Good day,

Our research team is preparing to release our next stock idea tomorrow morning, just before 12:00 PM Eastern.

As a reminder, we send this pick first to investors who subscribe to receive The Early Bird Stock of the Day via text message. Then, it goes out the following morning to our email newsletter subscribers.

If you’d like to see the idea before it reaches the broader audience, now is the time to join. Many subscribers told us they appreciated getting early access, and our most recent pick drew a strong response.

The Early Bird Stock of the Day is a free service from The Early Bird and MarketBeat. To add yourself to the SMS distribution list and make sure you’re included in tomorrow’s release, simply click the link below:

Get The Early Bird Stock of the Day

Best regards,

The Early Bird Team

Chewy Gobbles up Market Share in 2026: Poised to Advance in Q2

Authored by Thomas Hughes. Published: 3/27/2026.

Key Points

- Chewy is on track to rebound in 2026 as its growth, margin, and cash flow invigorate buyers to action.

- Industry-leading growth and market share gains underpin the outlook.

- Optimistic earnings outlook triggered a buying event, confirming support at a critical level.

- Special Report: Elon Musk already made me a "wealthy man"

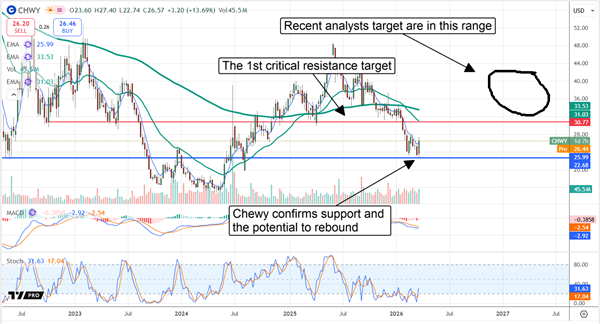

Chewy (NYSE: CHWY) stock faces headwinds in 2026, as do many retailers. Still, its digital-first, asset-light model is gaining share, as evidenced by an industry-leading growth pace. Chewy consistently outgrows peers and the broader pet-care industry thanks to rising digital penetration and a greater focus on nutrition and pet healthcare. The takeaway for investors: this stock rallied by double-digits after an otherwise tepid release, indicating market support and potential for further gains this year.

Chewy Leads Market in Q4: Guides for Strength in 2026

Chewy reported a solid quarter despite tough year-over-year comparisons and analysts' expectations. The company posted $3.26 billion in net revenue, a 0.5% increase on an as-reported basis and an 8.1% rise on an adjusted basis (the adjustment reflected an extra week). The performance was driven by a 4% increase in active customers, a 2.2% rise in sales per active customer, and a 4.8% increase in autoship sales.

The last dollar? (Ad)

After nearly five decades on Wall Street, Louis Navellier says a major currency shift is already underway - and the wealthiest Americans, including Musk, Zuckerberg, and Ellison, are quietly moving money out of dollars and into a different type of asset entirely.

It's not bitcoin or any other crypto. Navellier has identified 7 companies he believes are positioned at the center of this trend - the last time he spotted a setup like this, Nvidia climbed as high as 10,000%.

Watch Navellier's urgent briefing and get all 7 company namesAutoship sales are a critical element of Chewy's business because they represent sticky, recurring revenue tied to food, medicine and healthcare products. At roughly 84% of net revenue, autoship gives Chewy a strong foundation to accelerate growth in 2026 and provides clear visibility into future revenue.

Margin results were mixed. The company widened margins across the board, which contributed to a 30.4% increase in adjusted EBITDA, a 72% increase in net income, and a 47% increase in free cash flow (FCF). Yet some metrics fell slightly short of expectations. Adjusted earnings per share (EPS) declined by $0.01 year over year and missed the consensus, though results were strong enough to build cash on the balance sheet, retain low leverage and continue share repurchases.

