You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here.

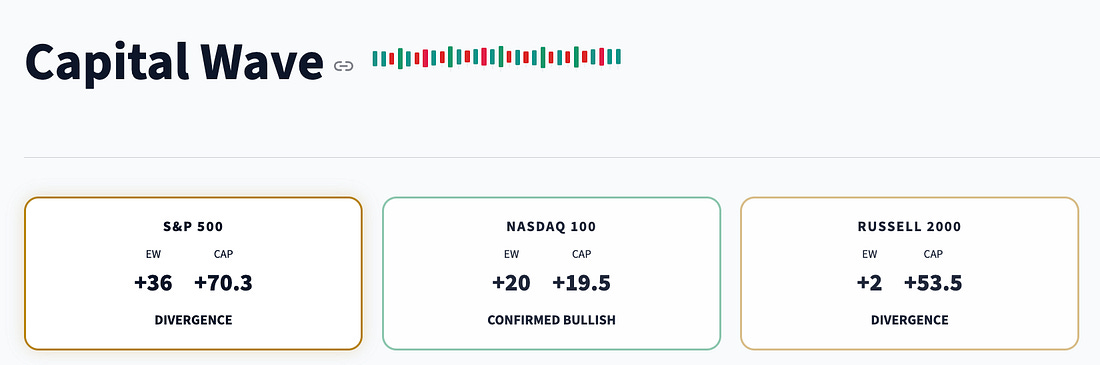

Dear Fellow Traveler: It’s been a long day… So… I explained to readers this morning, the pros were maxed out to the max… Prime brokerage gross leverage just hit a five-year high of 322.7%… with net leverage at the 85th percentile and long-short books at the 99th. The trend-following funds are loaded up… and if things go wrong, they’re going to be dumping… hard. The line in the sand remains 7,500 on the S&P 500.

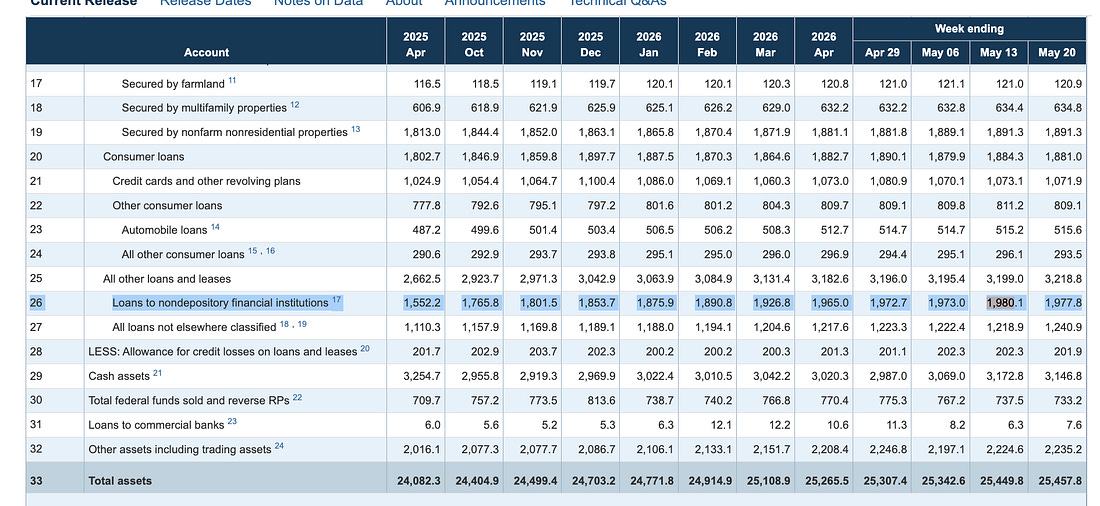

That said… the Russell 2000 is showing serious signs of cracking. I’m looking for that Equal Weight figure on Russell to go negative, and I may start to hedge with the TZA. We can blame interest rates and the Fed… but we can also have a little chat about the fact that the short-squeezes are handing back gains, software stocks are taking another bath (IGV fell 4.5% after yesterday’s note on software unwinding), and now we start to look again at the wall of zombie stocks that fill the roster of the Russell 2000. We’re close to even now on the Equal Weight Russell reading… with that index’s technology sector about to head in the wrong direction. We’re watching the Equal Weight, but this is the first mover worry… I’m still going to tell you the obvious… Watch the CW of our signal at MoneyPrinterPro.com… the FAZ is already above key moving averages, and markets are giving back some gains. What’s the issue? There’s a problem with Japan… and there’s still a screaming problem in private credit. Need proof on the latter? Having the Same Conversation…I recently had a conversation where the chatter evolved into a rather interesting excuse around the financial system. The story goes that private credit surged in the post-2008 world because “banks got out of lending…” The argument is that Dodd-Frank forced banks to hold more capital and reduce risk. Therefore, private credit took over as risk exited a regulated system. I’d say that story is half right. Banks pulled back from certain types of direct loans… but they never exited the full credit machine. They just changed their jobs and put on new ties… and changed the words around their jobs (bro, bro). Now they live in Gramercy… Rather than directly lend to companies, banks started to lend to the financial organizations that lend to the companies. That sounds counterintuitive, but once again - it all comes down to incentives… We can prove this behavior just by looking at a public database. There’s the Fed’s H.8 release. Let’s dig in… The Loan Growth IllusionI’ll start with the H.8. It calculates the weekly aggregate balance sheet of U.S. commercial banks. In the Fed H.8 release dated May 29, for the week ending May 20, total loans and leases in bank credit came in at $13.82 trillion. That figure is up from about $12.8 trillion in April 2025. It’s about a $1.01 trillion jump. Since April 2025, that is nearly 8%. That looks like a healthy economy - one where there’s money flowing to businesses… Right? But let’s do something that a lot of people won’t… dig into the numbers. If we strip out loans to non-depository financial institutions (NDFIs), you get a pretty interesting breakdown. Lending in that space increased from $1.56 trillion to $1.98 trillion during the same period. About 42% or $425 billion in total bank loan growth came from capital directed to non-bank lenders.

