UBS raised its MU price target to $1,625, lifting semiconductor stocks broadly. These 3 stocks rallied in sympathy, but are the gains... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

|

|

| Written by Dan Schmidt

The raging semiconductor rally received another boost this week when UBS analyst Timothy Arcuri raised his price target on Micron Technology Inc. (NASDAQ: MU) to a stunning $1625, nearly triple its previous target. The stock was trading under $800 at the time of the upgrade, so the new target represented an upside of more than 100% and a company valuation of over $1.8 trillion. MU shares rallied nearly 20% the following day, and the entire industry seemed to join in, as the iShares PHLX Semiconductor ETF (NASDAQ: SOXX) accelerated 6%. When the entire industry seems to rally every day, it's easy for undeserving companies to get caught in the wave and soar to new all-time highs. But it's also crucial to remember Warren Buffett's quote about what happens when the wave recedes: you find out who’s been swimming without proper attire. Why UBS Boosted Their MU Price Target by 200%Arcuri’s May 26 MU price target boost reflected his view that high-bandwidth memory (HBM) is undergoing a fundamental shift from a cyclical semiconductor business to one driven by long-term AI infrastructure demand. Instead of a cyclical manufacturing industry, HBM now has structural growth tailwinds led by two key factors:

Long-term Revenue Visibility: AI hyperscalers are running into HBM backlogs and are more willing to lock in long-term agreements for supply and access to next-gen products. Micron already has agreements in place for its entire 2026 HBM supply. Concentrated Supply Chain: Producing HBM products at a large scale is a capability currently possessed by only three companies: Micron, Samsung Electronics Ltd. (OTCMKTS: SSNLF), and SK Hynix. In its Q1 2026 earnings report, Micron projects that data center demand for HBM will exceed $100 billion by 2028, more than three times the $35 billion in HBM sales to data centers in 2025. Given these secure, long-term agreements and heavy supply concentration, Arcuri argues that MU shares are worth a valuation similar to NVIDIA Corp. (NASDAQ: NVDA). However, the stock traded at under 10x forward earnings at the time of the call—far cheaper than the NASDAQ 100 average of 24x earnings, hence the massive re-rating. 3 Stocks Rallying in Sympathy: Hype or Substance?Many tech stocks in the AI and semiconductor space rallied hard in sympathy, especially Western Digital Corp (NASDAQ: WDC), Rambus Inc. (NASDAQ: RMBS), and onsemi (NASDAQ: ON). But are these gains warranted? Despite the industry's exuberance, each company still requires substantial due diligence to separate substance from hype. Western Digital: A Clean Complement to Micron’s SurgeWestern Digital Corp also rallied 8% the day of the report, bringing its total year-to-date (YTD) gain to over 200%. Western Digital is now a pure hard disk drive (HDD) manufacturer following the SanDisk spinoff, and the same logic that UBS applied to Micron’s HBM products also applies to Western Digital’s HDDs. Hyperscalers are locking in long-term agreements, and the company’s production capacity throughout 2026 has already been claimed. The fiscal Q3 2026 earnings report on April 30 confirmed the bull thesis with a massive double-beat featuring 45% year-over-year (YOY) revenue growth and gross margins over 50%.

Several technical staples underpin the lengthy rally in WDC shares. It has strong support at the 50-day moving average, which has traded above the 200-day moving average for over a year. A bearish crossover in the Moving Average Convergence Divergence (MACD) indicator briefly paused the rally, but now a bullish reversion appears to be underway as the stock makes new all-time highs. Rambus: Undervalued Logic Company Licensing Necessary IP to Data CentersRambus is a classic “picks and shovels” play on the memory storage theme. The company develops memory-interface systems that enable the GPU and memory stack to communicate within the data center mainframe, and licenses them as IP. High-margin licensing products that can be sold regardless of which memory company wins the design provide a steady, recurring revenue stream. Additionally, the firm’s HBM4E Memory Controller, launched in April, is now the industry's fastest. The stock has surged more than 60% YTD but remains undervalued relative to peers in the AI space.

