The Coca-Cola Company plans to spin off its Indian bottling unit to unlock massive latent equity value and drive long-term structural margin... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

|

|

| Written by Jeffrey Neal Johnson

The Coca-Cola Company (NYSE: KO) is orchestrating a masterful strategic pivot to unlock tremendous shareholder value. This is not a complex financial derivative or a speculative tech venture, but rather a powerful, time-tested strategy: the emerging market spin-off. Coca-Cola has officially signaled its intent to take its primary Indian bottling unit, Hindustan Coca-Cola Holdings (HCCH), public in a 2027 Initial Public Offering. This move is the crown jewel in a global strategy to transform Coca-Cola into a high-margin, asset-light powerhouse, a shift that could fundamentally enhance the return on every dollar the company invests for years to come. For investors, this is the most significant catalyst on the horizon, providing a direct mechanism to monetize the explosive growth of the Indian consumer class. By separating its capital-intensive bottling infrastructure from its brand and high-margin syrup business, Coca-Cola is creating a blueprint for structural margin expansion and a more agile capital-allocation strategy. From Bottler to Licensor: Coke's High-Margin Pivot in IndiaThe potential 2027 IPO is the capstone of a deliberate, multi-year refranchising strategy within India, which currently stands as Coca-Cola's fifth-largest market by volume. The groundwork was laid with the July 2025 deal that brought the Jubilant Bhartia Group, a formidable local conglomerate, on board as a 40% stakeholder in HCCH. This strategic partnership was a critical first step, offloading operational risk while gaining a partner with invaluable, on-the-ground market intelligence. Now, the public listing aims to raise over $1 billion and establish a total enterprise valuation for HCCH north of $10 billion. To steer this massive undertaking, Coca-Cola has appointed the prestigious firm Rothschild & Co as its lead advisor, a clear signal to the market of the seriousness and institutional caliber of this transaction. This strategic sale effectively completes Coca-Cola's transformation in the region, shifting it from an owner of factories and truck fleets into a brand owner, marketer, and concentrate supplier of its world-famous brand and a supplier of its incredibly profitable concentrate. It's a leaner, more profitable model that focuses on what Coca-Cola does best: marketing and brand management. India's IPO Could Be Worth More Than You ThinkThe true scale of the value waiting to be unlocked becomes crystal clear when held up against a regional competitor. Varun Beverages, the key bottling partner for rival PepsiCo (NASDAQ: PEP) in the region, provides an excellent and highly relevant benchmark. Varun Beverages trades at a steep trailing P/E ratio of roughly 57x and commands a price-to-sales multiple of approximately 8x. By contrast, the proposed $10 billion IPO valuation for HCCH pegs it at a far more conservative 7.5x fiscal 2025 sales. This discrepancy represents a significant valuation gap and, for investors, a clear path for potential multiple expansion after the IPO. If the public markets decide to award HCCH a valuation in line with its closest peer, the financial upside for the new entity, and the value reflected back to The Coca-Cola Company, could be immense. This arbitrage opportunity is the core of the thesis, showcasing the value that is currently buried within Coca-Cola's vast corporate structure. Beneath the Surface: Insider Sales and Institutional HedgingWhile the long-term strategic picture is compelling, investors must always examine the short-term flow of funds. Recent SEC filings do show that insiders, including Executive Chairman James Quincey, have sold over $64 million in stock over the past 90 days. Such sales near 52-week highs can certainly create overhead resistance for the stock price. Simultaneously, short interest in Coca-Cola has increased to 48.26 million shares. However, digging into the data reveals that nearly 64% of this short activity is happening on off-exchange dark pools. This is a crucial detail, as it suggests the activity is not a direct bearish bet against Coca-Cola. Instead, it is more characteristic of large institutions using sophisticated strategies to hedge massive, long-term positions against broader market risks. These data points do not appear to challenge the core business's fundamental strength. Coca-Cola delivered robust Q1 2026 results, showing 10% organic revenue growth and exceptional operating margins of 35%. Shedding the capital-intensive assets of HCCH and its 2,000-plus distributor network is a direct strategy to push those already impressive margins even higher. How India's Consumers Will Fuel Coke's Next ChapterThe strategic logic behind this IPO would be underpinned by India's undeniable economic strength. With a young, rapidly growing population and rising disposable incomes, the country represents a multi-decade tailwind for consumer goods. The non-alcoholic beverage market is at the epicenter of this growth, as a new generation of consumers seeks convenient, premium products. By creating HCCH as a distinct, publicly-traded company, The Coca-Cola Company is forging a purpose-built vehicle to capture this regional expansion. The capital unlocked from the IPO will be directly injected into strengthening this engine of growth, expanding distribution into new territories, and innovating to meet local tastes. For investors in The Coca-Cola Company, a stock that has already outperformed competitors like Keurig Dr. Pepper (NASDAQ: KDP) this year, the 2027 IPO is the most important catalyst to watch. It is a clear and powerful signal that this iconic American brand is not resting on its laurels but is actively engineering its business to win the future.  Read This Story Online Read This Story Online |

Michael Burry - the man who made $725 million shorting the 2007 housing market - quietly deregistered Scion Asset Management with the SEC last November, ending all future 13F filings. His final disclosure showed $912 million in Palantir puts and $187 million against Nvidia.

