awarded Palantir an enterprise agreement — potentially worth up to $10 billion over a decade — aimed at consolidating data and software systems across the service.

All told, recent reporting describes combined contract ceilings and framework capacity around Maven-related work as reaching roughly $13 billion from the initial $480 million award.

The Details Matter, but the Bull Case Remains

Critics are right to point out one important caveat about future revenue from the Maven program: Palantir isn't guaranteed to receive the full $13 billion.

That amount is IDIQ — the government doesn't have to spend it, but it has pre-authorization to do so. If the Pentagon approves the spending, there is strong incentive to deploy it.

Nevertheless, revenue tied to Maven has an annuity-like impact on Palantir's top line (and, potentially, its bottom line). The year-to-year amounts may still be lumpy, but the program adds a clearer long-term revenue pathway.

A Wide Moat to Counter a Lofty Valuation

The most significant takeaway for investors is that the Maven designation widens the company's already large moat.

For example, the Maven deal with the U.S. Army alone consolidates 75 separate contracts into a single agreement. If the cost of switching was already high, it has become enormous.

The program has also grown from roughly 5,000 to 20,000 active users. Government contracts are often renewed and expanded based on adoption; with 20,000 daily users, Palantir's own user base makes the case for adoption more convincingly than the company can alone. That kind of embedded, daily reliance transforms a vendor relationship into critical infrastructure — the sort of capability that is much harder to cut from budgets.

This email is a sponsored message provided by Behind the Markets, a third-party advertiser of MarketBeat. Why did I get this email content?.

If you need help with your account, please email MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Place, Suite 620, Sioux Falls, South Dakota 57103-7078. USA..

Post a Comment

Post a Comment