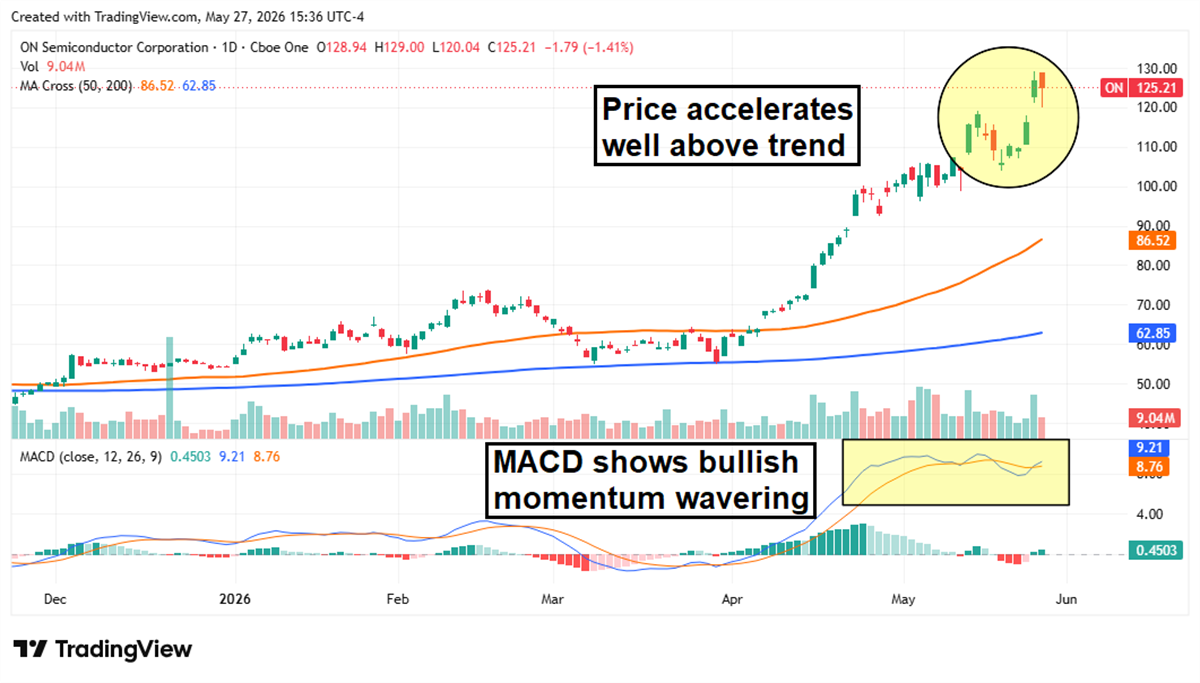

RMBS shares have been more volatile than WDC, but volatility is often the price investors pay for higher upside. The stock spent two months stuck in neutral, bouncing between the 50-day and 200-day moving averages as the Relative Strength Index (RSI) remained in bearish territory. However, an April rally sent the price above the 50-day moving average, and the momentum stalled when the RSI crossed above 50 into the bullish range. The 50-day moving average now appears to be support, which bodes well for future upside potential. onsemi: Sympathy Rally Without the Substanceonsemi also rallied 9% on the day of the Micron report, but the UBS thesis doesn’t really apply here. The company traditionally makes chips for the automotive and industrial markets, which are cyclical and not closely tied to the broader AI space. onsemi has some data center business, but it accounts for only a small portion of the company’s total revenue. For example, the $797 million in Q1 automotive revenue was more than half of the company’s total Q1 2026 sales. Management expects data center revenue to double YOY in 2026, but that’s still just $500 million out of a projected revenue base of more than $6 billion.

While the company has a compelling bull thesis of its own, it remains outside the Micron paradigm. And an almost 90% gain over the last three months has the stock looking frothy. The price is now well above trend, and the MACD is hinting that the bullish upswing is losing momentum. It might be a good time to take profits on ON shares.  Read This Story Online Read This Story Online |

Tom Busby, Founder and CEO of the Diversified Trading Institute, has spent decades refining trading strategies - from his days in the Air Force to today's markets.

He's compiled everything into 'The Little Black Book of Trading Strategies,' and right now he's offering it at no cost. This is one of the most comprehensive guides available for traders looking to sharpen their edge. Download your free copy of the Little Black Book today