On April 8, 2026, a single Burry post on X wiped roughly $23 billion from Palantir's market cap in 90 minutes. He has since expanded his shorts to QQQ and SOXX, while going long beaten-down software names like Adobe, Salesforce, and MercadoLibre. The Shiller CAPE on May 8 hit 40.1 - the highest since the 2000 tech bubble. See the full rotation Porter Stansberry is making right now

|

| Written by Jeffrey Neal Johnson

The June 1 execution of the FedEx Freight separation permanently restructures the global logistics sector, immediately infusing FedEx with a $4.1 billion cash dividend while isolating capital-intensive less-than-truckload operations. By definitively neutralizing the historical sum-of-the-parts (SOTP) discount, the newly streamlined express enterprise is positioned to drive aggressive margin expansion, optimize return on invested capital, and command premium market multiples. This corporate unbundling is the definitive value play of 2026, and investors should be monitoring post-spin FedEx Corp. (NYSE: FDX) as leaner operations and refined capital allocation attract attention. A $4.1 Billion Special Dividend DeliveryOn June 1, 2026, FedEx Corp. finalized the tax-free spin-off of its less-than-truckload (LTL) division, creating the independent, publicly traded FedEx Freight (NYSE: FDXF). The strategic imperative behind this move is clear: to unlock shareholder value by separating distinct business models with fundamentally different capital requirements. The parent company, FedEx Corp., now sharpens its focus on the high-margin global express and parcel delivery network, a business defined by speed, technology, and network effects rather than raw physical asset intensity. The mechanics of the separation provided an immediate and substantial benefit to the FedEx Corp. balance sheet. Before the split, FedEx Freight financed and paid a $4.1 billion cash dividend directly to its parent. This infusion provides significant liquidity for debt reduction, share repurchases, or reinvestment into the core Express business's technological and logistical infrastructure. Furthermore, FedEx Corp. retained a 19.9% stake in the newly independent FDXF, an asset earmarked for strategic disposal over the next two years, likely through exchanges designed to efficiently retire existing debt. This structure gives management a powerful tool for deleveraging while retaining short-term upside exposure to the LTL market. To ensure leadership continuity and operational focus, the C-suite was immediately realigned. John Smith assumed the role of CEO at FedEx Freight, while Claude Russ took the Interim CFO position at FedEx Corp. This dedicated leadership allows each management team to pursue strategies tailored to their specific markets, free from the competing capital-allocation demands of a diversified conglomerate. Unlocking Express Division ProfitsFor years, investors have argued that the capital-intensive nature of the LTL freight business, which requires heavy investment in trucks and terminals, has obscured the true profitability of the core Express division. Combining these disparate models into a single entity often leads to a sum-of-the-parts discount, in which the market values the consolidated company below the sum of its individual businesses' values. The market struggles to apply a clean valuation multiple to a business with two different growth and margin profiles. By shedding the LTL segment, FedEx Corp. appears poised to demonstrate a significantly higher return on invested capital (ROIC). ROIC is a critical metric that measures how effectively a company uses its capital to generate profits. The remaining Express and Ground businesses are less capital-heavy and generate stronger cash flows relative to their asset base. A higher ROIC is a powerful magnet for long-term capital, as it indicates a company has a durable competitive advantage and a management team skilled at disciplined capital allocation. This newly clarified financial profile is more attractive to investors who prioritize capital efficiency and margin expansion. The upcoming Q4 earnings call on June 23, 2026, will be a critical first look for analysts to model the margin improvement potential of the streamlined enterprise. Learning From the Leader: XPO's Success Validates FedExInvestors looking for a roadmap for this type of corporate action need look no further than XPO Inc.'s (NYSE: XPO) recent history. XPO's multi-year strategy of spinning off its logistics and truck-brokerage divisions transformed the company into a pure-play LTL carrier. The market's reaction provides a compelling case study for the value-unlock thesis. Year-to-date, shares of XPO have appreciated about 60%, reflecting investor appetite for focused, best-in-class operators. Its first-quarter 2026 results beat analyst expectations, with revenue of $2.10 billion and earnings per share of $1.01. However, this success has driven valuation to elevated levels, with a trailing P/E ratio sitting near 74x. While this premium validates the market's enthusiasm for the pure-play LTL model, it also introduces a note of caution. Macroeconomic headwinds, including inflationary pressures and potential tariff disputes, could challenge such a high multiple, underscoring the need for flawless execution from all players in the LTL space. XPO has set the precedent, and now FedEx Corp. has the opportunity to show its own path to a premium valuation. Smart Money Doubles Down on a Streamlined FedExA key indicator of market sentiment can be found in institutional ownership and short interest data. A high level of institutional ownership suggests that sophisticated, long-term investors are confident in a company's strategy. At the same time, low short interest indicates a lack of significant bearish conviction. FedEx Corp. currently exhibits a strong institutional ownership floor of nearly 85%. More telling is the muted short interest, which remains low at just 1.5% to 1.77% of the float. With a days-to-cover ratio of only 3.7, it is clear that few major funds are betting against the success of this spin-off. The absence of a significant short thesis lends credibility to the SOTP value-unlock narrative. Further bolstering the case for investors is FedEx Corp.'s recalibrated commitment to shareholder returns. On June 2, 2026, FedEx Corp. is scheduled to announce an adjusted annualized dividend of $5.80 per share. This move thoughtfully preserves FedEx's five-year history of consecutive dividend growth while aligning the payout with the new, leaner capital structure. It signals management's confidence in the post-spin entity's ability to generate consistent and predictable cash flow. Investors focused on companies undergoing strategic transformation may find the new FedEx a compelling story. The freight separation is complete, the balance sheet is strengthened, and the business is now focused on its most profitable core. The key variable remains execution, and the upcoming earnings report will provide the first data-driven glimpse into the operational efficiencies unlocked by this defining corporate action. Read This Story Online |

