Hello, Thanks for signing up for MarketBeat Daily Ratings—we’re excited to have you on board. Every weekday, you’ll get a curated summary of new “Buy” and “Sell” ratings from Wall Street’s top-rated analysts, the latest stock news, and bonus investing content—all delivered straight to your inbox. You’re just two quick steps away from completing your sign-up: 1. Make sure our emails go to your inbox Gmail users:

Mobile: Tap the three dots (…) in the top right and select Move to Inbox or Move to Primary

Desktop: Click the folder icon at the top and select Move to Inbox or Primary Apple Mail users:

Tap our email address at the top (next to From: on mobile), then select Add to VIP Other providers:

Reply to this message and add newsletters@analystratings.net to your contacts 2. Confirm your subscription Click this link to confirm your subscription. This verifies your account and ensures you receive your newsletters without interruption instead of getting stuck in your spam filter. Confirm your subscription here. After you confirm, feel free to download our popular free report, "7 Stocks to Buy and Hold Forever" with this link. Thanks again for subscribing—we look forward to being part of your investing journey.

Matthew Paulson

Founder and CEO, MarketBeat. P.S. If you didn’t mean to subscribe, no problem—you can unsubscribe here.

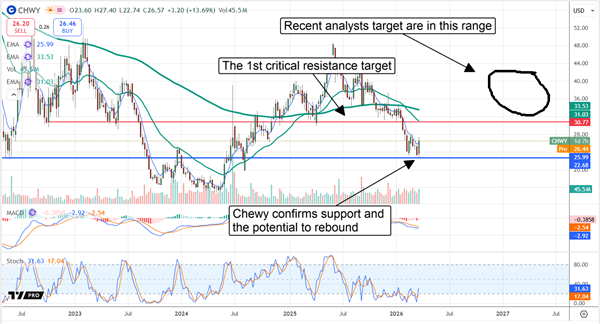

More Reading from MarketBeat.com Chewy Gobbles up Market Share in 2026: Poised to Advance in Q2Reported by Thomas Hughes. Publication Date: 3/27/2026.

Key Points - Chewy is on track to rebound in 2026 as its growth, margin, and cash flow invigorate buyers to action.

- Industry-leading growth and market share gains underpin the outlook.

- Optimistic earnings outlook triggered a buying event, confirming support at a critical level.

- Special Report: Elon Musk's $1 Quadrillion AI IPO

Chewy (NYSE: CHWY) stock faces headwinds in 2026, as do many retailers. Still, its digital-first, asset-light model is working — Chewy is gaining share and leading the industry in growth. It consistently outgrows peers and the broader pet-care market, driven by rising digital penetration globally and greater consumer focus on nutrition and pet healthcare. The takeaway for investors: the stock jumped by double-digits after an otherwise tepid release, signaling market support and potential for further gains this year. Chewy Leads Market in Q4: Guides for Strength in 2026 Chewy delivered a solid quarter despite tough year-over-year comparisons and analysts' expectations. The company reported $3.26 billion in net revenue, up 0.5% on an as-reported basis and 8.1% on an adjusted basis. The adjustment reflects an extra week in the fiscal period. Underpinning the results were a 4% increase in active customers, a 2.2% rise in sales per active user, and a 4.8% increase in autoship sales. Brand-new data centers in Silicon Valley are finished, wired, and loaded with hardware - but they can't turn on. The grid equipment needed to connect them doesn't exist yet, and the waitlist runs past 2028. With $969 billion in AI spending in motion, this infrastructure bottleneck is already pressuring timelines. One company is positioned to solve it - and a June IPO could force a repricing before most investors take notice. See the full story on the company solving the AI power crisis Autoship sales are a critical driver for the business: they represent sticky, recurring revenue tied to food, medicine, and healthcare products. At 84% of net sales, autoship gives Chewy a strong foundation to accelerate growth and provide investors with clearer revenue visibility heading into 2026. Margin news was mixed. The company widened its margins, contributing to a 30.4% increase in adjusted EBITDA, a 72% rise in net income, and a 47% increase in free cash flow (FCF). However, some metrics fell slightly short of analyst expectations. Adjusted earnings per share (EPS) declined by $0.01 year over year and missed consensus, but the company still built cash on its balance sheet, maintained low debt levels, and continued share repurchases. Chewy's buybacks aren't large and did not materially reduce the share count in fiscal 2026, but they largely offset share-based compensation and could be increased over time. Management is forecasting margin improvement and an accelerated pace of earnings growth. The long-term outlook implies a high-teens to low-20% compound annual EPS growth rate, which translates to the stock trading at roughly 9X its 2031 EPS forecast. While valuation concerns remain today, that multiple implies substantial upside potential — roughly 100% over the next few years under the company's growth assumptions. Guidance was the key driver of post-release price action. Revenue guidance met expectations and the earnings outlook was optimistic: Chewy forecasts FY2027 adjusted EPS of about $13.68, nearly a dime above MarketBeat's consensus.

Analysts Put Bottom in Chewy Stock: Institutions Pose Risk The analyst reaction was mixed: early commentary praised earnings strength and the 2026 guidance, but several firms trimmed price targets. The net result is that Chewy's Moderate Buy rating and 80% Buy-side bias remain intact, although the consensus price target was moderated. That consensus still implies roughly 60% upside this year, but many of the recent revisions sit at the lower end of the range. Even so, the new targets suggest potential upside, with most clustered in the 20%–50% range. Those estimates support Chewy's rebound potential, leaving room for positive revisions later in the year if momentum continues. Institutional ownership is a risk factor. Institutions own more than 90% of Chewy stock and were net sellers in early Q1. Continued selling into Q2 2026 could prevent CHWY from clearing key resistance; as March closes, that resistance sits near $20.75 and could be tested before quarter-end. Conversely, renewed institutional accumulation would help cement a market bottom and create a clearer path for a rebound. Chewy's catalysts center on executing its high-margin initiatives: Chewy Vet Care, private-label expansion, AI-driven efficiency, and its advertising business. The ad platform lets manufacturers advertise directly to consumers on a pay-per-click basis, while AI improves efficiency across the digital ecosystem. Private labels are a growing source of margin and help the company capture share from premium brands. |

Post a Comment

Post a Comment