You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here.

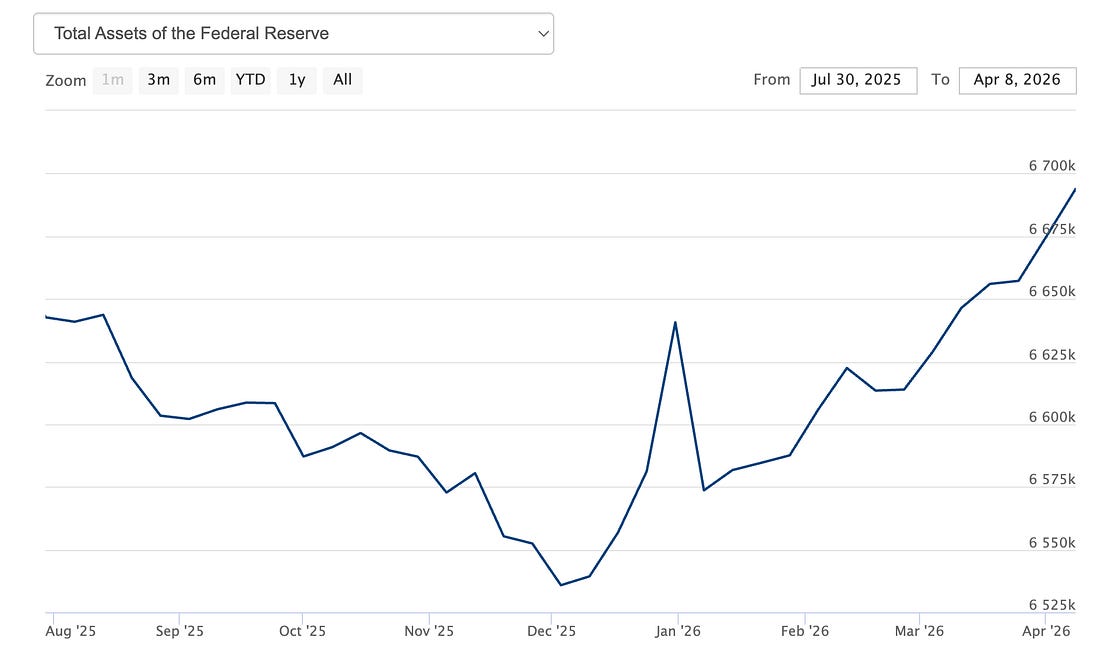

Dear Fellow Traveler, A few weeks ago, I wrote an article covering the “liquidity chatter” out of economists like Jeff Snider, Michael Howell, Brent Johnson, Zoltan Pozsar, and Lyn Alden… As we know, the Federal Reserve brought quantitative tightening (QT) to a halt at the end of 2025. That arrived around the time we saw stress in repo markets and questions about Japan’s ongoing battle against rising inflation and higher rates… In less than a year, the Fed reversed course and resumed Treasury bill purchases at a pace of roughly $40 billion a month, which shows up as reserves in the banking system. They just refused to call it “Quantitative Easing.” Lyn Alden has called it “The Gradual Print…” Jerome Powell has called it “front-loading” to make sure there were enough reserves to get through tax season. But is that front-loading ending? Roberto Perli, the New York Fed official who manages the central bank’s multi-trillion-dollar securities portfolio, said last month that the pace would be “significantly reduced” starting mid-April… He said they would taper “somewhat gradually” into May. Since December, the Fed has purchased roughly $217 billion in T-bills, based on balance sheet data. Roughly a quarter-trillion dollars added back into the system over four months, during a period when the economy was supposedly strong enough to handle tighter conditions. This equity market has held up… overcoming repo worries, Japan’s inflationary problems, and finding key support levels despite a massive oil shock. Can you hear me in the back? They’re printing money… and that matters… Alden’s used “Gradual Print” terminology. It wasn’t blatant “monetary expansion…” It was “supportive…” and it has helped support the U.S. equity market. Here’s the thing… the question isn’t whether the Fed keeps buying. They’ll continue buying… because all roads point to more monetary expansion. It’s how much they taper and how fast they get to a “steady state.” And that’s where the estimates get interesting. What the $40 Billion Actually DoesThe Fed isn’t buying stocks. It isn’t wiring money to Fidelity… It doesn’t need to do that… That $40 billion works through a chain of effects that connects the Fed’s balance sheet to every asset price in the country. Recall how the rewiring happened in 2008… When the Fed buys T-bills, it credits bank accounts at the central bank with reserves. Those reserves function as cash within the banking system. Banks with excess reserves are less constrained in their balance sheet decisions, which supports lending activity and the smooth functioning of repo markets that broker-dealers use to finance their inventory of stocks and bonds. That’s the plumbing layer. Liquidity (capital and credit) stays loose enough that nothing seizes up. But here’s the thing I really need you to understand… The second effect is in the Treasury market itself. When the Fed absorbs T-bill supply, there are fewer bonds for the private market to digest. That keeps short-term yields from spiking, which helps limit upward pressure on longer-term rates, which keeps equities looking relatively attractive. The old TINA (There Is No Alternative) dynamic… There is no alternative… no longer requires zero rates. It just requires rates that aren’t rising out of control. The third effect is the signal. When the Fed is actively purchasing $40 billion a month, the market reads that as the central bank being unwilling to let liquidity conditions tighten too fast. It’s not QE… by definition… because QE was a different level of manipulating duration. So nobody at the Fed calls it QE. But it functions as a floor under financial conditions. It aims to achieve the same outcomes as QE… Which is financial stability. The mandate for the Fed isn’t inflation or employment stability… That’s just what they tell people… it’s a giant sleight of hand. The reality is that we have to judge the system and policies by the outcomes… Which is… targeting Financial Stability. That’s the real mandate. And once you see the outcomes over the last 20 years… you’ll never unsee that as the mandate. The stock market increasingly trades on financial conditions and stability as much as underlying economic data. Maybe more… What Wall Street ExpectsBloomberg compiled estimates from the major banks on what the new pace looks like once the taper kicks in. Guess what? They’re not going to zero… the banks say…