Chewy's buybacks were modest in fiscal 2026 and did not materially reduce the share count, mostly offsetting share-based compensation. Management expects to increase buybacks over time as margins improve. The long-term outlook calls for a high-teens to low-20s percent compound annual EPS growth rate, which implies the stock is trading at roughly 9X its 2031 EPS forecast — a metric that suggests substantial upside potential over the next several years.

Guidance drove CHWY's post-release price action. Revenue guidance was in line with expectations, and the earnings outlook was optimistic: Chewy forecast FY2027 adjusted EPS of about $13.68, roughly $0.10 above MarketBeat's consensus.

Analysts Put Bottom in Chewy Stock: Institutions Pose Risk

The analyst reaction to the release was mixed. Early commentary highlighted earnings strength and optimistic guidance but included several price-target cuts. The net result: Chewy's Moderate Buy rating and a roughly 80% buy-side bias remain intact, though the consensus price target was trimmed. That consensus still implies about 60% upside this year, but recent revisions sit near the low end of that range.

Even so, many new targets suggest at least some upside is possible, typically in the 20%–50% range. Those projections support Chewy stock's potential to rebound, setting the stage for positive revisions later this year if the company sustains momentum.

Institutional ownership is a risk to monitor. Institutions own more than 90% of Chewy's float but were net sellers in early Q1. If that selling continues into Q2 2026, CHWY may struggle to clear key resistance levels. As March closes, critical resistance sits near $20.75 and could be tested before quarter-end. The opportunity is that institutions resume accumulation, which would strengthen the market bottom and increase the odds of a rebound.

Key catalysts for Chewy include execution of its high-margin strategies: Chewy Vet Care, private-label expansion, AI-driven efficiencies and its advertising business. Chewy enables manufacturers to advertise directly to consumers on a pay-per-click basis and leverages AI across its digital ecosystem to improve efficiency. Private labels are expanding, boosting margins and helping Chewy capture share from premium brands.

As Tech Earnings Grow, This ETF Still Hasn't Caught Up

Authored by Jessica Mitacek. Published: 3/26/2026.

Key Points

- Despite strong earnings growth and record revenue driven by AI demand, the tech sector is down nearly 5% year-to-date, creating a disconnect between company health and share prices.

- The QQQM is trading in a tight range and approaching oversold territory, offering investors an entry point before tech stock prices catch up to their financial performances.

- While mega-cap Mag 7 stocks have struggled recently, QQQM’s exposure to steady performers in consumer staples and communication services has helped offset tech-sector volatility.

- Special Report: Elon Musk already made me a "wealthy man"

Despite the tech sector’s struggles this year, the companies that make up that corner of the market continue to show strong financial health.

Fueled by intensifying demand for artificial intelligence (AI), tech companies—particularly those in the Magnificent Seven—have delivered robust earnings growth, record revenue and guidance that reflects confidence from management teams across industries, from cloud computing and cybersecurity to fintech and semiconductors.

The last dollar? (Ad)

After nearly five decades on Wall Street, Louis Navellier says a major currency shift is already underway - and the wealthiest Americans, including Musk, Zuckerberg, and Ellison, are quietly moving money out of dollars and into a different type of asset entirely.

It's not bitcoin or any other crypto. Navellier has identified 7 companies he believes are positioned at the center of this trend - the last time he spotted a setup like this, Nvidia climbed as high as 10,000%.

Watch Navellier's urgent briefing and get all 7 company namesWhile investors have been rotating out of tech since Q4 2025, analysts have continued to raise their earnings forecasts for 2026. As seen in Q1, many companies have comfortably exceeded Wall Street’s expectations.

Stock prices, however, have yet to catch up with that earnings growth. Overall, the tech sector is down nearly 5% year-to-date (YTD), making it the fourth-worst performer among the S&P 500’s 11 sectors.

On an individual basis, the picture is even worse. Microsoft (NASDAQ: MSFT), for example, has fallen more than 20% YTD—the steepest decline among the Magnificent Seven—even though all of those stocks are down in 2026.