That’s not direct bank lending to operating companies or households. It’s bank lending to financial intermediaries that may ultimately lend to companies, consumers, or investors. Strip NDFI out and the rest of the bank loan book grew from $11.25 trillion to $11.84 trillion. That’s about a 5.2% increase combined to the 27.2% jump for NDFI. The banking system looks like it is lending. But a much larger share is swishing directly to the firms that exist because banks supposedly stopped lending. Now… let’s step back… What NDFIs Are (They Are NOT an STD)So, there’s lots of chatter about whether private credit is a systemic issue… A lot of banks… that happen to be in private credit… will of course say there’s nothing to see here… But there’s real risk (just not like 2008 bad). Luckily, we can just look at the same data sources that most of the research desks use… largely because it’s all public information. For example, the Fed’s H.8 footnote spells out what qualifies. The category covers mortgage, business, and consumer credit intermediaries, private equity funds, hedge funds, pension funds, insurance companies, investment funds, and securitization vehicles. These are all banks that lend to the groups that lend, invest, lever, securitize, warehouse, or finance other assets. So, as you see… traditional banks aren’t just lending to the economy. They are lending to the lenders. Lending to Lending is Systemic… It Just Is…So, let’s explain this with the right sort of corn… If a bank lends to a small business, that risk layer is just a single layer deep… If that business fails, the bank takes the loss - and we hear about writeoffs… But when a large bank lends money to a non-depository lender (one not backed by the FDIC), that lender turns around and lends to a business. We now have two layers of risk. The fund would take the loss, and the bank would lose if the fund fails. Now… this is where you tell me to shut up… Because - like a dad explaining to the kids on the long ride - it turns out that two layers of credit is… Leverage.

The fund uses bank financing to boost their returns… And the bank gains exposure through a financing relationship rather than direct ownership of the underlying loans. Both companies operate according to their own incentives and disincentives. Just like different groups in the financial system buy equities and futures for reasons that escape the ecosystem of other participants… Now… let’s multiply all of these actions by a nearly $2 trillion category that’s growing 27%, and you have a pretty large swing in how companies manage risk… I stress that while some people say this isn’t an issue, I do the thing that a lot of people really don’t like to do when it comes to finance. I listen to lawyers. A recent whitepaper by White & Case LLP on JDSupra walked through various structures last month. They explain that total return swaps are increasingly being used to bolster returns. Funds might be posting collateral at around 30%, while the bank provides the rest of the funding. We’re talking about loan-on-loan facilities, where a special purpose vehicle (SPV), holds the fund’s loans and then the fund borrows against them. You dizzy yet? I am… Why This Matters NowI doubt you’re ever going to read the Fed Financial Stability Report… Or the FSOC Annual Report, Or the freaking the IMF Global Financial Stability Report, Or BIS NBFI papers… But they all flag the same picture in careful language. And it’s why it’s not possible for anyone - if something goes really wrong - to say that they didn’t see a problem coming. And it’s not like 2006-07 when people are casually dismissing subprime. It doesn’t matter what the asset class is. The structure looks safe when asset prices are rising. But things go awry when credit losses show up, marks come down, redemptions surge, and funding lines have to reprice. That’s where bank lines get pulled from banks, and the fund might have to dump assets for less than what they believe them to be worth… The problem again is that the bank might also be holding collateral that also isn’t worth what they thought when they established the credit line… You don’t need it to start at scale. It just requires one or two prominent funds or vehicles to find themselves in trouble. The Tricolor and First Brands failures are not proof of a systemic crisis. They’re reminders of how quickly opacity, receivables finance, and bank exposure can collide. Reuters reported on First Brands exposure across multiple lenders. JPMorgan’s Jamie Dimon warned that more problems could emerge after a string of private-credit failures. Some banks have already paused or repriced back-leverage lending. Not yet a crisis. The early language a credit cycle uses before it learns the long words. The 2008 LessonThe lesson of 2008 was not that every crisis starts in banks. It was that leverage moves through institutions faster than anyone can map it. The GILT Crisis was about leverage… the Silicon Valley Bank crisis… leverage… the Nikkei crash? Leverage… The unwind of the basis and carry trades in recent years? Leverage… For me, I have to do all I can to make sure that I’m watching how this impacts momentum… These massive breakdowns in momentum - the ones that have come since COVID - are directly tied to what lives upstream of my world… And I have to read some of the most boring stuff in the world to know what’s happening at any given moment. In the future, pay attention to the Fed H.8 for NDFI. We’ll watch the FDIC for the longer trend. And I’ll do my best to set an alarm for the SEC Form PF to see what is happening with leverage in the private investment space… Isn’t finance wonderful? Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Post a Comment

Post a Comment