|

| Written by Thomas Hughes

Snowflake (NYSE: SNOW) is only the latest example of how the AI flywheel is gaining momentum. Demand for the company’s product is hot, exceeding expectations and driving management to increase spending. Increased spending leads to new demand, increased revenue, and an improved outlook—and the cycle has only just begun. The likely outcome is that Snowflake and other well-positioned software-as-a-service companies will continue to accelerate in the coming quarters and sustain high-level growth well into the future. More importantly, Snowflake, unlike some other AI up-and-comers, is profitable and driving intrinsic value for its shareholders. Snowflake Accelerates in Q1, Guides for Strength in Q2Snowflake had a robust quarter, as shown in its Q1 earnings: revenue growth accelerated to 33%, outpacing consensus by over 500 basis points, the strongest growth in nearly three years. The $1.39 billion in revenue was underpinned by a 34% increase in product sales, driven by new clients and increased penetration. The number of large clients contributing more than $1 million in annual recurring revenue increased by 29%, while net new clients increased by 28%. Net retention, a measure of revenue generated from existing clients, was also strong, up by 126% as AI adoption continues to accelerate. Margin news was also good. The company keeps posting GAAP losses due to heavy investments, but remains profitable at its core. Adjusted earnings per share came in at 39 cents, up more than 60% year-over-year and 2,200 bps above forecasts, outpacing the top-line strength by 1700 bps. Looking ahead, strength is expected to continue, and the guidance may be overly cautious. Management forecasts Q2 revenue to grow 30% at the midpoint, which was better than expected, and raised the full-year revenue target by 400 bps. The $5.84 billion target implies a 31% year over year increase and will likely be increased again before the year is over. Remaining performance obligation, the measure of contracted but unearned revenue, grew by 38%, suggesting business momentum continues to grow. Analysts' Revisions Go Into Overdrive—Snowflake to Hit Fresh HighsAnalysts responded robustly to the news. MarketBeat tracked a half dozen revisions within the first few hours of the release, affirming the bullish trends and leading price action to the high end of the target range. As it stands, the 41 analysts tracked provide high conviction in the Buy rating, with 35 of 41 (85%) ratings pegged at Buy, and a consensus price target of $277. The high-end range of new price targets would be sufficient to put this market at a multi-year high. Takeaways from the chatter include the impact of the new Amazon Web Services (AWS) deal and the Natoma acquisition. The AWS deal amounts to billions in new spending over the next five years, but for the capacity and infrastructure to drive business. The likely outcome is that Snow continues to gain share and monetizes its investment over time, and the Natoma acquisition amplifies the outlook. Natoma’s platform helps connect AI tools to existing apps, both inside and outside the Snowflake platform, providing utility across the ecosystem. Snowflake Market Melts Up, Again—This Time It May StickSnowflake’s market responded vigorously to the news, rising by more than 30% in its wake. The move signals solid support at the market lows, affirming the deep value presented in early May, and a high probability of continuing higher. The question is whether SNOW will continue higher immediately or whether profit-takers will cap gains. The 30% overnight increase in the stock price made some traders millionaires, creating an unmissable opportunity for profit-taking. Critical resistance targets are near $240 and $280; critical support is near the cluster of exponential moving averages near $190.

Snowflake’s biggest risks are its valuation and competition. Competition for data management is fierce, including from megacap players such as Alphabet (NASDAQ: GOOGL) and Microsoft (NASDAQ: MSFT). While Snowflake provides utility, they have the scale and finances to capture share. In this environment, execution is critical, and the high valuation sets the stage for large pullbacks. Trading at over 100X its current-year earnings, any signs of weakness in upcoming reports or bullish news from competitors will be reflected in the stock’s price. The caveat is that this market is pricing in a robust growth trajectory. Consensus forecasts put this stock below 10X earnings before 2035, suggesting it could rise 100% to 200% from the $235 level. Short-selling is also a risk, but not as pronounced as it is with some tech names. The short interest was rising ahead of the report, but pegged at only 6% of the shares. It's likely that short covering helped amplify Snowflake’s post-release price surge. Read This Story Online |

On July 17th, the House passed the GENIUS Act - and at least one prominent Trump ally is raising alarms. Rep. Marjorie Taylor Greene claims the bill contains 'the entire setup, groundwork and infrastructure to move from cash to digital currency.'

If the legislation becomes law, the implications for how Americans store and control their money could be significant. There may be a limited window to act before it takes effect. Learn what steps you can take to protect your wealth before this becomes law

