U.S. Treasury Secretary Scott Bessent is the man who oversees America’s $37 trillion debt load.

No one has more insight into what’s happening with the US dollar… mounting US debt… of the likely changes coming to the US monetary system.

Not surprisingly…

His largest personal investment holding is gold.

Not tech stocks… Not U.S. Treasuries… Not “safe-haven” index funds or ETFs…

Gold.

When the U.S. Treasury Secretary’s largest personal holding is gold…

That’s known as “a clue.”

Wanna know who else sees what Bessent does?

Warren Buffett.

At last count, Buffett is sitting on $330 billion in cash. But he knows he cannot hold this much cash forever.

- Cash is losing purchasing power at roughly 22% a year (measured in gold).

- The US political system is printing money like it’s Monopoly cash

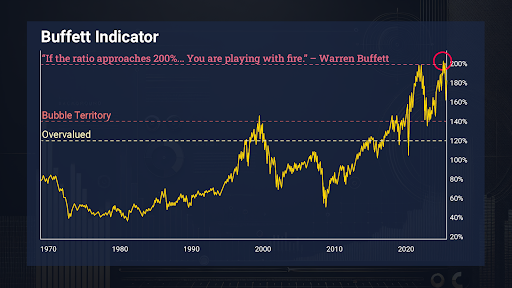

- And – most importantly – Buffett’s favorite indicator currently sitting just over 200% – which means US stocks are still more overvalued than they’ve ever been.

Every time the “Buffett Indicator” reaches a peak…

Gold goes on a tear for a decade or more. Every. Single. Time.

That’s why I believe Buffett is preparing to buy the one gold miner large enough to protect his cash. And here’s the kicker…

This large-cap miner is still trading at a 40% discount to its free cash flow.

What’s more, Trump recently tapped the CEO of this mining powerhouse to help lead America’s mining revival!

Add it all up and here’s what you get:

- The US Treasury Secretary is positioned for a major move in gold… and move that’s sure to come when he authorizes all the money required to finance more deficit spending.

- The world’s greatest investor needs a major gold position to protect his $330 billion cash pile… and there’s only one company big enough to do it.

- Trump has entrusted the CEO of the #1 major gold miner to lead a Renaissance in US mining.

You want to be in position before that happens.

You still have time to “front run” the world’s greatest investor by taking a stake in the one mining company big enough to handle his $330 billion cash hoard.

That’s why I’ve prepared a private gold briefing with:

- The name and ticker of the company Buffett is likely targeting

- Four tiny gold miners with “anomaly” upside potential up to 100X

- A special bonus pick that doesn’t mine gold at all – collects royalty income on mines it financed

Go here to get the name and ticker of Buffett’s next big move into gold.

Regards,

Garrett Goggin, CFA, CMT

Chief Analyst and Founder, Golden Portfolio

Big Analyst Revisions Could Be Ahead for SoFi Stock

Written by Gabriel Osorio-Mazilli. Published 8/26/2025.

Key Points

- SoFi stock has new fundamental tailwinds working in its favor, placing the current Wall Street analyst consensus under pressure to be changed.

- Upward revisions could send the stock higher in the coming months, and investors need to be prepared for that.

- As investors can see, institutions are already ahead of the wave in their buying activity.

Wall Street analysts are typically cautious about upgrading a stock's rating or valuation if its price is trailing the S&P 500 or its industry peers. Upgrading a lagging stock risks their reputations and careers if it fails to rebound.

This dynamic may explain the hesitancy around shares of SoFi Technologies Inc. (NASDAQ: SOFI). After lagging market indexes and real estate peers for several quarters, SoFi has embarked on a sharp rally over the past two months—one that recent U.S. macro data suggest could have further to run.

REVEALED FREE: Our three TOP stocks of 2025 are … (Ad)

Every time Weiss Ratings flashed green like this, the average gain on each and every stock has been 303% (including the losers!).

Click here for the names of our three top stocks to own this year (no purchase necessary).Now may be the time for analysts to revisit their price targets and ratings on SoFi. With the risk of backing a loser diminished, any upgrades could fuel additional momentum and reward early investors.

In the Eye of the Hurricane: SoFi Stock

Investors should track two key indicators of SoFi's mortgage-financing exposure: housing supply levels and building permit volumes. Currently, housing supply sits near a cyclical high while permits have fallen to cycle lows.

A normalization of these trends would likely boost demand for real estate financing, positioning SoFi to capitalize and potentially lift its valuation.

The second catalyst is interest-rate policy. After the Jackson Hole symposium, Federal Reserve Chair Jerome Powell hinted at the possibility of rate cuts as early as September 2025. Lower Fed funds rates would translate into cheaper mortgage rates.

This more accommodative backdrop could spark a revival in mortgage markets, making SoFi a compelling name to watch for a breakout in the coming months. But before betting on this trend, investors should examine additional fundamental factors.

Why Analysts May Need to Shift

At present, Wall Street analysts assign SoFi a consensus "Hold" rating with a $19.30 price target, implying 22.6% downside. Yet the stock has rallied 91.1% over the last quarter, suggesting these views could soon prove too conservative.

Indeed, some metrics are already improving. SoFi's short interest has declined 16% over the past month, indicating bearish investors are covering positions as the risk-reward now favors buyers.

On the earnings front, SoFi delivered 8 cents per share in its latest quarterly report, beating consensus estimates by nearly 50% (versus 6 cents expected). This performance lays the groundwork for analysts to raise forecasts and price targets.

Analysts currently project 12 cents in EPS for Q2 2026—a figure that may already assume some of the housing and rate tailwinds. However, the stock's valuation does not appear to fully reflect this growth.

The price-to-earnings-growth (PEG) ratio, which measures today's valuation against expected EPS growth, signals upside potential when below 1.0x. SoFi's PEG of 0.6x points to an undervalued growth opportunity.

Finally, institutional investors have been accumulating shares. Over the past quarter, $866 million of net buying flowed into SoFi, underscoring growing confidence in the company's outlook.

Together, these factors—declining short interest, earnings beats, a low PEG ratio and significant institutional buying—suggest analysts may need to adjust their cautious stance and acknowledge the upside potential in SoFi stock.

This email content is a paid sponsorship sent on behalf of Golden Portfolio, a third-party advertiser of MarketBeat. Why did I receive this email content?.

If you need assistance with your newsletter, please don't hesitate to contact MarketBeat's U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2025 MarketBeat Media, LLC. All rights protected.

345 N Reid Place, Suite 620, Sioux Falls, SD 57103. United States of America..

Post a Comment

Post a Comment