Tech is approaching oversold territory, suggesting that once it bottoms and reverses, shares could begin to close the gap with fundamentals.

For investors, that makes exchange-traded funds (ETFs) that track the tech-heavy NASDAQ—like the Invesco NASDAQ 100 ETF (NASDAQ: QQQM)—an attractive way to position ahead of a potential rebound.

Despite Earnings Growth, QQQM Has Been Mostly Flat

Reflecting the performance of the tech giants in its portfolio, QQQM is down nearly 5% YTD. Although the fund is up more than 19% over the past year, it has traded in a tight range since early September 2025.

At the same time, many of the large-cap names in its holdings have reported blowout earnings. However, whether due to valuation concerns or fears of an AI bubble, the market has repeatedly reacted negatively.

Investors’ emotions don’t change income statements. Consider NVIDIA—the largest holding in QQQM with a current weighting of 8.80%—which, despite a YTD loss of more than 7%, is showing no signs of slowing down.

Indeed, among the fund’s top five holdings, four companies posted sizable quarterly earnings per share (EPS) growth (listed here in order of their QQQM weightings):

- NVIDIA (NASDAQ: NVDA): 95.56%

- Apple (NASDAQ: AAPL): 18.33%

- Microsoft (NASDAQ: MSFT): 59.75%

- Amazon (NASDAQ: AMZN): 13.60%

The one exception is Tesla (NASDAQ: TSLA), which reports Q1 earnings on April 28.

It’s reasonable to argue that QQQM is merely biding its time before breaking out of its range. Institutional investors may already be positioning for that scenario: although institutional selling rose in Q4 2025 to about $1.84 billion, it was still outpaced by institutional buying of $3.09 billion as buyers stepped in during the sell-off.

Outside of the Mag 7, QQQM Holds a Mix of Outperformers and Underperformers

The YTD losses among the mega-cap Magnificent Seven have overshadowed strong performances from other holdings lower in QQQM’s roster.

Micron (NASDAQ: MU), the ETF’s 11th-largest holding at a 2.53% weighting and one of the fund’s top performers this year, has continued to exceed investors’ expectations after a nearly 217% gain in 2025.

Similarly, semiconductor equipment maker Applied Materials (NASDAQ: AMAT), with a 1.50% weighting, has turned in an impressive run following a 54% gain in 2025.

That said, the ETF remains dominated by large tech names that have lagged since the start of Q4. In addition to the troubled Magnificent Seven, QQQM has been held back by underperformance from Palantir (NASDAQ: PLTR) and Broadcom (NASDAQ: AVGO), both of which have trailed the S&P 500 this year.

However, while the fund has a heavy tilt toward tech (nearly 47% of its portfolio), it also includes well-known names from sectors that have performed better in 2026.

Consumer staples, which make up more than 8% of the fund, are the fifth-best performer among S&P sectors in 2026. Walmart (NYSE: WMT) and Costco (NASDAQ: COST) account for 3.24% and 2.36% of the ETF’s portfolio, respectively, and have contributed as defensive, high-quality retailers have held up better than many growth names.

Meanwhile, communication services represent about 14.6% of QQQM’s holdings, with consumer discretionary adding roughly 13.4%. So while investors wait for tech’s rebound, the fund’s often-overlooked diversification offers built-in hedges that have helped offset the larger positions’ YTD declines.

We empower investors to make better financial decisions by delivering real-time financial information and best-in-class investment analysis.

This email content is a sponsored message sent on behalf of The Early Bird, a third-party advertiser of MarketBeat. Why did I receive this email message?.

If you need assistance with your account, feel free to contact our South Dakota based support team at contact@marketbeat.com.

If you would like to unsubscribe or change which emails you receive, you can manage your mailing preferences or unsubscribe from these emails.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Place, Suite 620, Sioux Falls, SD 57103. USA..

Post a Comment

Post a Comment