The Fed held rates steady while inflation sits at 2.4% and geopolitical pressure keeps volatility elevated. Reacting late in this kind of tape can get expensive fast.

Mastering Options Trading: Ultimate Guide to Success walks through bullish, bearish, and sideways setups - including an income-focused approach for targeting quality stocks at better entry prices and managing risk when earnings and macro news collide. Get the options guide and build your plan before the next move

|

| Written by Thomas Hughes

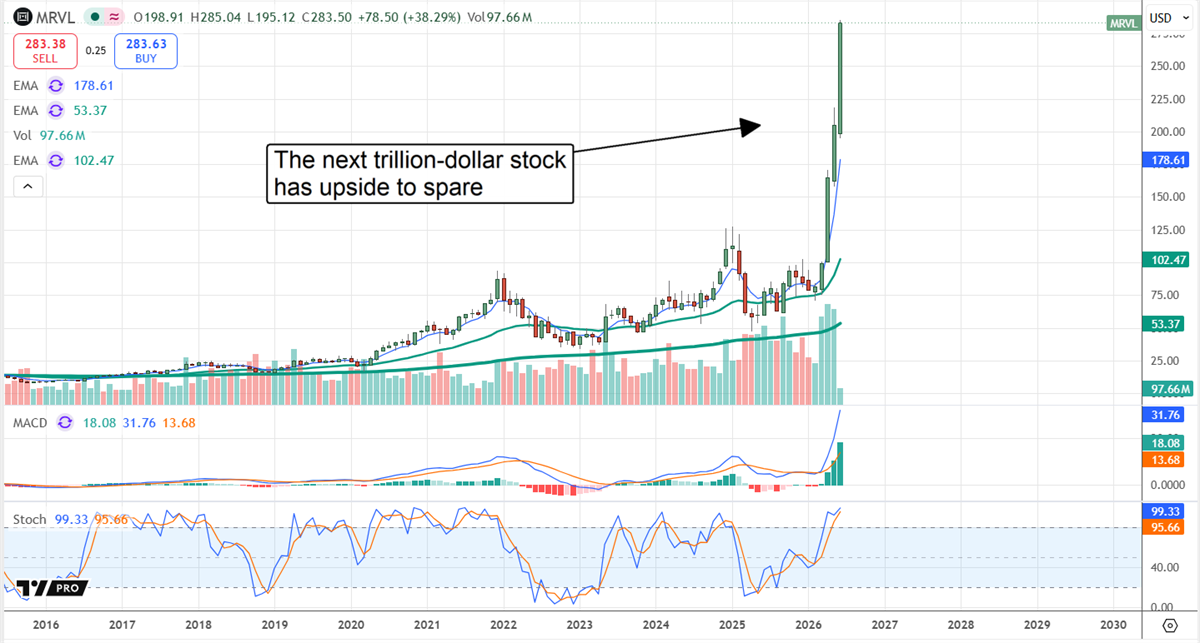

The calendar Q1 2026 earnings reports were incredibly good. The result at the end of the season is that the S&P 500 grew earnings by more than 28%, more than doubling the best-case scenario presented ahead of the period. While impressive, what’s more impressive is that the forward outlook was also improved, expects strength to persist into next year, and is likely to be cautious. The takeaway for investors is that a robust tailwind supports broad market activity, and it's only getting stronger. Q1 earnings strength was broad-based, but the leading sector was technology—no surprise there. The surprise was the strength seen in companies other than NVIDIA (NASDAQ: NVDA). NVIDIA was strong, no doubt about it. The company has been growing at a hyper pace for over three years, but spending is shifting to nuts-and-bolts plays, as reflected in the results, and positive feedback loops are forming. When AI infrastructure comes online, applications and new use cases follow, leading to increased demand and helping sustain the cycle. The communications sector was also strong, coming in second with earnings up by 50%. The season-end tally is more than 5000 basis points better than expected, underpinned by results from Mag Seven and large-cap stocks such as Alphabet (NASDAQ: GOOGL), Netflix (NASDAQ: NFLX), and Meta Platforms (NASDAQ: META). The caveat is that, while AI underpinned their strengths, one-offs were also involved. Either way, the sector and these companies are expected to continue driving index-level strength, as Alphabet and Meta Platforms are critical to AI and its applications, while Netflix is a category-leading juggernaut that is still not fully flexing its muscles. The Winner From Q1? Marvell Technology, Hands DownMarvell (NASDAQ: MRVL) is the clear winner from Q1. Not only did the company produce robust results, accelerating due to AI demand, but it also secured a major investment from NVIDIA. NVIDIA sank $2 billion into the company, securing future supply while strengthening its supply chain and preparing for next-gen transitions. The next transition will be toward more widespread use of photonics and optics, categories in which Marvell excels. And if this isn’t enough, NVIDIA CEO Jenson Huang capped off the King-making, later calling Marvell the most likely stock to hit a trillion-dollar valuation.