|

| Written by Jeffrey Neal Johnson

While retail capital chases the computational firepower of AI logic chips, a more fundamental story is unfolding in the circuitry that powers them. The insatiable energy demands of next-generation data centers and electric vehicles (EVs) are forcing a non-negotiable architectural shift from legacy 48-volt systems to 800-volt platforms. This transition transforms analog power management integrated circuits (PMICs) from simple components into mission-critical bottlenecks. Institutional capital is taking notice, quietly building positions in the gatekeepers of this power revolution. Two innovators, Texas Instruments (NASDAQ: TXN) and onsemi (NASDAQ: ON), are positioned at the absolute epicenter of this supercycle. Armed with aggressive buybacks, recent sell-side upgrades, and the structural leverage to dictate the pace of AI expansion, they represent a compelling, and perhaps underappreciated, way to invest in the future of technology. An AI Problem of Physics, Not Just CodeThe AI boom is fundamentally an energy problem. As data center racks surpass 100 kilowatts of power density to support clusters of advanced GPUs, traditional 48V power distribution architectures are hitting a thermal wall. The physics are unforgiving. Since power loss (as heat) is proportional to the square of the current (I²R), doubling the voltage from 400V to 800V cuts the current in half, thereby slashing energy losses by 75%. This move isn't just an optional upgrade; it is an economic and engineering necessity that allows for thinner, lighter copper wiring and dramatically less waste heat. This is where the thesis for analog semis gains its power: these companies provide the sophisticated chips needed to safely and efficiently manage high-voltage environments. Texas Instruments has evolved from being a component supplier to a core architectural partner for the biggest names in tech. The collaboration with NVIDIA (NASDAQ: NVDA) on a complete 800V DC power framework proves that next-gen logic cannot scale without a corresponding leap in power delivery. By enabling a more direct, efficient power-conversion path from the 800V source to the processor, the technology developed by Texas Instruments drastically reduces the number of failure points and costly conversion stages. onsemi is carving out a dominant position by focusing on intelligent power solutions. The acquisition of Aura Semiconductor's power IP directly targets the high-margin data center market, giving onsemi critical power-management technology at the point-of-load. Simultaneously, its silicon carbide (SiC) technology has become the gold standard for high-efficiency EV platforms. At the 2026 Beijing Auto Show, onsemi's SiC solutions were featured in an estimated 55% of new EV models, including next-generation 900V platforms from global players like Geely (OTCMKTS: GELYY) and NIO (NYSE: NIO), cementing its role as a key enabler of vehicle electrification. Reading the Voltage on Corporate ConfidenceAn investor can learn a lot by watching how a management team allocates capital. In this regard, onsemi is sending one of the market's clearest signals. The board is actively executing a massive $6 billion share repurchase program, authorized in late 2025, giving it the mandate to retire nearly a third of its outstanding shares. Investors should see this as more than a financial maneuver; it is a statement of profound confidence from leadership that believes onsemi's stock price is fundamentally undervalued. To fuel this aggressive buyback without throttling investment, onsemi recently announced a $1.3 billion convertible senior notes offering. This is a savvy move, providing immediate strategic capital to execute the buyback while protecting the R&D budget for critical technologies, such as its Treo platform, which saw staggering 2.5x sequential growth in Q1 2026. This use of intelligent leverage signals a belief that future stock appreciation will far outweigh the cost of debt. Texas Instruments, a more mature and diversified player, demonstrates its strength through operational resilience. Management acknowledged some near-term choppiness in the Chinese automotive sector during its Q1 2026 earnings call, a potential macro headwind. Yet, Texas Instruments' financial performance shows that this weakness is entirely offset by growth in its Data Center and Industrial segments. The stock's exceptionally low short interest of 1.72% suggests that bears have largely given up betting against this diversified powerhouse. Wall Street Flips the Switch on Price TargetsThe sell-side is beginning to align with this powerful thesis. Bank of America recently raised its price targets for both companies. It raised its target for onsemi to $138, citing underappreciated content gains in AI data centers. It also lifted its Texas Instruments target to $370, forecasting that Texas Instruments' data center business alone could reach $4.5 billion by 2028, accounting for up to 18% of total sales. This pivot is particularly relevant for onsemi. The stock still carries a significant short interest of 7.47%, representing over 29 million shares sold short. This creates a compelling technical setup. With management now confirming that the period of inventory digestion in its legacy automotive business is "largely behind us," the operational catalysts are aligning. A high short float, a massive corporate buyback, and a positive inflection in the core business create classic conditions for a potential short squeeze, where a rush of short covering could fuel upside volatility. The Analog Opportunity: A Charged Path ForwardThe core argument is simple: for every dollar spent on a high-powered AI logic chip, an increasing share must be allocated to the sophisticated analog technology required to power it efficiently and reliably. The secular shifts toward AI and vehicle electrification are structural, long-term tailwinds that appear poised to benefit both Texas Instruments and onsemi for years to come. Of course, no investment is without risk. The semiconductor industry is historically cyclical, and both enterprises face intense competition and are subject to geopolitical risks associated with global supply chains. A broader economic downturn could also temper demand in their key industrial and automotive markets. Given the strong year-to-date performance, where the stock price for Texas Instruments is up 80%, and onsemi has climbed 130%, some investors may prefer to wait for a broader market pullback before initiating a position. Cautious investors might consider adding both Texas Instruments and onsemi to a watchlist to monitor for attractive entry points, as the 800V supercycle appears to be in its early innings. Read This Story Online |

Everyone is watching June 12 - the SpaceX listing date. The real deadline is June 4, when Goldman Sachs, Morgan Stanley, and the largest funds begin presenting SpaceX's S-1 to clients.

Buried in that filing is a small, publicly traded company that builds critical power infrastructure Musk's Colossus can't operate without. Right now it trades like a sleepy industrial stock. Dylan Jovine has the ticker and is releasing it before the roadshow begins. Get the ticker name before June 4 changes the price

|

|

More Stories

|

|

|

Post a Comment

Post a Comment