Hello, Thanks for signing up for MarketBeat Daily Ratings—we’re excited to have you on board. Every weekday, you’ll get a curated summary of new “Buy” and “Sell” ratings from Wall Street’s top-rated analysts, the latest stock news, and bonus investing content—all delivered straight to your inbox. You’re just two quick steps away from completing your sign-up: 1. Make sure our emails go to your inboxGmail users:

Mobile: Tap the three dots (…) in the top right and select Move to Inbox or Move to Primary

Desktop: Click the folder icon at the top and select Move to Inbox or Primary Apple Mail users:

Tap our email address at the top (next to From: on mobile), then select Add to VIP Other providers:

Reply to this message and add newsletters@analystratings.net to your contacts 2. Confirm your subscriptionClick this link to confirm your subscription. This verifies your account and ensures you receive your newsletters without interruption instead of getting stuck in your spam filter. Confirm your subscription here. After you confirm, feel free to download our popular free report, "7 Stocks to Buy and Hold Forever" with this link. Thanks again for subscribing—we look forward to being part of your investing journey.

Matthew Paulson

Founder and CEO, MarketBeat. P.S. If you didn’t mean to subscribe, no problem—you can unsubscribe here.

Additional Reading from MarketBeat Media

Johnson & Johnson: A 20% Gain Looks Easy After Q1 Earnings ResultsReported by Thomas Hughes. Posted: 4/14/2026.

Key Points

- Johnson & Johnson is on track to accelerate growth in 2026 and beyond.

- A healthy pipeline and balance sheet support an outlook for sustainable dividends and increases.

- Institutional and analysts support underpins the stock price uptrend, with forecasts pointing to fresh highs by mid-year.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

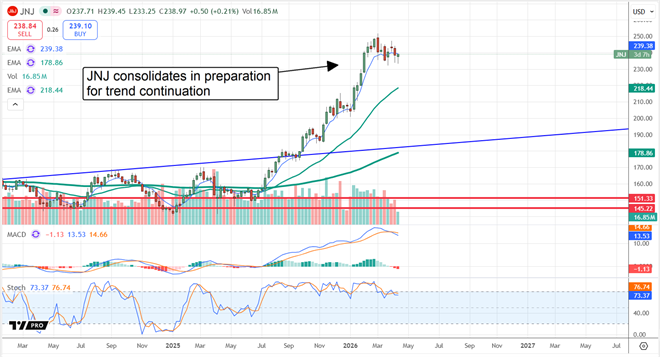

Johnson & Johnson’s (NYSE: JNJ) price action moved into a consolidation phase in early March. While the stock could continue to trade sideways or experience a further pullback, a convergence of factors makes those scenarios less likely. The combination of price action and accelerating underlying growth suggests the March pullback is a continuation signal—and a potential buying opportunity that could lead to higher prices over time. Highlights from the recent Q1 earnings release included multiple approvals and pipeline updates. Management raised guidance and reaffirmed a double-digit revenue growth pace by the end of the decade.

For a moment…

Forget about Trump’s ties to Israel.

Forget about reports of Iran’s nuclear program.

Because my research has led me to believe we’re risking World War 3 with Iran for a completely different reason. Click here to find out what it is.

Technically, JNJ’s consolidation displays the characteristics of a Bull Flag or Pennant formation. These patterns represent brief pauses within an uptrend and provide clear upside targets once confirmed. Confirmation comes from price action: the stock setting new highs and then successfully retesting support after a breakout.

As of mid-April, the key resistance level is $250. If the stock breaks above $250 and that level holds as support, a reasonable initial upside target is roughly $285 (about $35 above the breakout). Using the magnitude of the prior rally as a guide, the bull case implies an approximate 17% move from the breakout, which would place the stock in the high $280s to around $290 within a few months of confirming a new high. Johnson & Johnson Pulls Back Following a Strong Quarter and Raised GuidanceJohnson & Johnson reported a solid quarter, with revenue up 9.9% driven by organic growth, acquisitions, and favorable foreign-exchange effects. Revenue outpaced MarketBeat’s consensus by more than 190 basis points, with both core segments contributing. Innovative Medicines rose 11.2%, led by strength in oncology, while MedTech grew 7.7%. U.S. sales increased 8.3%, and international sales were stronger at 11.9%. Margins and guidance were constructive but not enough on their own to trigger a rally. Margins compressed notably due to patent expirations and increased competition for Stelara. That pressure was only slightly worse than expected and was partially offset by revenue strength, but earnings still declined. Adjusted EPS of $2.70 was down about 2.5% year-over-year, yet it beat consensus by $0.02 (roughly 75 basis points), trailing the topline strength by more than 100 basis points. Guidance was modest despite the increase. The company raised its fiscal 2026 forecast to align with consensus, implying roughly 7% earnings growth at the midpoint. The opportunity for investors is that accelerating top-line growth and new approvals could translate into margin improvement as the pipeline is commercialized. Institutional and Analyst Support for JNJ’s 2026 OutlookInstitutional activity jumped in Q1, coinciding with the move to new highs. Institutions now own nearly 70% of the stock. Given the outlook for accelerating growth, it’s more likely these holders will continue to accumulate rather than distribute shares in the near term. Analysts have also been constructive, lifting price targets and ratings heading into the report. The consensus view is a Moderate Buy, with roughly 67% of the analyst coverage recommending Buy and no Sell ratings currently logged. The consensus price target has been drifting higher. Even discounting the lowest targets, the high-end analyst estimates imply about 20% upside—consistent with the technical ~$290 target. Short interest is negligible, remaining below 1% and unlikely to be a significant headwind. Dividends are a key reason for strong sell-side interest. JNJ yields roughly 2%, and the payout has grown annually for more than 60 consecutive years. The company manages a conservative balance sheet, uses debt to fund cash and capital needs, and generates sufficient free cash flow to support both distributions and growth. The main risks remain ongoing patent expirations and their impact on revenue and margins. Offsetting that risk, the pipeline looks robust: leading candidates are expected to contribute roughly 5%–7% in annualized revenue growth over the next four to five years. Management is also prioritizing MedTech, with the Cardiovascular unit driving growth across several platforms. Surgical robotics is another growth area—the OTTAVA system is expected to seek approval later this year—and the market for surgical robotics is projected to expand substantially over the coming decade. |

Post a Comment

Post a Comment