Hello, Thanks for signing up for MarketBeat Daily Ratings—we’re excited to have you on board. Every weekday, you’ll get a curated summary of new “Buy” and “Sell” ratings from Wall Street’s top-rated analysts, the latest stock news, and bonus investing content—all delivered straight to your inbox. You’re just two quick steps away from completing your sign-up: 1. Make sure our emails go to your inbox Gmail users:

Mobile: Tap the three dots (…) in the top right and select Move to Inbox or Move to Primary

Desktop: Click the folder icon at the top and select Move to Inbox or Primary Apple Mail users:

Tap our email address at the top (next to From: on mobile), then select Add to VIP Other providers:

Reply to this message and add newsletters@analystratings.net to your contacts 2. Confirm your subscription Click this link to confirm your subscription. This verifies your account and ensures you receive your newsletters without interruption instead of getting stuck in your spam filter. Confirm your subscription here. After you confirm, feel free to download our popular free report, "7 Stocks to Buy and Hold Forever" with this link. Thanks again for subscribing—we look forward to being part of your investing journey.

Matthew Paulson

Founder and CEO, MarketBeat. P.S. If you didn’t mean to subscribe, no problem—you can unsubscribe here.

Just For You Trash to Treasure: 3 Waste Removal Stocks to Minimize VolatilityWritten by Dan Schmidt. First Published: 3/22/2026.

Key Points - Waste removal stocks often perform well in volatile times due to inelastic demand for services and long-term contract agreements.

- While the industry is highly-concentraded, the incumbents have unique advantages due to regulatory compliance hurdles.

- Waste Management, Republic Services, and Clean Harbors are three waste removal companies with upside in the current market environment.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

If you hate taking out the trash, welcome to an exclusive club: everyone. Trash removal is a common consideration when renting or buying a home because we all produce waste and need it collected in one form or another. Since demand for trash removal is inelastic, companies that provide these services typically generate steady, if unspectacular, revenue. The waste removal industry also has a few advantages that set it apart from typical consumer staples firms: - Regulatory and environmental burden — Removing trash from households is usually simple, but handling waste for businesses and governments is another matter. The industry is highly regulated, with strict standards and high barriers to entry. Opening a new landfill can take years, so incumbents operate in an oligopoly with considerable pricing power.

- Long-term revenue streams — Waste companies typically work on multi-year contracts that lock in steady revenue and tend to hold up during economic slowdowns. Businesses often sign contracts lasting one to three years, while larger companies and municipalities commonly agree to five- to seven-year terms. Contracts can be flat- or variable-rate and frequently include provisions for regulatory fees and fuel surcharges (which matter more as oil prices fluctuate).

This combination of essential demand and regulatory obstacles makes waste services a solid defensive investment. Historically, waste-management firms have held up well during market corrections and volatile periods. With the conflict in the Middle East ongoing and the S&P 500 near its 200-day moving average, market swings are likely to continue, making these waste-service companies worth a look. 3 Steady Waste Removal Stocks With Upside The AI bottleneck has shifted from chips to power. Goldman Sachs projects demand growing 15% per year, with 40% of AI facilities constrained by electricity shortages by 2027. One company holds $1.5 billion in backlog orders for the exact equipment these data centers need - yet Wall Street still prices it like a sleepy industrial stock. The June SpaceX IPO could change that fast. See the math Wall Street is missing before the SpaceX IPO The industry's oligopoly means only a handful of waste companies trade publicly on U.S. exchanges, narrowing investor options. With that context, here are three firms that offer a blend of upside, consistency, and dividend income while helping limit exposure to fluctuating fuel costs. Waste Management: The Cashflow King Waste Management Inc. (NYSE: WM) is the largest waste-removal company in the U.S. by market cap (about $94 billion) and by number of landfills, transfer stations, and recycling facilities. It is also shareholder-friendly. The company reported strong free cash flow of $2.94 billion in Q4 2025, and management expects free cash flow to grow more than 30% in 2026. Management is supporting that growth with a 14.5% dividend increase and $3 billion in share buybacks. Waste Management also limits the impact of fuel-price volatility through energy surcharges that pass diesel and compressed natural gas (CNG) cost increases on to clients.