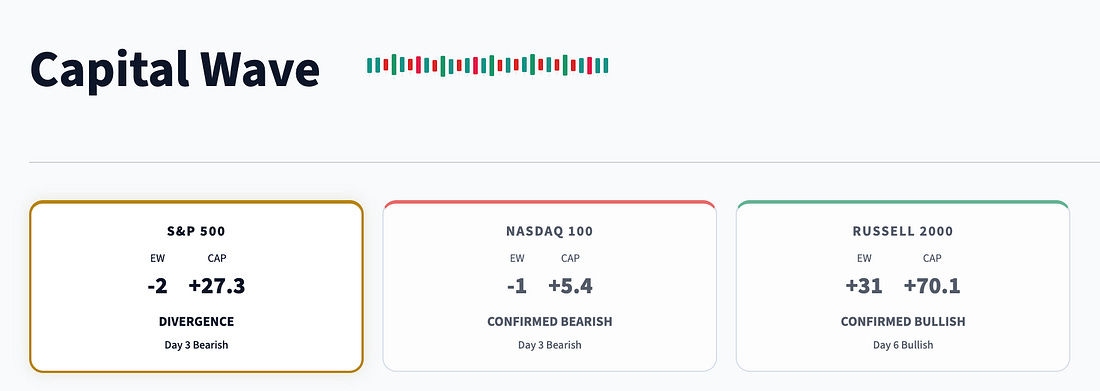

So the consensus clusters around roughly $10-$25 billion a month in ongoing Treasury purchases. That’s not zero. And that matters. That increasingly looks like a persistent liquidity drip the system has come to depend on. Which… for everyone again in the back… That’s the “Quiet BRRRRRR.” Perli himself expects reserves to stay around $3 trillion from April through September. That effectively acts as a floor, reflecting what the Fed believes the system needs to keep the lights on. If momentum does return to this market… then maybe Ed Yardeni is right… Maybe 7,200 to 7,700 is in the cards… But that’s why we have a momentum signal.

Russell momentum continues to hum… The Part Nobody Wants to Say Out LoudThe justification is technical. Banking reserves (especially at the regional level) were getting low. The overnight funding markets were showing stress. Tax season creates volatility in the Treasury General Account… But the effect, in practice, is similar to what we’ve seen before. The Fed has added liquidity, the plumbing has stayed loose, leverage has remained available, and asset prices have found support… even when the underlying fundamentals don’t justify it. This is how the moral hazard machine operates in 2026. It doesn’t need an emergency, and the market doesn’t need a crisis. It just needs a technical justification to keep buying, and the system does the rest. Banks expand credit in an environment supported by ample reserves. Broker-dealers finance their inventory. Hedge funds lever up. And retail investors continue buying the dip. And the whole thing runs on the assumption that the Fed will always be there to keep the plumbing from breaking. The uncomfortable question is what happens when they try to step back. The market has already priced in the liquidity. It’s already built on the assumption that the reserves are there. Pulling them back, even slowly, even carefully, changes the math underneath every levered position in the system. And we’ve seen this movie before. The Fed tapers… and something cracks… and the Fed comes back. Every time the central bank tries to withdraw support, it discovers that the system has grown around the liquidity like a vine around a fence. You can’t remove the fence without killing the vine. So the money printer isn’t printing in the way most people imagine. It’s not helicopter money or stimulus checks. It increasingly resembles a standing T-bill purchase program that keeps the banking system flush, the repo market calm, and the stock market supported by what appears to be a liquidity floor that nobody voted for and most people don’t know exists. It’s a form of fiscal repression… and it’s moving toward permanence. Of course… it makes the rich richer… and eats into the purchasing power elsewhere… They stopped calling it QE and started calling it “reserve management purchases.” But reserve management purchases still show up on the balance sheet.

These purchases still create reserves and suppress yields. And they still suggest to every levered participant in the financial system that they’re not going to let them fall off a cliff… The machine doesn’t need a new name to keep running. It just needs a new excuse, and there’s always a new excuse. Simply put… follow the momentum signal… and follow… The BRRRRRRRR. Even if it seems confusing. Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Post a Comment

Post a Comment