Hello – When central banks, retail investors and industry all clamor for the same metal, prices don’t just rise—they can launch. Our 2026 Gold Forecast: A Perfect Storm for Demand explains why spot gold could break past $4,000 this year and provides guidance on how to position yourself before it happens. Inside, you’ll discover: -

Why net-buying by central banks just hit a record first-half total, led by Turkey and India. -

How rate cuts and a weakening dollar create a powerful tailwind for precious metals. -

Three practical ways to add gold—from physical bars to high-margin mining stocks paying dividends. -

Price targets suggest $4,000 per ounce if current trends persist. This concise PDF outlines the catalysts, risks, and tactics so you can decide whether to hold the metal, own the miners, or both. 👉 Download your free Gold Forecast now. No cost. No credit card. Just actionable research before the crowd sees the signal. To your investing edge, Matthew Paulson

Founder & CEO, MarketBeat P.S. Only about 2–5 % of investors own physical gold today. If the other 95% start buying, you’ll want to be in first. Grab the report now while it’s still free.

Today's Exclusive Content What's in a Name? Shoe Carnival Plans Rebrand as 2026 Guidance Resets ExpectationsBy Chris Markoch. Publication Date: 3/27/2026.

Key Points - Shoe Carnival stock dropped after weak 2026 guidance overshadowed mixed Q4 results, including declining EPS and flat revenue expectations.

- The company’s shift to the higher-end Shoe Station concept is driving growth, but will slow in 2026 as management refines its strategy.

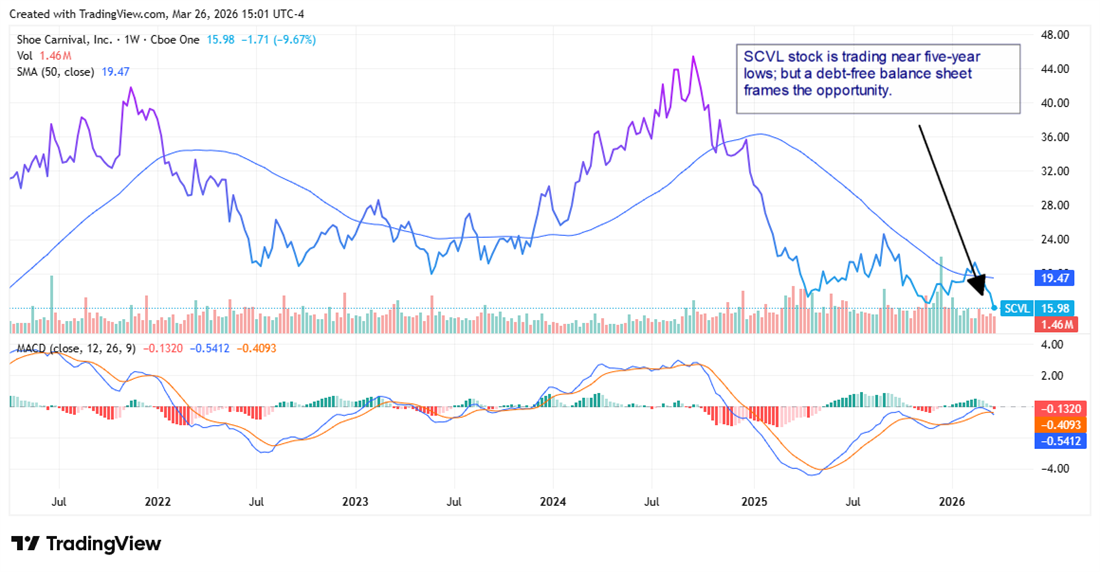

- Despite near-term concerns, SCVL offers a debt-free balance sheet, rising dividend, and a low valuation near five-year lows.

- Special Report: Elon Musk already made me a "wealthy man"

Shoe Carnival Inc. (NASDAQ: SCVL) stock fell nearly 10% after its Q4 2025 earnings report, which delivered solid but mixed results. The company met expectations with adjusted earnings of 33 cents per share, but revenue slightly missed estimates and both metrics declined from the prior year. The bigger concern was Shoe Carnival's outlook for fiscal 2026. Management forecast adjusted earnings per share (EPS) of $1.40 to $1.60, below expectations; the midpoint ($1.50) is about 20% below the $1.90 reported in fiscal 2025. Revenue guidance was also weak: net sales are expected to be roughly flat year-over-year, in a range from a 1% decline to a 1% increase. Management additionally expects profit margin to compress to about 34% (a 260-basis-point decline) due to higher tariff-related costs and increased promotional activity. In an earnings season that has separated the retail winners from the laggards, Shoe Carnival's results left investors questioning the roughly 6.5% run-up in SCVL stock during the week before the report. The stock's post-earnings reaction is a reminder that timing can matter as much as the numbers. Shoe Carnival's results weren't catastrophic, but the report arrived amid renewed geopolitical tensions, which likely amplified the negative market response. Shoe Carnival Branding Taps the Brakes What's in a name? For Shoe Carnival, plenty. The retailer continues to rebrand many stores under the Shoe Station name. At the end of its fiscal year, Shoe Station locations represented 34% (144) of the company's 426 stores, up from 10% at the start of the fiscal year. This is more than a cosmetic rebannering; it's a strategic repositioning. In November, Shoe Carnival's board approved changing the company's corporate name to Shoe Station Inc., pending shareholder approval in June. Shoe Carnival historically targeted lower-income, urban shoppers and built its identity around an in-store "carnival" atmosphere. But that value-oriented customer segment has become harder to serve profitably, in part because the growth of e-commerce has given price-sensitive shoppers many alternatives. Stores rebadged as Shoe Station aim at higher-income households that prefer an upgraded store experience and brand-focused assortments. The shift appears to be working: Shoe Station locations generated net sales of $236.7 million in fiscal 2025, accounted for roughly 21% of total revenue and delivered organic growth of 2.7% year over year. Why Management Is Taking a More Measured Approach Despite the Shoe Station traction, management said it will slow the pace of rebranding to the Shoe Station banner in 2026, citing significant variability in individual store performance. The company plans to gather more data before accelerating the rollout to: - Identify which consumer demographics respond most favorably to the Shoe Station format

- Determine which marketing channels are most effective for new customer acquisition

- Refine product assortment in rebannered stores to improve conversion

Debt-Free Balance Sheet Supports Long-Term Case There are valid reasons for investor caution, reflected in the stock's recent weakness. But for patient investors, several fundamentals support a longer-term case for Shoe Carnival. First, the company remains debt-free — uncommon for a retailer with a market cap near $400 million — and has carried no debt for 21 years. Second, on March 3 Shoe Carnival raised its dividend by 33%. The 17-cent-per-share dividend is payable on April 20 to shareholders of record on April 8. This marks the company's 14th consecutive year of dividend increases. Additionally, the stock trades at an attractive valuation of roughly 7x forward earnings. Cheapness can reflect real problems, but getting dividend growth from a debt-free company trading near five-year lows may appeal to some investors. That said, this is a retail turnaround story with risk. With short interest above 18%, many investors may prefer to wait for clear signs of a bullish reversal before adding exposure.

|

Post a Comment

Post a Comment