Dear Reader,

Pull up Tesla's most recent SEC filing. Page 5.

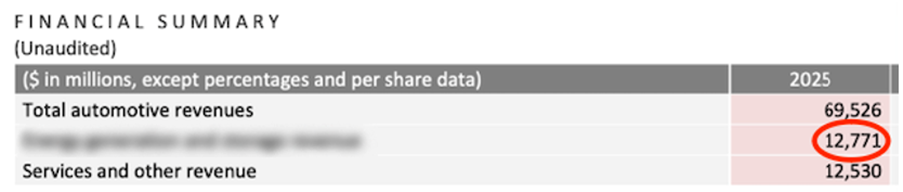

And you'll see a single line showing $12 billion in revenue from a brand-new "super startup" Elon Musk has been quietly incubating inside Tesla.

This new "super startup" has nothing to do with cars, or robots, or space or AI…

But it sits at the center of what Blackstone calls "a $23 trillion investment opportunity."

And on July 22, Elon is expected to pull back the curtain and reveal exactly what he's building.

But former hedge fund manager Adam O'Dell already knows… and he reveals it all in this urgent video.

Adam believes this will go down as Elon's greatest ever invention, and his biggest ever disruption…

And that investors who position themselves before this becomes front-page news could walk away wealthier than they ever thought possible.

Go here to watch Adam's full briefing now... And he'll even give you the name and ticker of one of his top picks to play it — completely free.

Regards,

Adam O'Dell

Chief Investment Strategist, Money & Markets

Marvell’s Pullback May Be the Setup Bulls Were Waiting For

Reported by Thomas Hughes. Posted: 5/29/2026.

Key Points

- Marvell is a nuts-and-bolts play on AI that is gaining momentum in 2026.

- Analysts' trend forecasts push the high end of the range, projecting a 50% upside from the late May highs.

- Price weakness is an opportunity to buy; the next big catalyst will come in August.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Marvell Technology’s (NASDAQ: MRVL) market signaled a top in late May, gapping up after strong fiscal Q1 2027 results only to fade from the highs and form an ominous candle.

The candle suggests a peak and the potential for a pullback, which is the key issue in June.

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereA price pullback is likely; the only question is how deep it goes and how long it takes for the next highs to be set.

In this case, those next highs are likely to come by year-end, if not by the end of summer, because business is good at Marvell and still accelerating.

Marvell’s Charts Say It All—This Market Is Gaining Strength

The strength of Marvell’s business, its position in the AI ecosystem, and its growth trajectory are reflected in the technical chart action. The market knows what there is to know about Marvell, and the stock is gaining momentum. Price action shows MACD convergence across two critical time frames, the weekly and monthly charts, a sign of market strength that is reinforced by increasing volume. Volume is an important factor because it reflects market commitment rather than a hollow move driven by just a few buyers. In this scenario, Marvell’s price is more likely to rebound from its correction and set a new high than not.

As for the possibility of a pullback, Marvell’s support targets are near $180 and $160. The $180 level aligns with the short-term 30-day EMA and may not be strong enough to support price action on its own, given the valuation and the arrival of summer trading conditions. Investors should expect lower volume and more exaggerated price swings until September, when the market returns from summer vacation. The $160 target is stronger, aligning with a congestion band that suggests elevated ownership at that level.

Institutions are likely buyers and help limit the downside risk. They own more than 80% of the stock and have been aggressively accumulating at a nearly 2-to-1 pace. The risk is that they step to the sidelines and wait for a deeper pullback, allowing a larger move to unfold. In that scenario, Marvell could fall below $160 and potentially retrace all of its 2026 gains to retest the 2025 high before rebounding. Valuation metrics also point to this risk, as Marvell trades at more than 50 times current-year earnings.

Marvell: Strategy Execution Equals Multiple Expansion

Valuation metrics, however, also suggest Marvell’s stock price will recover from the correction and reach new highs this year. Trading at more than 50 times this year’s earnings, the market is pricing in robust growth and, so far, forecasts have been too low. The long-term outlook puts this stock at approximately 6X the 2035 consensus forecast, setting the stage for a 300% to 400% increase in the stock price over time, assuming fair value relative to the S&P 500. If Marvell continues to command a premium, as many blue-chip tech growth companies do, the upside potential is even greater.

Analyst trends are another factor pointing to fresh highs for this stock. Analysts responded strongly to Marvell’s guidance update, with many revisions more than doubling existing price targets. The net result was a 65% overnight increase in the consensus target, with all new targets pushing the high end of the range higher. The high-end target is $300 as of late May, which represents 50% upside from the pre-release closing price.

Marvell’s Q1 results echo those reported across the AI ecosystem. AI spending is accelerating, and virtuous cycles are forming: AI infrastructure drives AI applications, which in turn increases demand. Revenue grew 28% to $2.42 billion, accelerating sequentially on strength in optics, switches, and interconnect devices for scale-up (bigger clusters) and scale-out (more clusters). Revenue set a record, was supported by operational leverage, and was followed by robust guidance.

Margin news was solid. The company produced record margins and profits, driving nearly $640 million in cash flow. Balance sheet highlights also show strength, with cash, current assets, and total assets rising, and equity increasing despite acquisitions, aggressive reinvestment, and capital returns. Equity, the measure of shareholder value, improved by 27%, leaving the company in a fortress-like position. Long-term debt is less than 1.5 times cash and less than 0.25 times equity.