Marvell is the Most Upgraded stock on MarketBeat’s platform coming out of the reporting period. MarketBeat tracked 48 revisions in the trailing 90 days as of June 1, 2026, which says something for a stock with 37 analysts covering it. Some issued more than one revision, helping to lift the consensus by approximately 75% for the period. The only bad news is that, with shares trading over $300, the consensus price target of $215 assumes substantial downside, but the trend points to the high end of the range and is leading the market. Assuming Marvell can reach a trillion-dollar valuation, that would represent a more than 4x increase, or roughly 300% upside. Amazon: Still the Leader in Hyperscale Cloud BusinessHyperscalers are being boosted by AI across the board, including Amazon (NASDAQ: AMZN). Its Q1 earnings release revealed the fastest pace of AWS growth in nearly four years, approaching 30%, and it is likely to remain strong due to AI demand. Among the drivers are its proprietary chips, and the core consumer business is also strong. The takeaway is that Amazon emerged as the second-most-upgraded stock for the period, and the trend points to robust upside in its stock price. The consensus price target, which has increased by 13% since the start of the reporting period, forecasts a 25% upside, with another nearly 50% possible at the high end.

ServiceNow Gets Price Target Reset: Gains Capped for NOWServiceNow (NYSE: NOW) had a solid quarter, but slowing growth and tepid comps relative to consensus figures sapped market sentiment. The result is a number of price target reductions that are impacting price action, but don’t read too much into that. While numerous price target reductions are logged, they are offset by an equally large number of reaffirmed targets, leaving sentiment pegged at Moderate Buy and a modest double-digit upside forecasted at the consensus. The likely outcome is that ServiceNow’s stock price will wallow near recent lows until later in the year, when more news becomes available. Catalysts include the shift to usage-based AI pricing and the shift to agentic services. The question is whether they will accelerate growth, or if this large cap has seen the last of double-digit gains. As it stands, the analyst and institutions remain optimistic; institutions own more than 80% of the stock and bought aggressively in Q1 when shares were at multiyear lows.

Read This Story Online |

A 29-page National Security Strategy document - what analyst Porter Stansberry calls the 'Donroe Doctrine' - connects every major geopolitical move from the Trump administration into a single coordinated strategy targeting China's dominance over AI supply chains and the global monetary order.

China already controls 70% of rare earth mining and 90% of processing. In response, over $400 billion in data center commitments landed in 2025 alone, with $650 billion projected for 2026. Stocks like Vertiv, GE Vernova, and Arista Networks have already surged hundreds of percent from their 2024 lows.

Stansberry has identified five companies critical to this mobilization - and one key investment tied to a coming reset of the U.S. dollar itself. Read the full Donroe Doctrine research and see all five stocks

|

|

More Stories

|

|

|

Post a Comment

Post a Comment