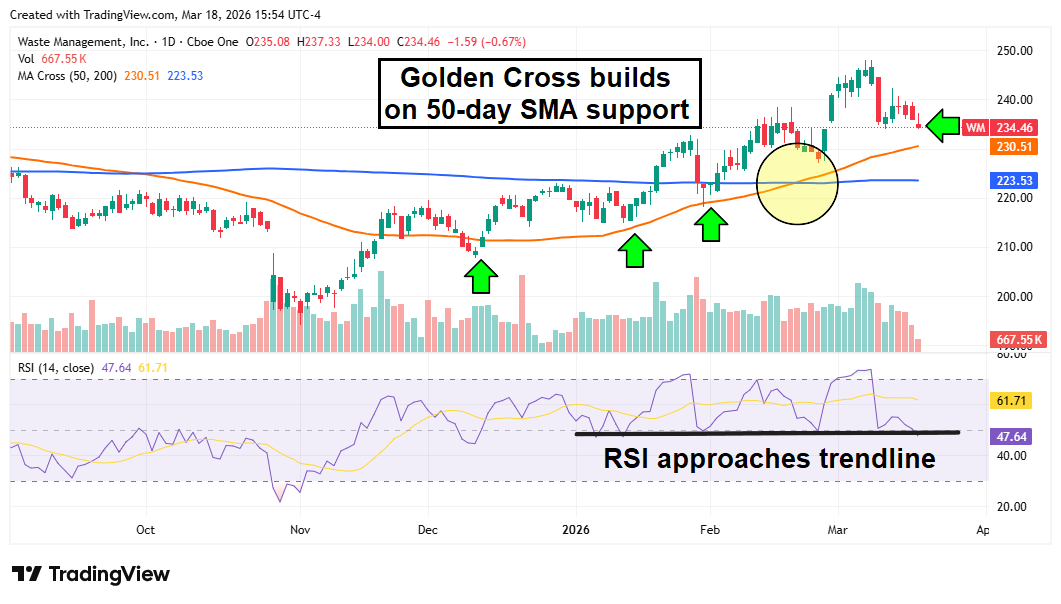

Technically, WM shares show the makings of a sustained uptrend, with a bullish Golden Cross and solid support at the 50-day moving average. A recent move into overbought territory on the Relative Strength Index (RSI) prompted a brief pullback, and the share price is now approaching the 50-day support again — a potential entry point for new buyers. The dividend currently yields 1.62%, with a 56% dividend payout ratio and a 22-year history of increases. Republic Services: Lower Leverage and Dividend Resilience Republic Services Inc. (NYSE: RSG) often ranks behind WM due to its smaller market cap, lower dividend yield, and fewer locations. But RSG brings some advantages WM lacks: it posted an earnings beat in Q4 2025 and maintains a cleaner balance sheet. RSG carries less debt and has engaged in less M&A than WM, which can mean slower growth but lower financial leverage. Its dividend yield is lower at 1.13%, but the DPR sits at a healthy 36%, leaving room for future increases. Republic also uses a fuel-surcharge model similar to Waste Management's, helping mitigate the effect of rising oil prices.

RSG shares have lagged WM so far in 2026, and the technicals show more conflict between buyers and sellers on the daily chart. However, if volatility persists, RSG can continue the breakout that began last November. The stock appears to have found support at the 50-day moving average, and the RSI is back to levels that previously marked short-term lows. A sustained move above the 200-day moving average could be the next catalyst. Clean Harbors: Upside From Government Contracts Clean Harbors Inc. (NYSE: CLH) isn't a traditional residential waste hauler like RSG or WM, but it offers potentially greater upside. More than 75% of the company's revenue comes from Environmental Services, a more cyclical stream than Collection and Disposal. Still, Clean Harbors benefits from one of its most reliable clients: the U.S. government. The company has a multi-year agreement with the Department of Defense for polyfluoroalkyl substances (PFAS) filtration services, with options to expand annually. PFAS are dangerous "forever chemicals" that may be present in water at more than 700 military bases. Clean Harbors is among the few companies capable of the full suite of PFAS filtration, remediation, and incineration services, giving it a meaningful moat and an advantage when pursuing additional government contracts.

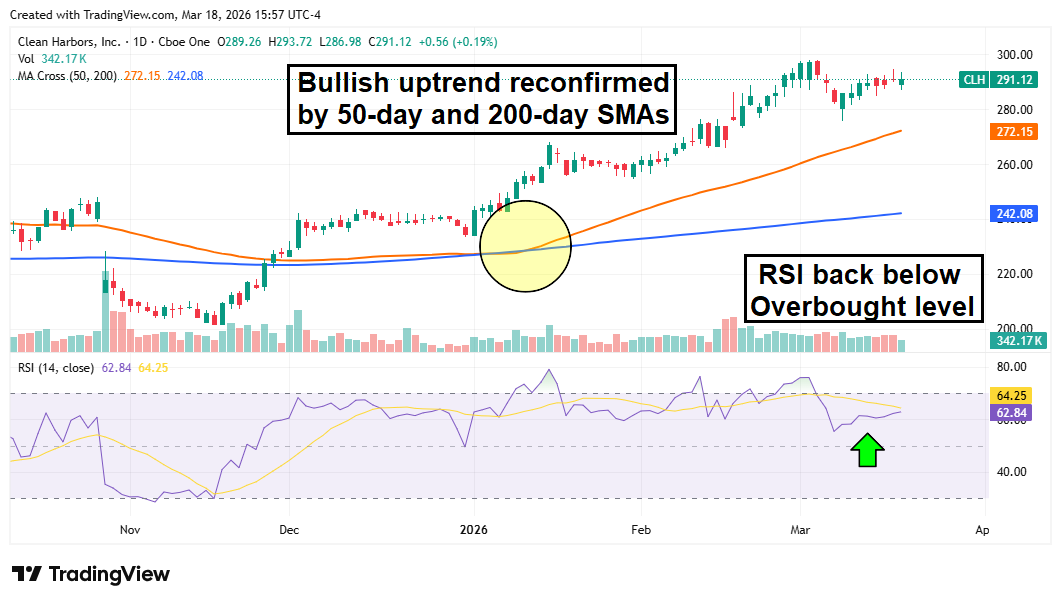

Investors generally favor companies with steady government contracts, and CLH shares have gained more than 20% year to date. The stock is in a strong uptrend, trading above both the 50-day and 200-day moving averages, with the RSI cooling from overbought levels. With the Department of Defense involved in sustained regional conflict, defense budgets may rise further, potentially boosting Clean Harbors' revenue. |

Post a Comment

Post a Comment