Guidance provides both support for the market and a catalyst. The company guided Q2 revenue to $2.7 billion, a YOY acceleration of 35%, with earnings of 93 cents, 3 cents better than expected. The catalyst is the potential for outperformance, which is expected in late August. The biggest risk for Marvell is customer concentration. Its largest customers are hyperscalers Amazon (NASDAQ: AMZN), Microsoft (NASDAQ: MSFT), and Alphabet (NASDAQ: GOOGL); the risk is that they turn to other solutions, but that does not appear to be a concern this summer.

Palantir Stock Faces Technical Pressure Despite Strong AI Growth

Reported by Chris Markoch. Posted: 6/1/2026.

Key Points

- Palantir continues posting strong revenue growth and industry-leading margins despite stock volatility.

- Wall Street remains divided between bullish AI expectations and concerns about valuation.

- Technical indicators suggest PLTR may face additional near-term pressure before a sustained breakout.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Another week for Palantir Technologies (NASDAQ: PLTR) that can be summed up as: the more things change, the more they stay the same. PLTR is down 12% in 2026, and many retail investors, if the online chatter is any indication, are bailing on the stock.

Palantir was once a rebellious stock that refused to grow into its valuation over the last two years. It’s starting to do that now, and some investors are convinced the stock’s best days are behind it. Well, if you define best days as 10x returns, that may be true.

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereBut the company investors are buying today has results that support a long-term bull case. If that’s the case, then buying the stock at these levels may be a gift that won’t be fully appreciated for several years.

Cantor Fitzgerald Delivers a Backhanded Compliment

Palantir received a quiet but meaningful vote of confidence on May 22, when Cantor Fitzgerald hosted CFO David Glazer and Chief Architect Akshay Krishnaswamy for an investor meeting.

Cantor came away incrementally more bullish on Palantir's positioning to benefit from secular AI growth trends in both U.S. Commercial and Government markets. The firm noted that Palantir continues to gain traction as a leading ontology and orchestration layer for enterprise AI, using large language models (LLMs) and the company's unique FDE (Federated Data Environment) go-to-market motion to create a deterministic, continuously updating data analytics system that governs enterprise operations.

Palantir's Ontology acts as a real-time digital twin, integrating operational data, workflows, security, APIs, and human inputs to ground AI-driven decisions and agentic workflows in an enterprise context.

The firm pointed to Palantir's 84% gross margin and 68% revenue growth over the past 12 months. And yet, Cantor kept its Neutral rating and $138 price target because the stock looks expensive.

This is notably conservative compared to peers. Other firms, including Citigroup and Rosenblatt, recently raised their targets to $225 following Palantir's strong Q1 results, with earnings per share of 33 cents on $1.633 billion in revenue, both topping estimates.

It would seem that Cantor is more impressed with Palantir's AI platform story than before, but the valuation gap between its $138 target and the bull camp's $225–$230 targets reflects a real divide on Wall Street about how much to pay for that growth.

The Chart Tells a Cautious Story

For investors who follow price action, PLTR's chart adds another layer of complexity to an already nuanced fundamental picture. After peaking near $210 in mid-November 2025, the stock collapsed sharply to a low around $120 by late January—a steep decline that created what technical analysts call a "flagpole." Since then, PLTR has slowly ground higher in a choppy, narrow range between roughly $125 and $145, a consolidation that has now stretched for nearly three months.

That pattern has the look of a bear flag—one of the more reliable bearish continuation setups in technical analysis. The structure forms when a sharp decline is followed by a slow, low-conviction drift higher, before sellers re-engage and push the stock to new lows. The longer the flag flies without a breakout to the upside, the more it tends to favor the bears.

Wednesday's session itself was telling. The stock tagged an intraday high of $135.73 before sellers stepped in hard, pushing it back down to close at $132.51, a loss of nearly 3% on the day. That kind of rejection near resistance is exactly the type of price action bears watch for.

The key support level to monitor is around $130, which corresponds to a horizontal zone that has held multiple times over recent months. A decisive close below that level would technically confirm the bear flag breakdown and open the door toward a retest of the February lows near $120. On the upside, the $135 to $138 zone represents both near-term chart resistance and, notably, the exact price target Cantor Fitzgerald assigned this week—a level that may prove easier to defend in analyst models than on a candlestick chart.

None of this means the bull case is broken. Fundamentally, Palantir remains one of the more compelling AI infrastructure stories in the market. But for investors eyeing an entry, the chart suggests patience may be rewarded. A clean hold of $130 and a reclaim of $140 would go a long way toward neutralizing the bearish technical setup and giving the long-term thesis room to breathe.

Don’t Pass on PLTR Without Knowing Why

Palantir is not a stock for investors looking for excitement or a quick win. The days of triple-digit annual returns are almost certainly in the rearview mirror, and anyone expecting that kind of ride again is likely to be disappointed.

What remains is something arguably more valuable: a company with a defensible AI platform, expanding margins, and a growing footprint in both government and enterprise markets. The stock is cheaper than it was six months ago, but it is still not cheap by conventional measures, and the chart suggests the path of least resistance may still be lower before it is higher.

For patient, long-term investors willing to look past near-term volatility and a valuation that will never satisfy the skeptics, current levels could look like a reasonable entry point in hindsight. For everyone else, there are flashier trades out there. But don’t be surprised if PLTR quietly compounds while you are chasing them.

This email is a sponsored message sent on behalf of Banyan Hill Publishing, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you would like to unsubscribe from receiving offers for Strategic Fortunes, please click here.

If you have questions or concerns about your newsletter, please don't hesitate to email MarketBeat's U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Pl. #620, Sioux Falls, SD 57103. USA..

Post a Comment

Post a Comment